Weekly round-up: Semi-finished steel prices drop amid overall demand downtrend

...

- IF rebar prices fall on rising inventories, approaching Holi

- BF rebar prices remain stable even as mills raise list prices

The Indian steel market remained subdued during the week ended 28 February, as demand weakened and market sentiment turned cautious. Semi-finished steel (billet) prices fell w-o-w, as finished steel saw corrections amid soft market sentiment and the upcoming Holi festive break. BF rebar prices were stable even as mills raised prices, indicating subdued trading momentum. HRC demand was lacklustre as well, with prices showing mixed trends.

Iron ore and pellet

ArcelorMittal Nippon Steel India Limited (AM/NS India) won the Alaghat West iron ore mine block with a 120.25% premium. The block spans 92.882 hectares and holds an estimated 133.4 million tonnes (mnt) of geological resources, with an average iron content of Fe 59.04%.

In SAIL's auction, 8,000 t of fines (Fe 59.5%) were sold at INR 5,325/tonne (t), while 20,000 t of CLO (Fe 60%) fetched INR 5,950/t with a premium of INR 150/t from Barsua mines on 25-26 February. Kalta saw 16,700 t of dump fines (Fe 57.56%) booked at INR 4,400/t with a premium of INR 500/t on 25 February, and Bolani recorded 20,000 t of dump fines (Fe 62.3%) sold at INR 5,875/t, carrying a premium of INR 650/t on 23 February, inclusive of royalty, DMF, NMET and extra premium.

Meanwhile, BigMints bi-weekly assessment indicated that Indian low-grade iron ore fines (Fe 57%) export prices edged up by $1/t w-o-w to $61/t FOB east coast on 26 February 2026. Despite the marginal uptick, seaborne market sentiment remained weak due to subdued trading activity after the Chinese holidays.

Ferrous scrap

Imported scrap trade activity in India remained cautious through the week, with buying largely need-based. UK-origin HMS (incinerator scrap) was booked at $255-260/t CFR, while UK-origin shredded was reported sold at $370/t CFR Chennai, although sellers continued quoting higher at $375-380/t. Demand for shredded remained limited, with HMS 80:20 workable lower at $348-350/t CFR.

Despite firm international cues and a strong dollar, weak domestic TMT demand kept mills price-sensitive. Chennai received relatively higher volumes, but buyers resisted firm Australian offers and instead preferred lower-priced, readily loaded cargoes from Malaysia, Singapore, Hong Kong, and Thailand.

Around 5,000-5,500 t were booked during the week, including nearly 2,000-2,500 t of HMS at $330-346/t CFR, along with shredded, LMS bundles, and incinerator scrap.

Ferro alloys

Silico manganese: Indian silico manganese (60-14) prices inched down by INR 400/t ($4/t) w-o-w to INR 72,600-73,200/t ($798-804/t) across Durgapur, Raipur, Vizag, and Raigarh. With market uncertainty prevailing, steel mills maintained strategic, need-based procurement of raw materials to limit further losses, keeping overall demand subdued.

Ferro manganese: Indian ferro manganese (70%) prices inched up by INR 300/t ($3/t) w-o-w to INR 74,000/t ($813/t) in Raipur and by INR 200/t ($2/t) to INR 73,700/t ($809/t) in Durgapur. The market remained cautious, with buyers limiting purchases to immediate requirements amid subdued fresh demand.

Ferro silicon: Indian ferro silicon (Si 70%) prices inched up by INR 500/t ($5/t) w-o-w to INR 98,800/t ($1,085/t) exw Guwahati, while Bhutan prices rose by INR 700/t ($8/t) to INR 99,000/t ($1,087/t). Prices have climbed to the highest level since December due to tight supply and limited spot offers, with market participants awaiting March prices from Bhutan.

Ferro chrome: Indian high-carbon ferro chrome (60%, Si: 4%) prices declined by INR 1,000/t ($11/t) w-o-w to INR 122,000/t ($1,340/t) exw-Jajpur. The market remained quiet after OMCs chrome ore auction, with most buyers having already secured material, leading to limited inquiries and weak trading activity. Additionally, at Vedanta-FACORs ferro chrome auction on 27 February, the larger lot (Cr 57% min, 10-150 mm) fetched INR 120,200/t ($1,320/t), up by INR 200/t ($2/t), while the smaller lot settled at INR 120,800/t ($1,327/t), up by INR 300/t ($3/t) from the base prices.

