Weekly round-up: Steel prices move up, market remains firm

...

Steel prices rose across segments, supported by stronger demand and improved market sentiment.

Semi-finished and finished steel led gains, while raw material prices provided firm cost support.

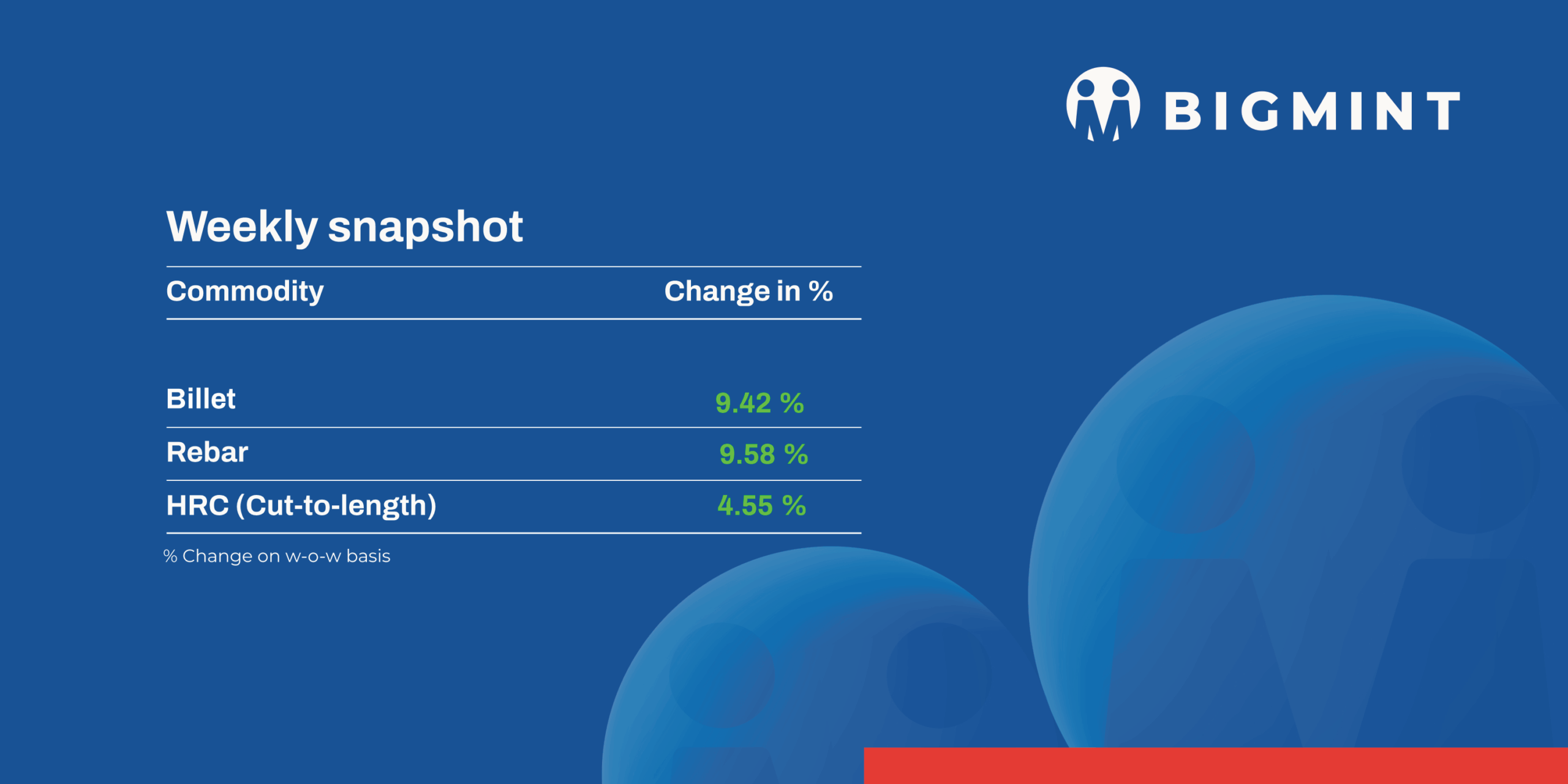

The domestic steel market recorded a positive price trend in week 01, as semi-finished steel prices increased by INR 1,700-4,200 per tonne

