What will be the impact of FTA on India's steel exports to UK? BigMint explores

...

- India had over 9% share of UK's total steel imports in 2025

- HRC exports to be affected due to sharp 90% drop in quota volumes

- Import quota under downstream processing increased by 3%

Data Deep Dive: The UK-India Free Trade Agreement (FTA) will finally come into effect from next month, four years after the negotiations started and exactly 13 months after it was signed in May 2025.

In intense last-minute negotiations, the government has claimed that it has secured duty-free access for as much as 85% of Indias steel exports to the UK despite the sharp reduction in import quotas by the UK earlier in April.

What does this mean for India's steel export prospects to the UK?

Sharp cuts in quotas

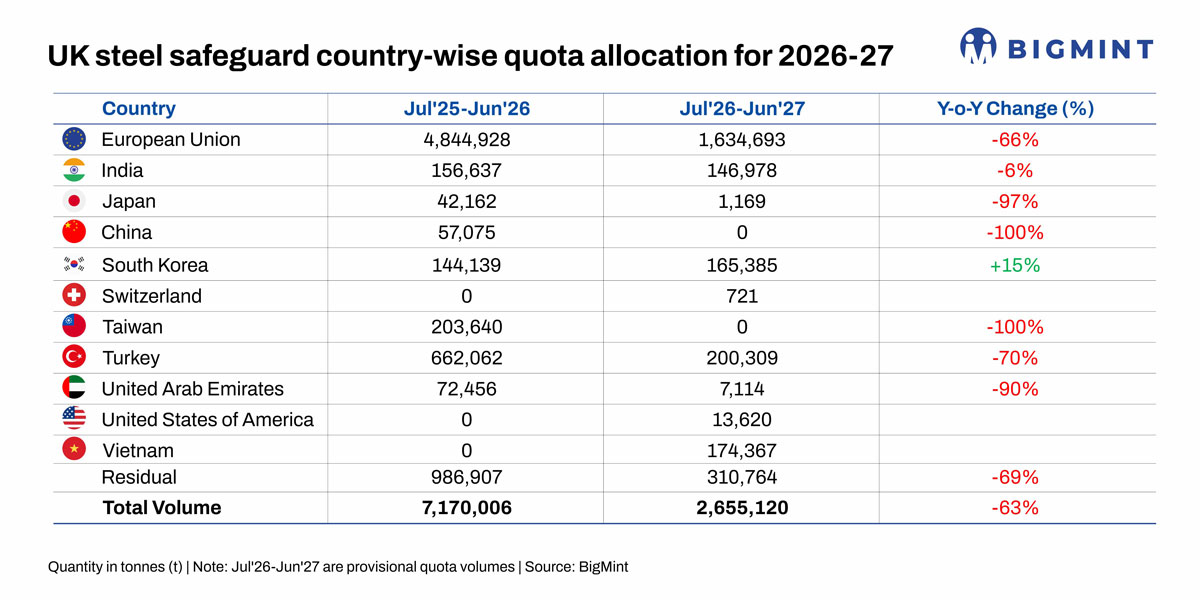

In April, the UK's Department for Business and Trade (DBT) confirmed its plan to cut the UKs tariff-rate quotas (TRQ) by 60% and double above-quota tariffs to 50%, from 1 July.

The provisional annual TRQ for hot rolled coil (HRC), detailed by the UK governments 1A non-alloy and other alloy hot-rolled sheet and strip category, has been cut by 90% to 102,341 tonnes (t). Other significant cuts include a 97% reduction in the annual TRQ for 12B non-alloy merchant bars and light sections, to 6,710 t.

However, import quota under 1B intended for further downstream processing has been increased by 3% to 2.36 mnt.

The key difference between 1A and 1B is the intended end-use: while 1A is classified as commercial imports for sale, 1B is for further "downstream" processing. This is, of course, a direct fallout of Tata Steel increasing semis imports sharply after Port Talbot closure to accelerate downstream processing in the UK.