Semi-finished steel

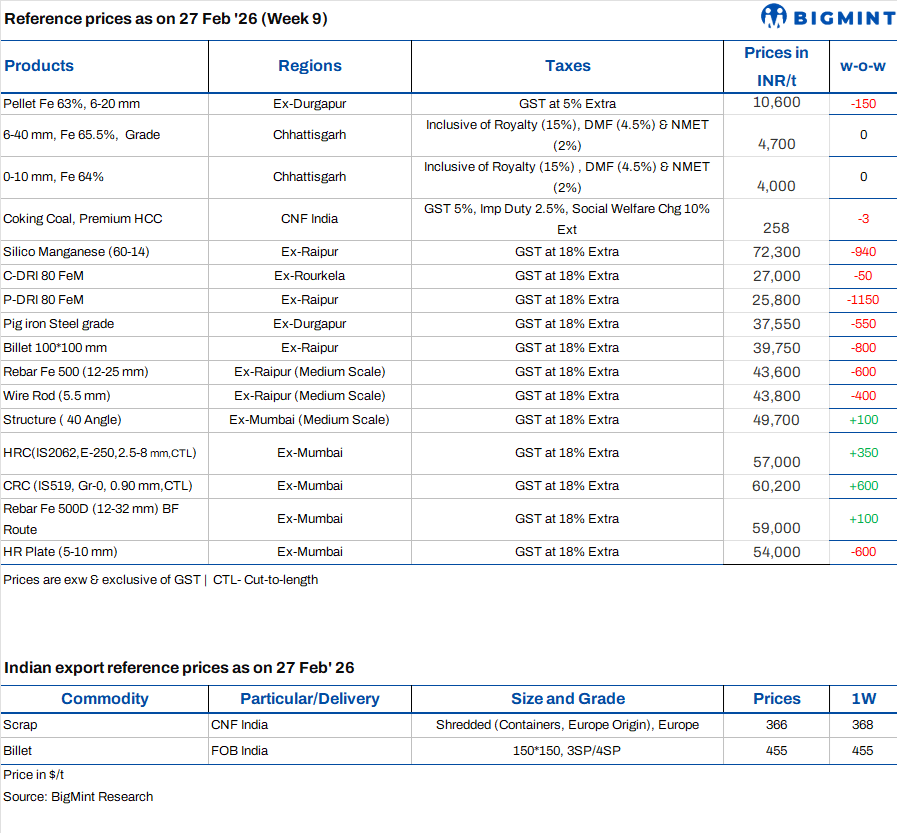

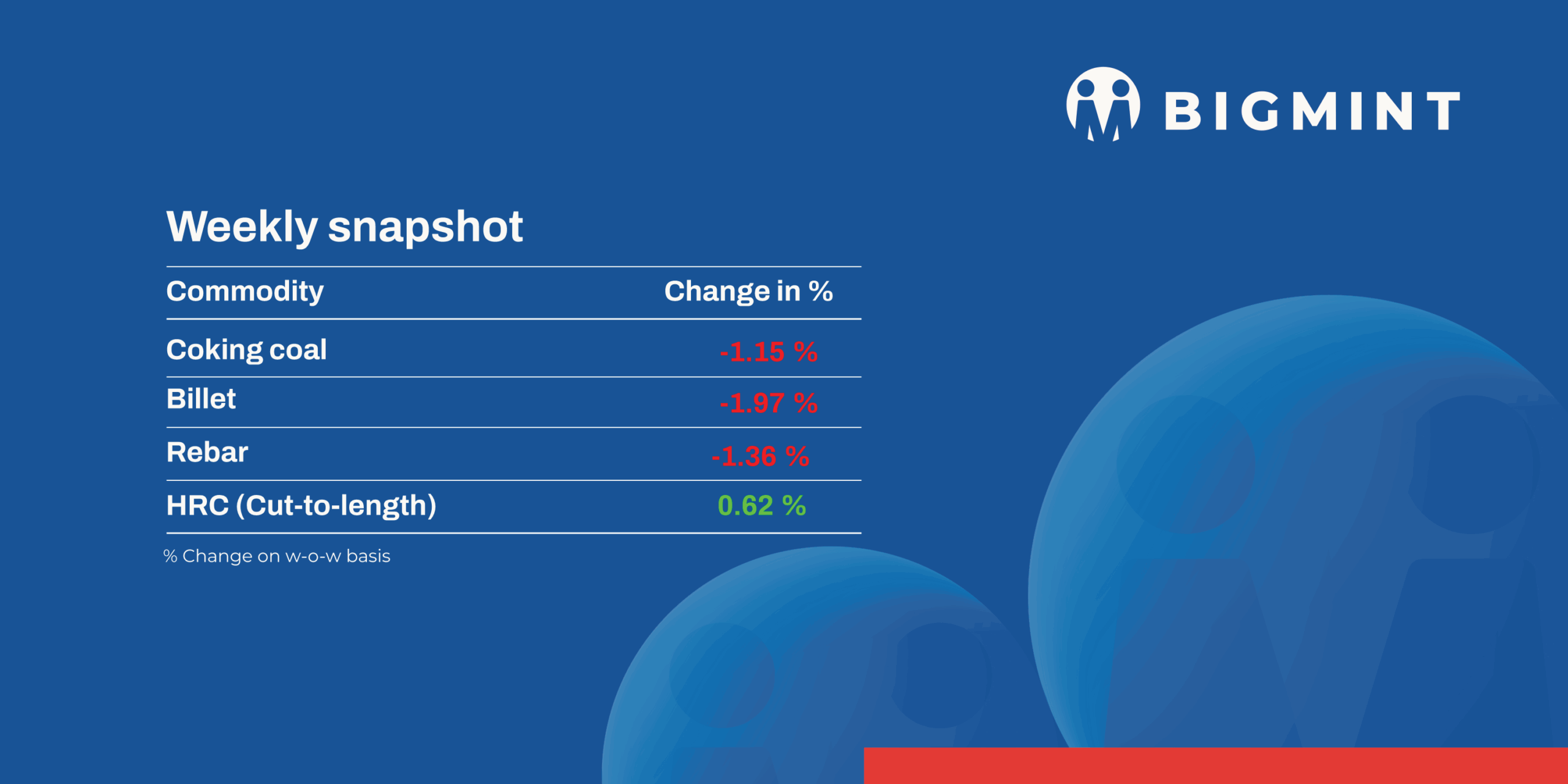

India's semi-finished steel market witnessed further correction this week, as ongoing weakness in finished steel demand and the upcoming festive holiday disruption weighed on sentiment across key producing regions. As per BigMint's assessment, domestic billet prices declined by INR 400-1,000/t ($4-11/t) w-o-w, amid weak buying interest and cautious procurement. Major regions, including Hyderabad, Mandi Gobindgarh, Rourkela, and Raipur, recorded sharp corrections of INR 800-1,000/t ($8-11/t), due to continued pressure from downstream steel demand. Market participants reported lower trade volumes, with buyers restricting purchases to immediate requirements.

Metallics

The sponge iron segment mirrored the weakness in billets. Prices in Raigarh, Raipur, and Jharsuguda fell by INR 1,100-1,150/t ($12-12.6/t) w-o-w, as reduced bookings in both billet and finished steel segments impacted sentiment. Prolonged softness in semis compelled producers to trim offers to stimulate enquiries, though overall activity remained limited. Traders noted that inventory pressure and limited fresh demand forced sellers to align prices with prevailing lower bids.

India's DRI export market remained relatively firm. Offers to Nepal were steady at $335/t CPT Raxaul, while Bangladesh offers edged up by $1/t to $345/t CPT Benapole. However, enquiries were limited, and deal volumes remained thin, indicating cautious buying interest in export destinations.

Finished long steel

IF-rebar: Indias induction furnace (IF) route rebar prices recorded a w-o-w decline amid subdued market conditions. Buying interest remained weak and largely restricted to need-based procurement; market activity has also slowed, mainly due to the upcoming Holi festival. Fresh bookings stayed limited, leading manufacturers to either reduce their offers or provide higher trade discounts depending on their existing order positions. Mill inventories have risen to above 10 days compared to the earlier maintained level of around 8-10 days across regions. Given the current scenario, any significant improvement in demand and rebar prices is unlikely in the near term, with prices expected to remain largely stable.

On a weekly basis, rebar prices declined by INR 200-700/t across regions, with Ahmedabad witnessing the sharpest fall of INR 700/t, as per BigMints assessment.