Iron ore and pellet

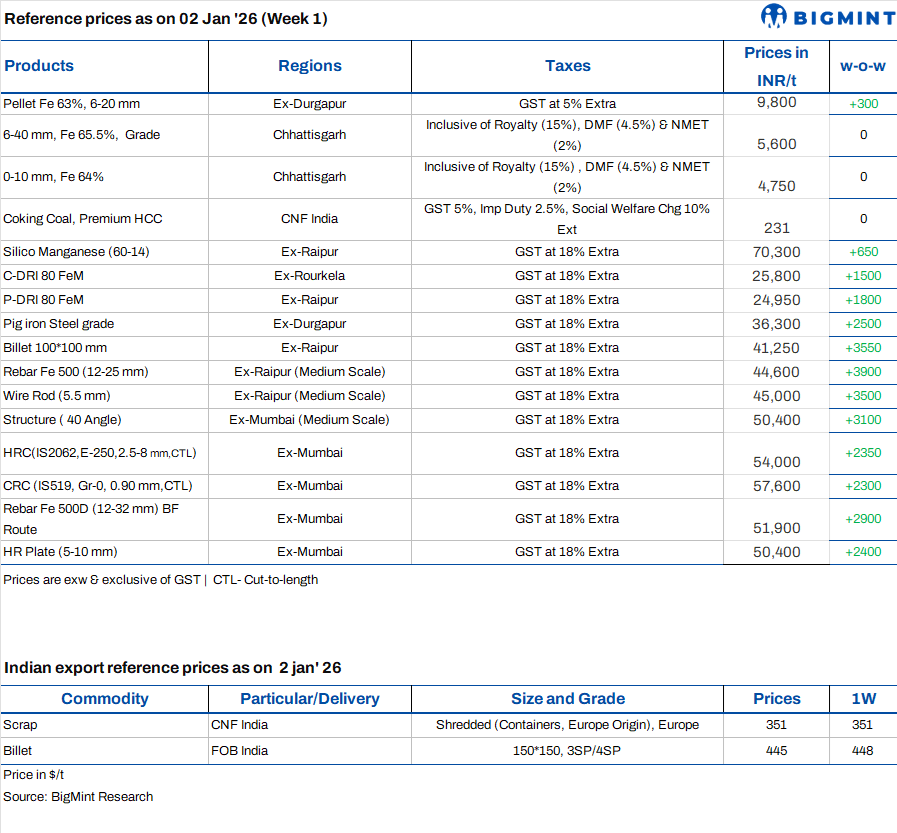

- PELLEX, BigMint's bi-weekly domestic pellet (Fe 63%) index for Raipur, increased by INR 200/t to INR 9,700/t DAP on 2 January, supported by a sharp rise in downstream steel prices and improving market sentiment. Recent strength in sponge iron and billet prices provided strong cost support to pellet producers, limiting near-term downside. Around 50,000 t of pellets were traded at INR 9,5009,600/t ex-works.

- Indian low-grade iron ore fines (Fe 57%) export prices declined by $1.5/t w-o-w to $66/t FOB east coast, while CFR China stood at $76/t. Export activity remained muted with no deals recorded amid New Year holidays and weak buying interest, as Chinese markets remained closed until 4 January.

In NMDC Kumaraswamys auction on 31 Dec25, 10,000 t of lumps (Fe 58.54%) were sold at INR 3,498/t, 24,000 t of lumps (Fe 56.69%) at INR 3,286/t, and 56,000 t of fines (Fe 57.0661.58%) at INR 2,702-4,483/t.