India's exports to UK

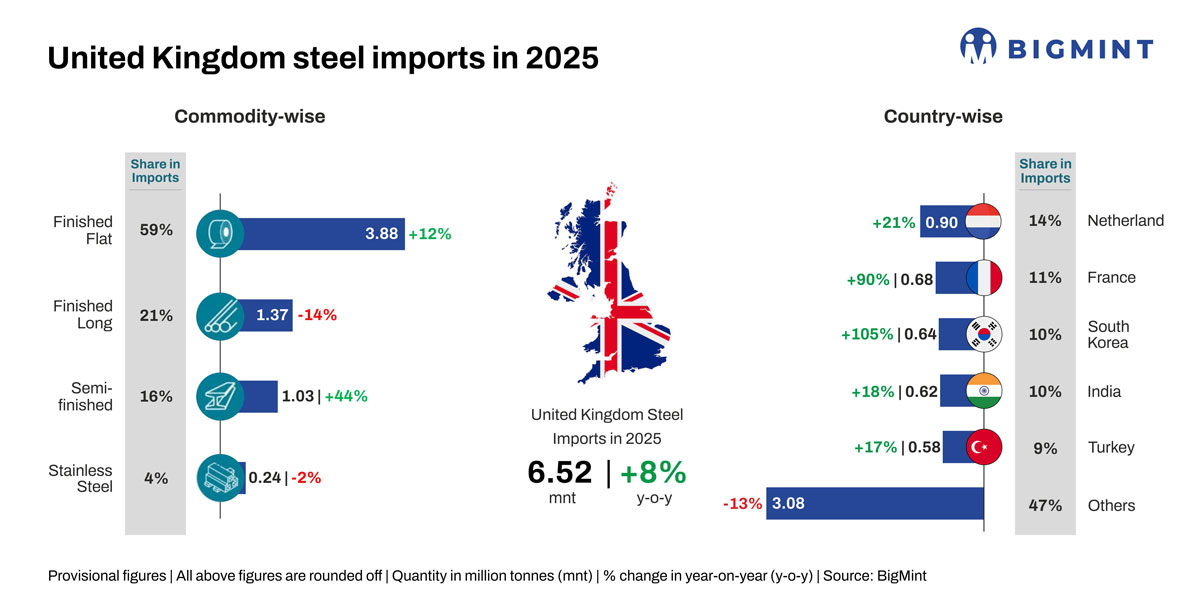

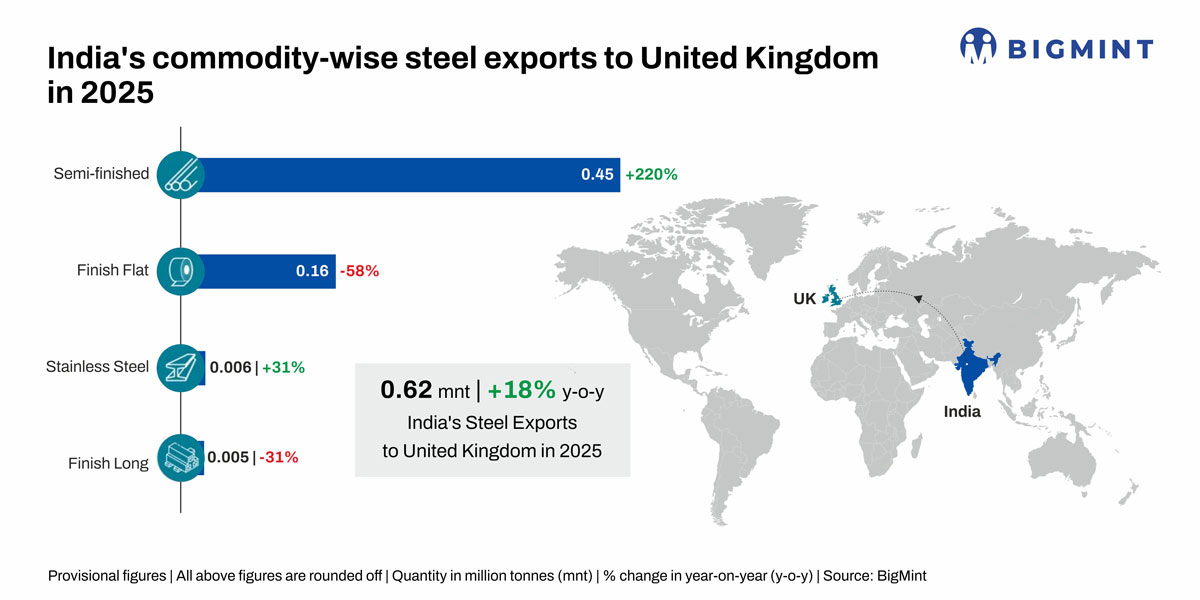

India increased its steel exports to the UK as primary steelmaking in Britain declined sharply and the country became more import dependent. As per BigMint data, India increased its steel exports by 17% y-o-y in 2025 to over 620,000 t from 530,000 t in 2024 - around 9% of total steel imports of the UK in 2025.

In fact, the over 450,000 t of semis exported from India in the form of slabs/billets to the UK in 2025 consumed nearly 40% of the quota cap on any one country under 1B norms. These are outside the purview of the TRQ.

UK's steel imports surge, industry in crisis.

BigMint data show that the UK's steel imports have grown steadily from 4.6 mnt in 2023 to 6.6 mnt in 2024 and, as per UK government data, around 7.5 mnt in 2025.

Reduction in primary steel production due to the winding down of Tata Steel's Port Talbot plant has boosted imports. Worldsteel data shows that the UK's crude steel production totalled 2.5 mnt in 2025 compared with 4 mnt in 2024 and 5.6 mnt in 2023.

In 2025, British Steel and Liberty Steels were placed under government control to avoid closures and job losses. The National Audit Office reported that the UK government is spending approximately GBP 1.3 million a day to keep British Steel's Scunthorpe site operational after the government took over from China's Jingye Group. The UK government has also committed GBP 500 million to the development of Tata Steel's 3.2 mnt EAF, which is due to come online in late 2027.

With total annual consumption pegged at over 10.5 mnt driven by the housing construction, auto and service sectors, as per government data, steel imports by the UK were sure to rise sharply, which the 60% reduction in TRQ seeks to address.

What's the fallout?

In the UK, manufacturers and traders, industry associations and end-users have voiced concerns that supply gaps can trigger price surges which will render service centres and end-users uncompetitive. A lack of domestic production capability for certain steel products is also a growing concern.

Industry associations have claimed that high steel prices would force manufacturing overseas and increase imports of finished products as mills in the UK currently do not have the capacity to meet domestic consumption.

Key takeaway

Will India's steel exports to the UK remain unaffected after the TRQ system due to advantages enjoyed as part of the FTA?

In volume terms, there is expected to be some impact due to the sharp reduction in quota cap of imports into the UK under 1A. On the other hand, there is a direct cap of 40% on any one country for imports under 1B which will naturally lower the total volume.

The UK is also coming up with a CBAM of its own. This, however, outside the ambit of the safeguard mechanism. Taxes under a prospective UK CBAM will be calculated independently of the TRQ.

In the long term, the UK has set out a steel strategy for 40-50% of UK steel consumption to be met by domestic producers, compared with around 30% in 2024. This is still a long way to go as primary production will take at least five years to return to some kind of balance. So, will the UK government do a policy re-think?

Imports, till then, will remain the only alternative.

And that way, India has a chance besides the EU, Turkiye and South Korea.