Weekly Round-Up: Steel Markets Mixed as Raw Materials Firm, Demand Remains Cautious

...

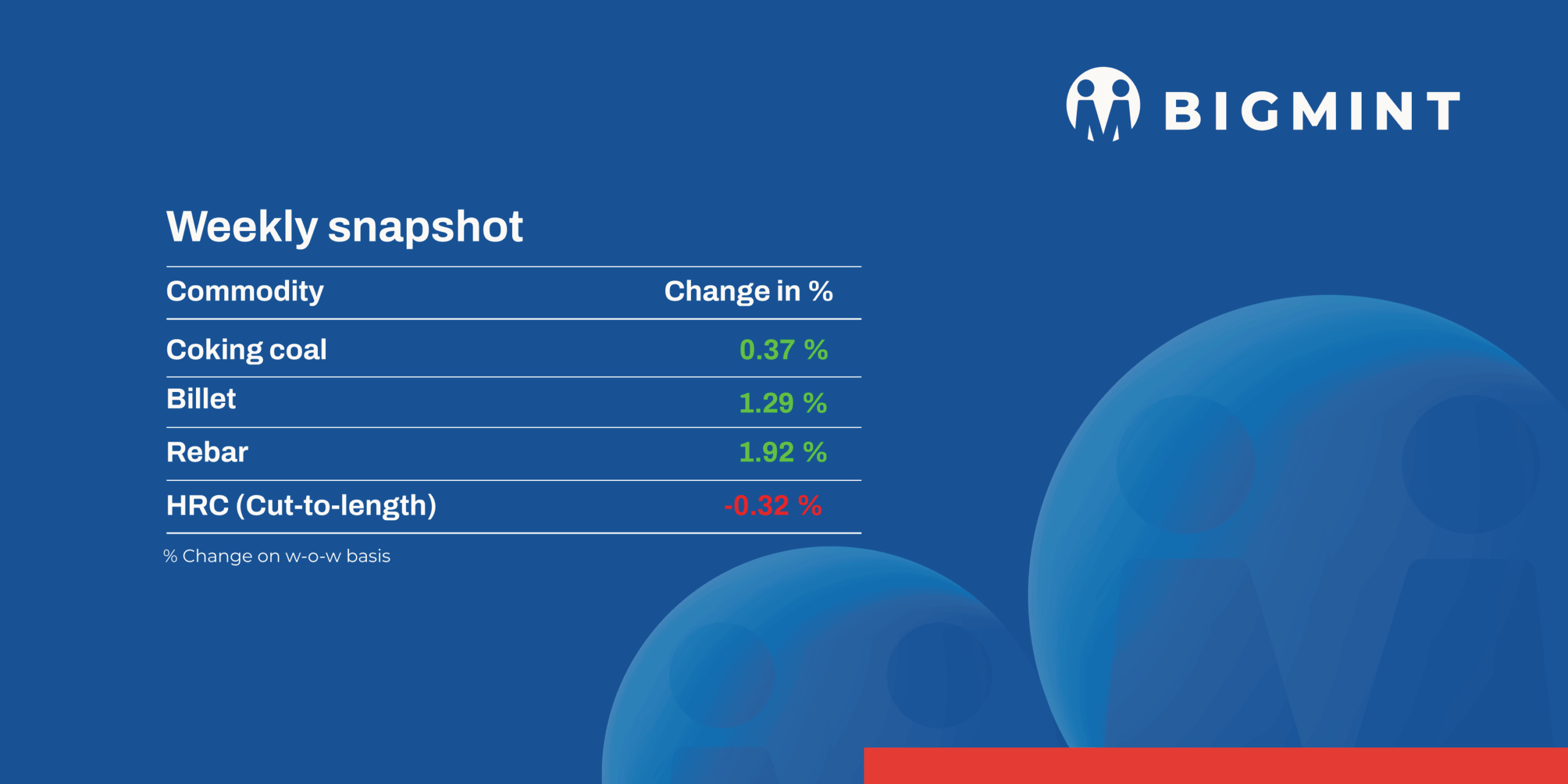

- Raw materials mixed; pellets, alloys firm while iron ore fines weakened.

- Steel demand remained cautious as inventories rose and buying stayed need-based.

Iron ore and pellet

- BigMint's India pellet (Fe 63%, 3-3.5% Al) export index edged up by $2.5/t to $105/t FOB east coast on 29 May against its previous assessment on 27 May. Export activity gained momentum as market participants capitalized on a modest decline in Chinese raw material inventories. Market sources indicated that around 350,000-400,000 t of iron ore pellets were traded during the period at approximately $119.5-127.5/t CFR China, reflecting improved buying interest from Chinese consumers.