Coal

- Indian portside South African thermal coal prices rose INR 100-300/t w-o-w by 2 Jan26, supported by higher sponge iron prices and tighter inventories. RB2 (5,500 NAR) reached INR 9,000-9,200/t, while RB3 (4,800 NAR) held at INR 7,500-7,550/t. Despite higher offers, deals remained limited due to ample domestic coal, though falling port inventories and strong sponge iron prices supported market sentiment.

- Domestic coal prices remained stable, with 5,000 GCV at INR 5,750/t and 4,500 GCV at INR 4,800/t w-o-w, supported by adequate supply across key regions. Procurement was largely need-based, and moderate downstream demand helped maintain a balance, keeping prices rangebound.

- The Indian metallurgical coke market remained largely stable w-o-w till 31 Dec'25, reflecting balanced but cautious sentiment. BF-grade coke was unchanged at INR 32,000/t ex-Jajpur (east) and INR 29,800/t ex-works Gandhidham (west), while foundry-grade held at INR 35,200/t ex-Rajkot. Market stability was supported by the governments provisional anti-dumping duty on low-ash met coke imports, which bolstered domestic producers, while Australian PHCC remained steady at $218/t FOB, providing cost support amid rising domestic availability.

- BigMint's premium hard coking coal (PHCC) index was assessed at $236/t CNF Paradip on 2 Jan26, down $2/t w-o-w amid muted New Year trading. Global activity remained limited, though a western India steel mill booked 30,000t of Australian PHCC at $238/t CFR India for mid-Jan loading. BigMint has revised its CFR India index to include multiple origins, reflecting Indias gradual diversification from Australian supplies.

Ferrous scrap

- India: India's imported scrap market stayed firm but cautious. European shredded was offered at $350-355/t CFR, UK HMS 80:20 at $325-330/t, and PNS at $355-360/t CFR Chennai, However bids were $5-10/t lower. Buying remained limited due to year end holidays and cautious mills.

- Improved steel market sentiments encouraged buyers to exit the wait-and-watch mode and actively pursue mid-level offers.

- Approximately 4,000-5,000 t of imported scrap arrived in India, including 1,400 t HMS 80:20, with additional turning/boring, PNS, blue steel, HMS 60:40, and other HMS grades.

Ferro alloys

- Silico Manganese:Indian silico manganese (60-14) prices inched up by INR 900/t ($10/t) w-o-w to INR 69,50070,800/t ($771786/t) across Durgapur, Raipur, Vizag, and Raigarh. The uptick was supported by a modest recovery in the steel sector, with mills showing better acceptance of slightly higher-priced material. However, subdued overseas demand continued to cap any significant upside in domestic prices.

- Ferro Manganese:Indian ferro manganese (HC 70%) prices inched up by INR 700/t ($8/t) w-o-w to INR 71,500/t ($794/t) in Durgapur and went up by INR 500/t ($6/t) to INR 71,300/t ($792/t) in Raipur. Prices rose due to improved domestic steel demand, restocking activity by buyers, limited spot availability, and rising manganese ore costs supporting sentiment.Ferro Silicon:

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices edged down by INR 200/t ($2/t) to INR 106,300/t ($1,181/t) ex-works Jajpur. Buying activity remained limited, with market participants adopting a cautious stance amid expectations of further price declines.

- Meanwhile, Rashtriya Ispat Nigam Ltd has issued 2 tenders to procure a total of 1,380 t of high-carbon HC ferro chrome (Cr: 57-63%,C: 6-8%, size: 10-100 mm) for its Visakhapatnam Steel Plant, with the submission deadline set for 20 Jan'26.

Semi Finished

- India's semi-finished steel market recorded a sharp upswing this week, according to BigMint's assessment. Domestic billet prices across major markets rose by INR 1,700-4,200/t ($19-46/t) on a weekly basis, supported by improved booking activity in the semi-finished segment. Stronger offtake in finished steel further reinforced the uptrend, resulting in heightened price momentum. Amid increased volatility, robust demand across most segments was observed pan-India over the week.

