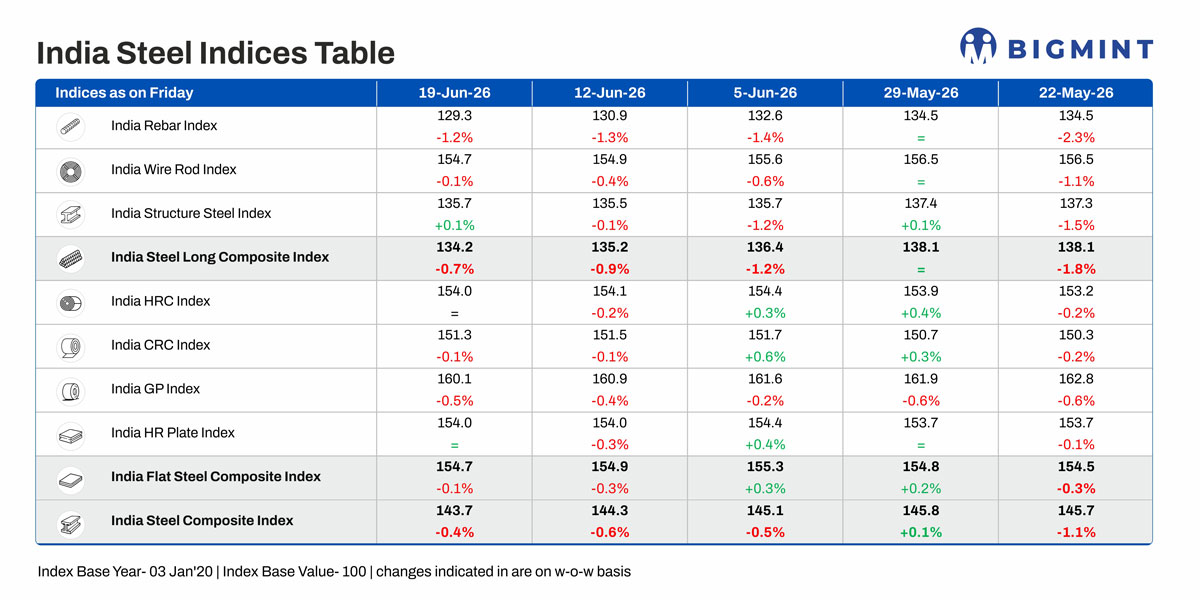

BigMint's India steel index drops w-o-w on inventory pressure, softening raw material prices

...

- High inventory accumulation impact BF rebar prices

- HRC prices largely stable amid weak trade sentiment

- Coking coal prices weaken, BigMint's India index drops w-o-w

Morning Brief: BigMint's flagship India steel composite index declined slightly w-o-w, as assessed on 19 June 2026, as inventory accumulation and weak trade market sentiment weighed on steel prices. Amid a temporary truce in the Middle East and easing fuel prices, steelmaking raw material prices saw a marginal downturn. Robust manufacturing fundamentals kept HRC largely supported, while rebar prices slipped amid the general slowdown in construction demand.

