Will weak steel fundamentals keep Indian iron ore prices under pressure?

...

- OMC auction bid corrections drag Odisha iron ore prices lower

- Pellet, sponge iron and billet weakness weighs on raw material sentiment

- Fresh mine output additions likely to keep domestic supplies elevated

Morning Brief: Indian iron ore prices have entered a corrective phase amid weakening steel market conditions, softer pellet and sponge iron prices, and rising ore availability across key mining regions. Market sentiment in eastern India deteriorated further following the latest Odisha Mining Corporation (OMC) auction, where bids corrected sharply month-on-month, reflecting weaker downstream demand across the steel value chain.

The correction in iron ore prices has coincided with a broad-based decline in pellet, sponge iron, billet and rebar prices, indicating that downstream steel weakness is increasingly feeding back into raw material markets. While Chinese iron ore prices have remained relatively supported by stronger blast furnace utilisation and higher hot metal output, domestic Indian market conditions have weakened amid softer steel demand and cautious procurement activity.

Eastern India prices weaken after OMC auction

Market sentiment in Odisha weakened sharply after OMCs latest auction bids dropped by around INR 700-900/t m-o-m for fines and lumps. The lower bid levels reflected weakening procurement appetite among steelmakers and traders amid declining margins in finished steel markets.

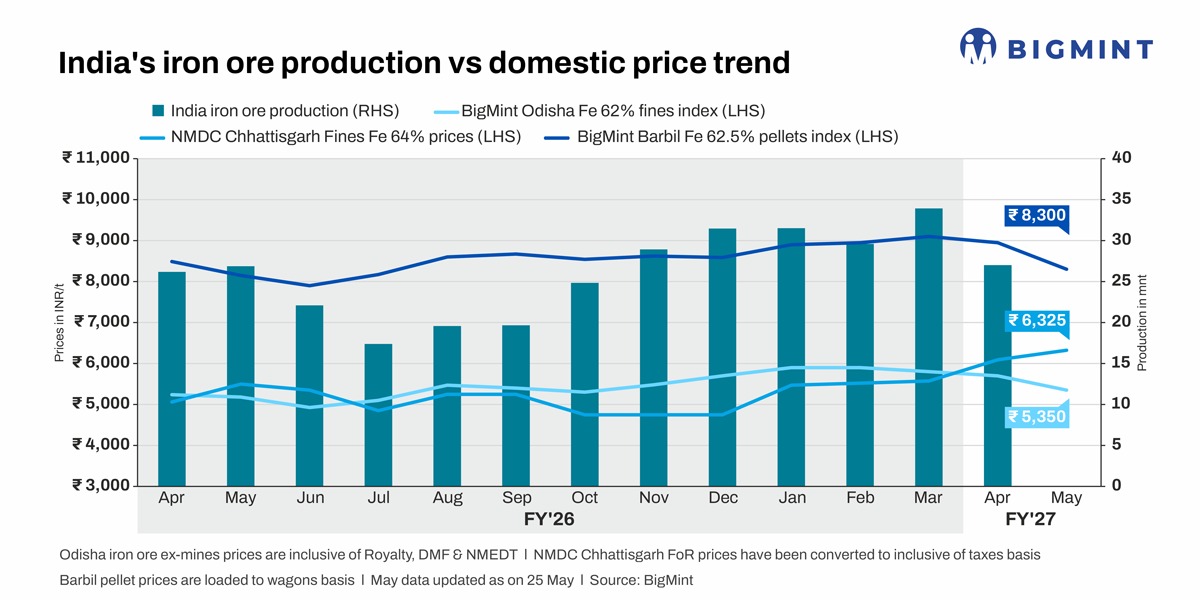

BigMints Odisha iron ore fines (Fe 62%) index declined by INR 400/t w-o-w to INR 5,100/t ex-mines Odisha following the auction outcome, with participants expecting additional price corrections as private miners revise offers lower. Pellet prices in Barbil also declined sharply, narrowing the spread between export realisations and domestic pellet prices. BigMints assessment indicated that derived Odisha iron ore fines prices may come down by INR 200-400/t, suggesting additional downside potential of nearly INR 400/t in domestic ore prices if pellet weakness persists. Also, key buyers opine chances of correction in Chhattisgarh iron ore prices too in the range of INR 200-500/t in the month of Jun'26.