- NMDC Limited auctioned 301,000 t of iron ore from its Kumaraswamy mines in Karnataka on 26 May 2026. The auction saw strong demand, with premiums reaching up to INR 960/t for lumps and INR 490/t for fines. Around 89,000 t of CLO (10-40 mm, Fe 60-64.37%) were sold at INR 4,497-5,756/t, while 212,000 t of fines (Fe 61.17-62.42%) were booked at INR 3,513-4,248/t, excluding royalty, DMF, and NMET charges.

- BigMints bi-weekly Indian low-grade iron ore fines (Fe 57%) export index declined by $3.5/t w-o-w to $56.5/t FOB east coast (equivalent to $72/t CFR China) on 28 May 2026. Export prices fell sharply amid persistent weakness in the global seaborne iron ore market and widening discounts for low-grade fines in the Chinese market.

- During SAIL auctions held from Monday to Friday, around 71,420 t of iron ore (Fe 55.77-61.22%) was booked at prices ranging between INR 2,725-4,250/t. The prices were on an ex-mines basis, inclusive of royalty, DMF, NMET, and additional premium charges.

Coal

- South African thermal coal sentiment remained subdued during the week, with limited enquiries and slow trade activity continuing across key Indian ports. Ex-Paradip RB2 (5,500 NAR) prices eased by INR 50/t w-o-w to around INR 11,400/t, while RB3 (4,800 NAR) prices increased by INR 50/t to around INR 9,850/t. Comfortable domestic coal availability, ample port inventories and cautious industrial buying continued to restrict import demand despite firm replacement costs.

- Domestic coal prices remained largely stable amid comfortable availability and frequent CIL auctions. BigMint assessed 5,000 GCV coal at around INR 5,500/t, while 4,500 GCV coal declined by INR 50/t w-o-w to nearly INR 4,050/t. Washed coal offers ex-Bilaspur were heard around INR 5,000-5,700/t, although some participants reported limited availability in select grades.

- The met coke market remained firm, supported by rising global coke prices and strong coking coal fundamentals. BigMint assessed Indonesian-origin BF-grade coke (65/63 CSR) at around $309/t CFR India, up $7/t w-o-w. Domestic BF-grade coke prices remained stable at INR 36,700/t ex-Jajpur and INR 33,500/t ex-Gandhidham, while Australian PHCC prices held firm at around $241/t FOB Australia.

- Imported US-origin petcoke offers softened further amid weak cement demand and growing competition from alternative fuels. Offers for US 6.5% sulphur petcoke were heard around $137-142/t CFR east coast India, while buyers largely waited for prices closer to $130/t before returning to the market. At the same time, US NAPP coal remained competitive, with portside US (6,900 NAR) coal at Kandla assessed at around INR 13,950/t, although buying activity remained cautious ahead of the monsoon season.

Ferrous scrap

- India: Imported ferrous scrap market remained weak throughout the week as poor import viability, rupee depreciation, weak steel demand, and slow downstream sales continued weighing on buying sentiment. Market participants noted that southern mills increasingly preferred domestic scrap, further reducing interest in imported cargoes.

- Imported scrap offers softened during the week, with UK-origin HMS 80:20 heard around $360-370/t CFR India and UK-origin shredded scrap at $395-400/t CFR by week-end but bids remain $15-20/t lower . However, a wide bid-offer gap persisted, with buyers targeting significantly lower levels amid continued pressure on mill margins.

- Trading activity remained limited, with only 1,500-2,000 t of imported scrap heard booked during the week, including Yemen-origin LMS and Mozambique- and Africa-origin HMS cargoes at Mundra. Chennai remained largely inactive despite ample offer availability.