Trade reference prices of Fe 500 grade rebars (10-25 mm), manufactured through the IF route, were assessed at INR 43,40043,800/t exw Raipur and INR 47,90048,500/t exw Jalna.

Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 45,000-45,500/t exw-Raipur.

Trade reference prices of wire rods stood at INR 43,600-44,200/t ex-Raipur.

BF-rebar: Indian primary steelmakers increased rebar prices by up to INR 1,000/t ($11/t) in the week ended 27 February, sources informed BigMint. Post-revision, list prices stood at INR 58,500-60,000/t ($643-659/t) on landed basis.

Trade-level BF-rebar prices (distributor to dealer) were stable w-o-w at INR 59,000/t ($648/t) exy-Mumbai, as per BigMint's assessment on 27 February 2026. In the trade segment, prices remained largely range-bound in key markets this week owing to slowness in buying activities and ongoing material shortages.

In the projects segment, prices hovered at around INR 59,000-60,000 /t ($648-659/t) FOR basis. Demand from the projects segment remained steady with dispatches of previously booked orders. Major mills are booked till the end of March and are operating at low stock levels, which led to higher offers in the market.

Flat steel

Trade-level prices of hot-rolled coils (HRC) in India showed mixed trends w-o-w across key regions amid soft sentiment and slow trading activity, with HRC prices assessed in the range of INR 52,200-54,500/t ($574-600/t) and cold-rolled coil (CRC) prices assessed at INR 56,200-61,700/t ($618-679/t) on 24 February.

HRC market sentiment remained weak across regions, with slow demand and cautious buying dominating trade activity. While most markets saw stable to soft trends, tight availability in select southern specifications supported a slight price uptick, with participants awaiting fresh mill price direction.

India's bulk imports of HRCs touched 205,760 t as of 20 February, based on vessel line-up data. Around 121,762 t of additional cargoes are expected by mid-March.

India's bulk exports of HRCs touched 102,250 t as of 20 February. Around 9,400 t of additional cargoes are in transit.

BigMint's Indian HRC (S275) export index for the European Union (EU) remained unchanged w-o-w at around $570/t FOB main port as of 24 February. Similarly, the Indian HRC (SAE 1006) export index for the Middle East and South East Asia held steady w-o-w at around $485/t FOB main port amid weak demand and cautious buying sentiment across the regions.