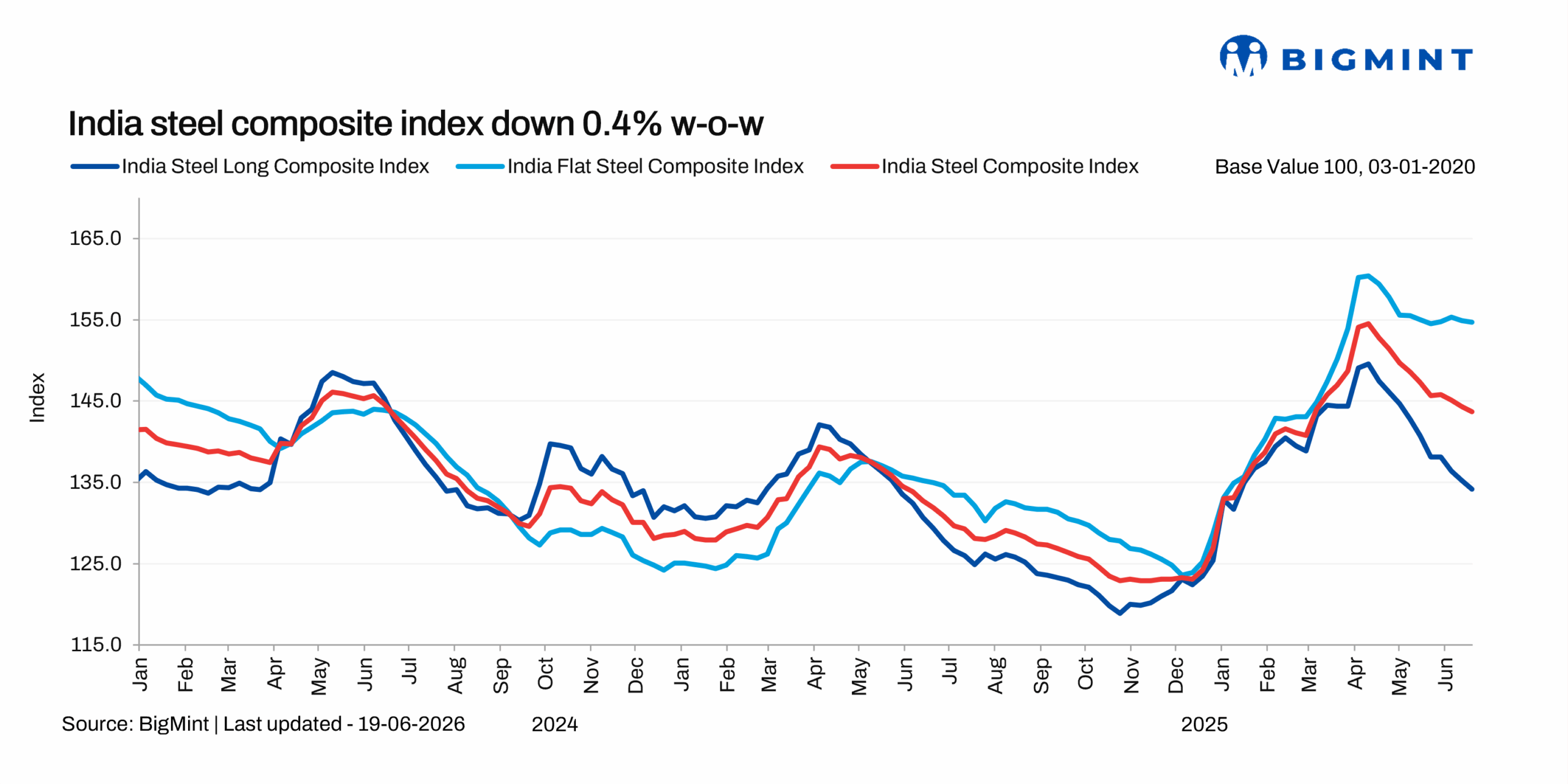

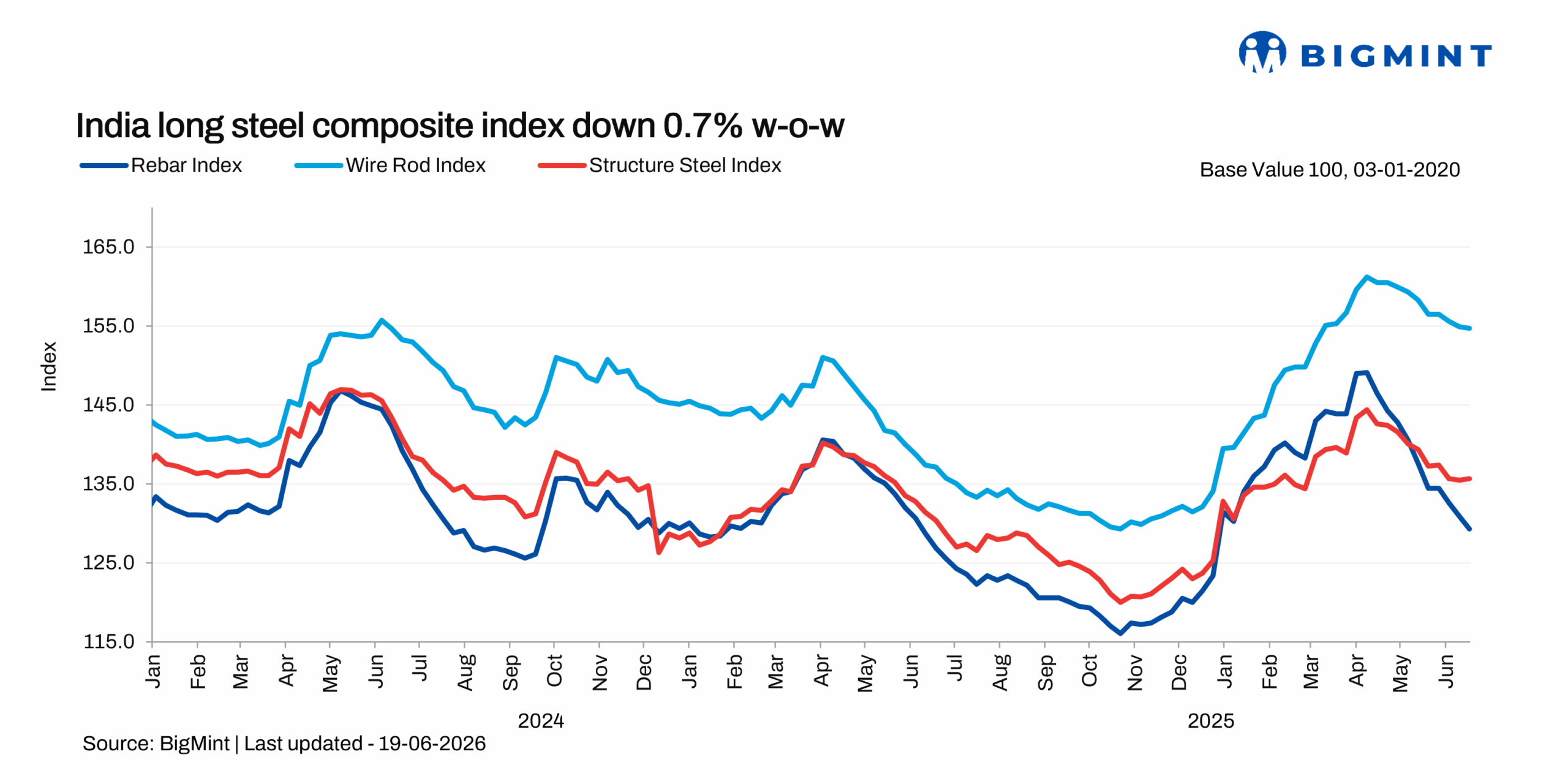

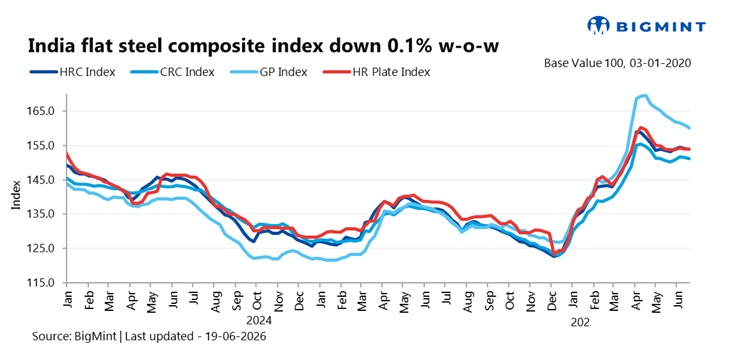

The composite index fell by 0.4% w-o-w, with the longs index declining by 0.7% compared with just 0.1% for flats.

Highlights of price movements

Inventory accumulation weighs on BF rebar prices: Blast furnace (BF)-origin rebar prices extended their downtrend, with trade-level prices (distributor-to-dealer) easing by INR 1,200/t ($13/t) w-o-w to INR 51,700/t ($547/t) exy-Mumbai. The latest correction has pushed prices to their weakest level in six months, a range last recorded in mid-January.

Elevated inventory positions exceeding 30 days at distributor stockyards, and a cautious buying approach across both the retail and project segments weighed on prices. Demand remained largely requirement-driven in most regions, while markets in south India continued to witness sluggish demand. Stable raw material prices, coupled with the availability of competitively-priced IF-route rebar further intensified pressure on BF rebar.

In the project segment, buyers continued to seek aggressive price negotiations amid subdued construction activity and limited visibility on near-term demand recovery.

IF steel markets show mixed trend: IF -rebar trade prices witnessed a mixed trend across markets, firming up in Raipur, Raigarh, and Delhi, while many other regions saw marginal corrections. Trading activity remained limited amid largely need-based deals being concluded.

Price gains in the central region were driven by an increase in electricity costs in Chhattisgarh, which prompted mills to revise offers upward. However, overall demand remained slow, restricting trade volumes. Inventories across most regions stood at around 10-15 days.

The BF-IF rebar price spread in Mumbai narrowed to around INR 6,000/t ($63/t). The differential, which was close to INR 10,000/t ($106/t) in the beginning of June, has compressed sharply.