Ferro alloys

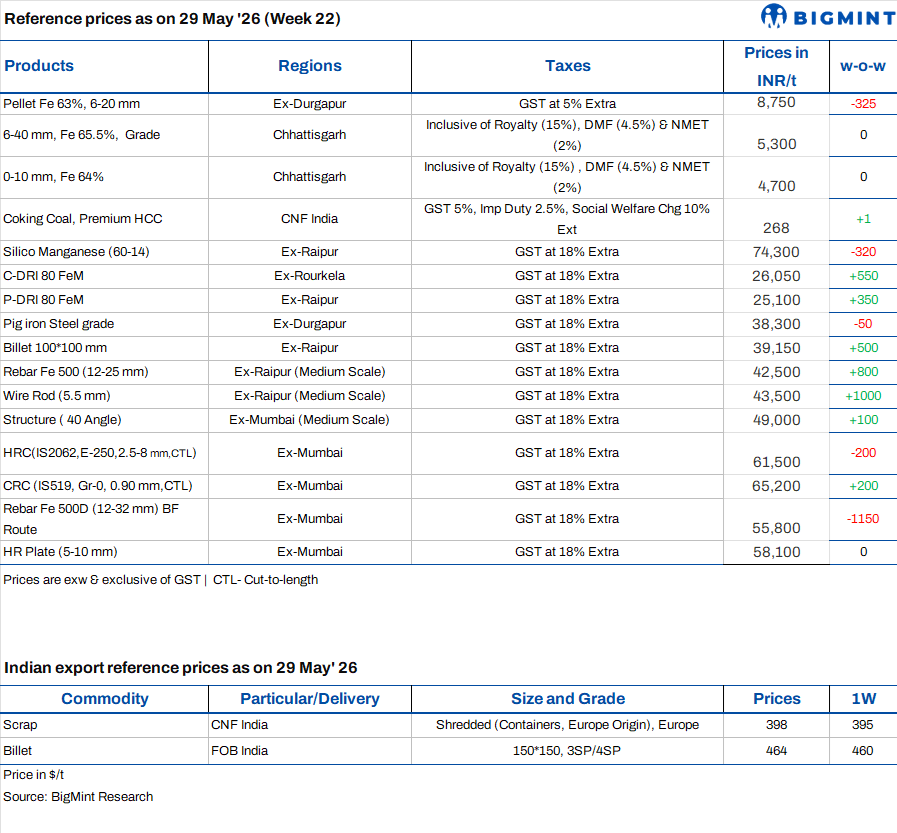

- Silico Manganese:Indian silico manganese (60-14) prices inched up by INR 250/t ($3/t) w-w-w to INR 74,000-75,000/t ($773-784/t) across key markets. The uptick was supported by a rise in buying inquiries from both domestic and export markets, reflecting improved market sentiment. Additionally, the depreciation of the Indian rupee improved export realizations, prompting stronger export interest and enabling sellers to hold firmer offers, which provided further support to silico manganese prices.

- Ferro Manganese:Indian ferro manganese (70%) prices rebounded after a prolonged downward trend, rising w-o-w by INR 1,200/t ($13/t) to INR 78,000/t ($815/t) in Raipur and by INR 1,000/t ($11/t) to INR 78,000/t ($815/t) in Durgapur. The increase was driven by producers and traders maintaining firm offers and showing limited willingness to accept lower bids, supported by improved market sentiment.

- Ferro Silicon:India ferro silicon (Si 70%) prices fell by INR 3,800/t ($40/t) w-o-w to INR 100,000/t ($1,045/t) ex-works Guwahati, while Bhutan prices also went down by INR 3,000/t ($31/t) to INR 100,000/t ($1,045/t). Prices fell to their lowest level since March 2026 as demand remained subdued, with most bookings already concluded earlier this month. Buyers were also in wait-and-watch mode, awaiting Bhutan's June offers.

- Ferro Chrome:India high-carbon ferro chrome (HC 60%, Si 4%) prices rose by INR 1,000/t ($11/t) w-o-w to INR 121,000/t ($1,264/t) ex-works Jajpur. Prices increased following strong bids at Odisha Mining Corporations (OMC) chrome ore and Vedanta-FACORs ferro chrome auctions.

Semi finished

- India's semi-finished steel market witnessed a modest-to-mixed uptrend this week, as per BigMint's assessment. Domestic billet prices across India increased by INR 450-1,200/t ($4.7-12/t) w-o-w, supported by volatile market sentiments and a moderate improvement in buying activity. The sharpest gains were recorded in Raigarh, Rourkela, and Mandi Gobindgarh, where prices rose by INR 1,000-1,200/t ($10-12/t) amid improved enquiries and tighter spot availability. In contrast, the southern region witnessed a marginal decline on a weekly basis due to weak demand from both the semi-finished and finished steel segments.

- The sponge iron market reflected a positive trend during the week, except in the southern region where prices edged lower. Pan India sponge iron prices increased by INR 100-600/t ($1-6/t) w-o-w, supported by moderate improvement in bookings and volatile market sentiments. However, Chennai registered a slight correction due to limited enquiries and weak buying interest. Overall, balanced supply conditions and improved buying activity lent support to sponge iron prices across various regions.