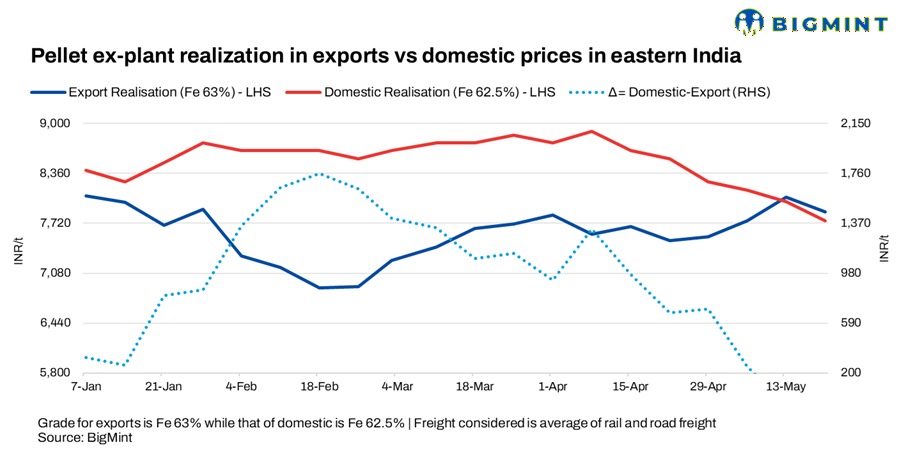

Indian pellet export prices fell in the week ended 22 May, with BigMints pellet index assessed at around $102.5/t FOB. At prevailing freight and logistics costs, ex-plant realisations for eastern Indian producers were estimated at around INR 7,600/t. In comparison, domestic pellet prices in Barbil were assessed at INR 8,100-8,200/t LTW, translating to an ex-works equivalent of around INR 7,750-7,850/t. As a result, the premium of domestic pellet prices over export realisations narrowed sharply to around INR 200/t by end-May26 from nearly INR 1,300/t over the course of the last month.

At the same time, buyers across eastern India have increasingly shifted to need-based procurement, while several distributors and steelmakers have adopted a wait-and-watch approach amid expectations of further raw material corrections.

Steel market weakness drags raw materials lower

The correction in ore prices has largely been driven by weakening downstream steel fundamentals. Sponge iron prices in Rourkela dropped by around INR 1,100/t w-o-w, while billet prices declined by nearly INR 1,300/t during the same period.

Long steel markets have also weakened. BF-route rebar prices in Mumbai fell by INR 700/t w-o-w amid sluggish buying activity, rising inventories, and cautious distributor sentiment. Market participants noted that procurement activity remained moderate, with buyers limiting inventory accumulation amid softer finished steel prices.

Higher domestic ore availability, coupled with weaker downstream absorption, has added further pressure on prices. NMDCs iron ore production rose 16% y-o-y in April to 4.64 mnt, while fresh output from Odisha mines such as BPSLs Netrabandha and Rungtas Chandiposi has started entering the market.

Outlook

We expect Indian iron ore prices are expected to remain under pressure through June amid rising domestic supplies and weak steel market fundamentals. Additional offer corrections by private miners in Odisha are likely as producers attempt to align prices with weaker pellet and sponge iron markets.

However, some restocking activity ahead of the monsoon season may temporarily support procurement activity. Chinese iron ore prices may continue receiving temporary support from elevated hot metal production and improved mill margins, although rising seaborne supply is expected to weigh on prices in the coming weeks.

To know more on what's happening in Indian iron ore industry, join the BigMint India Ferrous Week (BIFW 2026), which will take place in Kolkata from 19-21 August 2026.