- Meanwhile, the sponge iron market witnessed a notable rally, supported by a marked improvement in buying activity, which encouraged sellers to raise spot offers. Prices across key producing hubs increased by INR 1,300-2,200/t ($14-24/t) w-o-w. Procurement activity strengthened across regions as buyers returned to the market following a prolonged period of weakness in domestic sponge iron demand.

- SAIL-BSP held an auction for 910 t of steel-grade pig iron on 27 Dec'25, out of which the entire quantity was booked at an average price of INR 33,900/t exw. Bids increased by INR 2,900/t from the previous auction, conducted on 24 Oct for 910 t of steel-grade pig iron, in which the entire volume was booked at an average price of INR 31,000/t exw.

- NMDC-Nagarnar Steel Plant held an auction on 2 Jan'26 for 7,000 t of steel-grade pig iron, with the entire quantity booked at an average price of INR 36,000/t exw. Bids increased by INR 4,600/t compared with the previous auction on 18 Dec'25, in which 9,000 t were booked out of 10,000 t at INR 31,400/t exw.

- Indian DRI offers increased this week, with prices assessed at $315/t CPT Raxaul for Nepal and $325/t CPT Benapole for Bangladesh. Despite the upward price revision, export demand from both destinations remained limited, as buyers continued to adopt a cautious procurement approach.

Finished Long Steel

- IF-rebar: Indias Induction Furnace (IF) route rebar prices moved up further on a week-on-week basis. Market sentiment remained positive, with enquiries continuing across key regions, though buying interest was seen adjusting to higher price levels. Order bookings improved selectively as buyers calibrated procurement strategies amid rising offers. Mills has no inventory pressure and have future bookings of 15-20 days varying by location. Market sentiment remains positive in the near term, and prices are expected to stay on the plus side.

- On a weekly basis, prices in rebar steel witnessed increased in the range of INR 1,500-4,300/t across the regions as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 49,800-50,300/t exw Raipur, INR 45,400-46,000/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 46,500-47,300/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 44,800-45,300/t ex Raipur.

- Bf-rebar:Indian Tier-I mills increased rebar prices by up to INR 2,000/t during the last week of December 2025, sources informed BigMint.

- Trade-level BF rebar prices surged w-o-w by INR 2,900/t to INR 51,900/t exy-Mumbai, as per BigMint's assessment on 2 January 2026. Prices are exclusive of GST at 18%. Strong bookings last week supported market sentiment and prompted price hikes, with several mills also facing substantial order backlogs for the coming days.

- In the projects segment, prices stood at INR 51,000-52,000/t FOR Mumbai basis.

Flate Steel

- Leading Indian steelmakers have raised prices by INR 7501,000/t ($8-11/t) in mid-December, followed by a second hike of around INR 750/t ($8/t) in late-December.

- BigMint's benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) rose sharply by INR 1,500/t ($17/t) w-o-w to INR 49,800/t ($554/t) on 30 December against INR 48,300 ($537/t) on 23 December.

- Additionally, CRC (IS513, Gr O, 0.9 mm/CTL) prices increased by INR 1,500/t ($17/t) w-o-w to INR 56,400/t ($628/t) on 30 December against INR 54,900/t ($611/t) last week.

- India's HRC and CRC trade markets moved sharply higher, underpinned by recent mill price hikes and elevated raw material costs during the year-end holiday period. Distributors reported moderate inventory levels, while market sentiment has turned bullish.

- India's bulk imports of HRCs touched 284,481 t as of 26 December, based on vessel line-up data. Around 64,905 t of additional cargoes are expected by the early-January.

- India's bulk exports of HRCs touched 301,189 t as of of 26 December and around 35,000 t of additional cargoes are being shipped.

- BigMint's Indian HRC (S275) export index for the European Union (EU) remained unchanged w-o-w at $520/t FOB main port, as trading activity in the destination markets remained subdued due to the year-end holidays. Indian HRC (SAE 1006) export index for the Middle East also remained stable w-o-w at around $465/t.

- Leading Indian steelmakers have raised prices by INR 7501,000/t ($8-11/t) in mid-December, followed by a second hike of around INR 750/t ($8/t) in late-December.