- On the export front, Indian DRI offers witnessed a sharp correction despite an improvement in booking activity, as lower offer levels attracted buyers back to the market. Export offers to Nepal declined by $9/t w-o-w to $311/t CPT Raxaul, while offers to Bangladesh fell by $12/t to $316/t CPT Benapole. The reduction in offers helped stimulate trading activity, resulting in improved bookings compared to previous weeks.

- NMDC's Nagarnar Steel Plant auctioned 15,000 t of steel-grade pig iron on 26 May'26, of which 3,500 t were successfully booked at a base price of INR 36,700/t exw. Bid prices declined by INR 550/t compared to the previous auction on 15 May'26 where full volume of 10,00o t were booked at INR 37,250 t exw. The lower booking volumes indicate cautious buying sentiment amid weakening market fundamentals and price resistance from buyers.

- SAIL-RSP auctioned 5,000 t of steel-grade pig iron on 28 May'26, with only 1,600 t booked at an average price of INR 37,550/t ex-works. Bids declined by INR 200/t compared to the previous auction held on 21 May'26, where 4,500 t were sold at INR 37,750/t ex-works.

- NMDC's Nagarnar Steel Plant auctioned 12,000 t of steel-grade pig iron on 29 May'26, of which 3,000 t were successfully booked at a base price of INR 36,500/t exw, down by INR 200/t from the previous auction. In the previous auction held on 26 May'26, 3,500 t out of 15,000 t were sold at the base price of INR 36,700/t exw. The weak booking reflects subdued buying interest amid cautious market sentiment and pricing pressure.

Finished long steel

- IF-rebar: IF-route rebar prices witnessed mixed trends across major regions this week, while overall trading activity remained moderate. Buying sentiment improved only for a couple of days during the week, with most buyers continuing to procure material strictly on a need-based basis amid weak demand and slower construction activity due to the extreme heatwave prevailing across most regions.

- On the manufacturer side, mills attempted to increase prices following the rise in billet and sponge iron prices in key markets such as Raipur and Mandi Gobindgarh. While the higher raw material costs provided some support to finished steel prices, buyers remained resistant to elevated offers, resulting in restricted trade volumes. However, slower booking activity continued to weigh on overall stock levels, with mill inventories reported at around 10-15 days.

- Going forward, IF-route rebar prices are expected to remain cautious amid limited buying interest on higher price levels and elevated inventory levels at mills. However, seasonal pre-monsoon restocking activity may provide partial support to prices in the near term.

- On a week-on-week basis, rebar prices showed mixed trends in the range of INR 100-2,000/t across key regions, with the sharpest decline observed in the southern region, while the northern market recorded the most significant price increase, according to BigMint's assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (1025 mm size) were assessed at INR 42,300-42,700/t exw Raipur and INR 46,000-46,600/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 44,500-45,000/t exw Raipur.

- Trade reference prices of wire rod stood at INR 43,300-43,800/t exw Raipur.

- BF-rebar: India BF rebar prices fell INR 1,000/t w-o-w to INR 55,800/t exy-Mumbai amid weak demand, rising mill inventories, and cautious buying. Inventory levels surged over 30%, while limited construction activity and persistent selling pressure kept market sentiment weak despite ongoing infrastructure project announcements.

Flat steel

- BigMint's bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) inch down by INR 200/t ($2/t) w-o-w to INR 58,500/t ($616/t) as of 29 May against INR 58,700/t ($618/t), a week ago.

- However, CRC (IS513, Gr O, 0.9 mm/CTL) increased by INR 200/t ($2/t) w-o-w at INR 65,200/t ($687/t) on 29 May against INR 65,000/t ($685/t) as on 22 May. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

- Trade-level HRC prices remained range-bound during the week ending 29 May. However, demand stayed subdued, with procurement limited to immediate requirements amid weak end-user consumption and resistance to higher offers.

- India's bulk imports of HRCs touched 307,885 t as on 22 May. Around 133,411 t of additional cargoes are expected by mid-June.

- India's bulk exports of HRCs touched 141,466 t as on 22 May. Around 69,950 t of additional cargoes are expected to be shipped.

- Indian HRC export activity remained subdued this week, with shipments to Europe and the Middle East constrained by regulatory uncertainty, logistical disruptions and weak buying sentiment.

- BigMint's bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) inch down by INR 200/t ($2/t) w-o-w to INR 58,500/t ($616/t) as of 29 May against INR 58,700/t ($618/t), a week ago.