HRC market remains stable: BigMint's bi-weekly benchmark assessment for HRC (IS 2062, Gr E250, 2.58 mm/CTL) stood at INR 58,200/t ($611/t) on 19 June, down INR 100/t from INR 58,300/t on 12 June. The assessment for CRC (IS 513, Gr O, 0.9 mm/CTL) remained stable w-o-w at INR 65,200/t on 19 June. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Trade-level HRC continued to exhibit stability amid limited trade activity and problems related to payment collection. Across regions, trading remained subdued. Market sentiment was guarded as buyers refrained from restocking and focused primarily on meeting near-term demand.

An eastern India-based mill is likely to remain under maintenance for the next one to two weeks which may limit supply in the region.

However, the absence of strong consumption trends offset any supply-side support, keeping prices largely stable.

Steel imports subdued, exports too: After a brief surge in May, steel imports again declined in June and the safeguard duty continued to support domestic prices. Exports were subdued, too, due to limited buying interest and cautious procurement strategies in major destinations in an uncertain trade environment. Exports prices to SE Asia and the Middle East actually declined last week.

Softening raw material prices: Key raw material prices remained on a downward trajectory, easing cost pressure on steelmakers. BigMint's Odisha iron ore fines (Fe 62%) remained stable on 20 June, yet iron ore prices across grades in Odisha declined last week. Premium hard coking coal (PHCC) prices softened by $2/t w-o-w to $266/t CNF Paradip. BigMint's India index dropped $1/t w-o-w.

Outlook

As the country enters the monsoon period, steel prices are expected to remain slightly subdued due to downstream weakness. Elevated inventories are weighing on rebar prices. However, some pickup in project construction activity is expected to keep rebar market sentiment supported. Despite sporadic maintenance shutdowns, the supply balance from the mills will remain undisturbed. Strong industrial and manufacturing activity is expected to lend support to HRC prices.