Weekly round-up: Indian steel markets remain mixed amid weak demand, monsoon pressure

...

- Pellet prices rise as buyers resume bookings after recent corrections

- BF rebar prices fall further amid weak demand, monsoon disruptions

India's steel and raw materials market remained mixed in the assessment week ended 27 June 2026, with prices of some raw materials showing signs of recovery or stabilisation, while finished steel markets continued to face demand-side pressure.

Iron ore and pellet

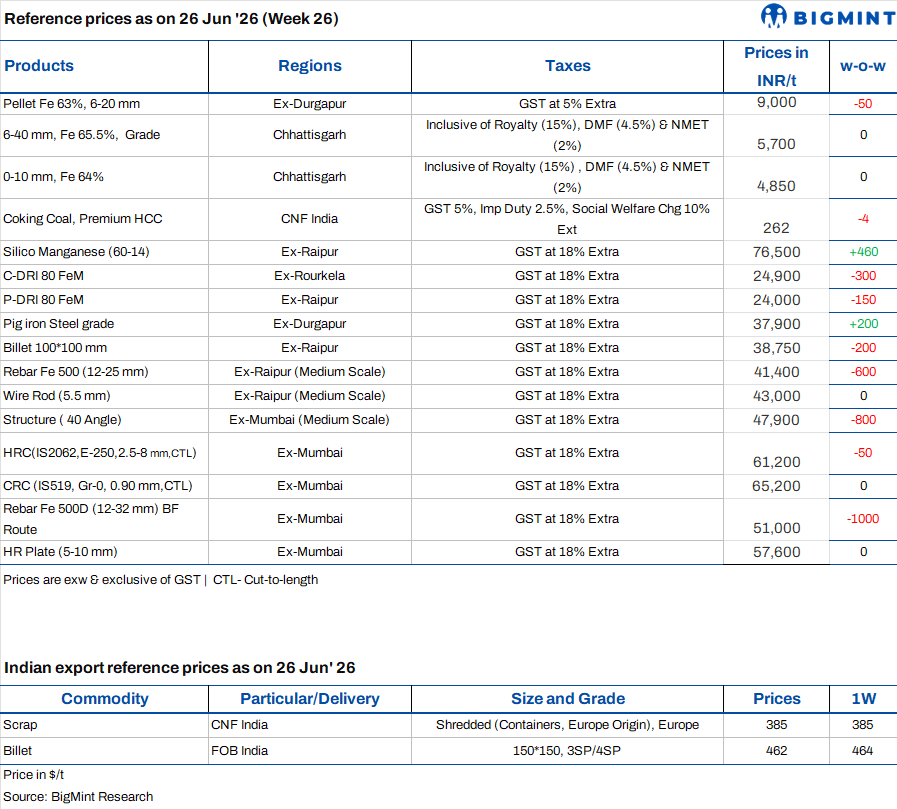

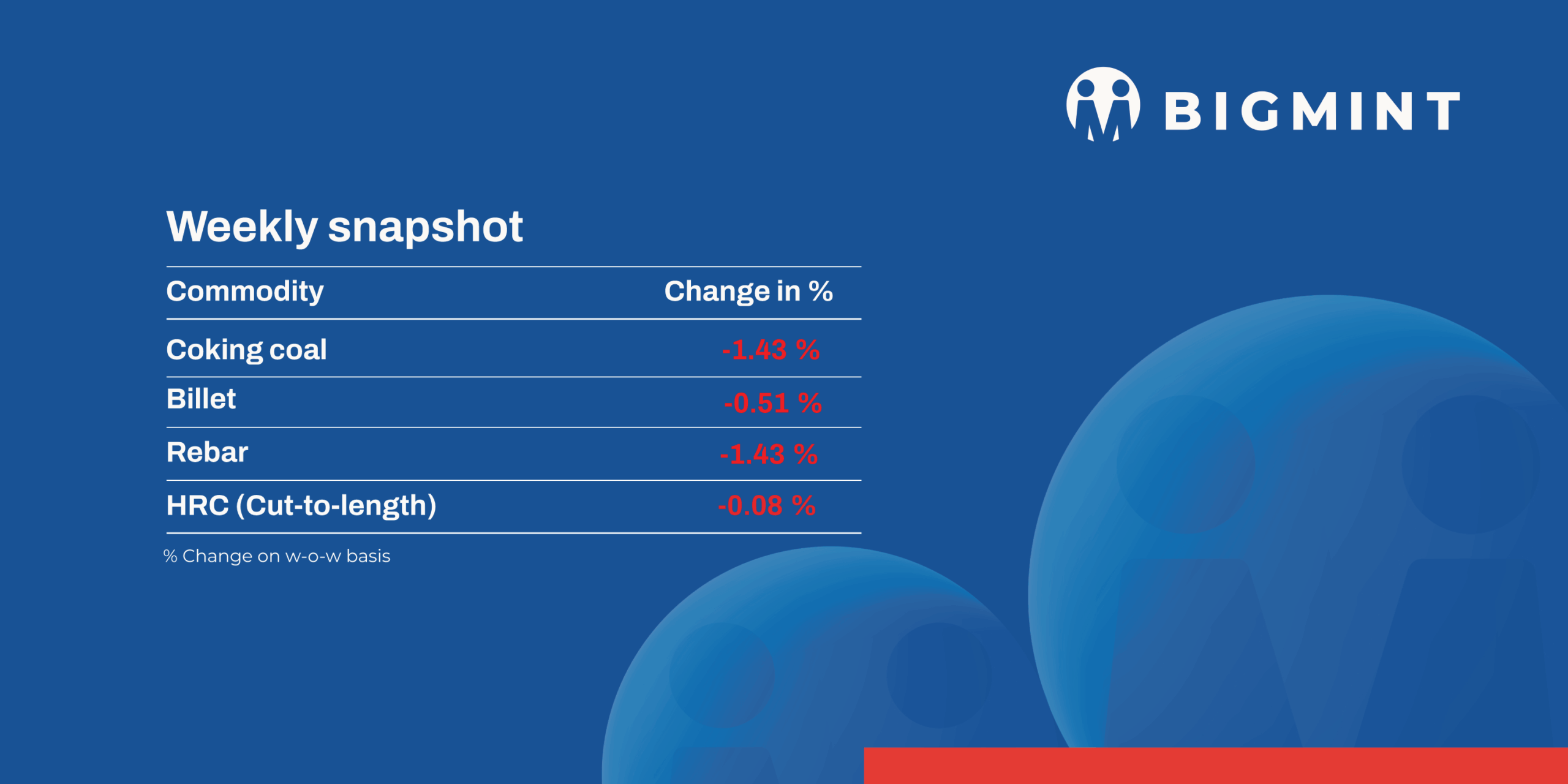

- PELLEX, BigMint's bi-weekly domestic pellet (Fe 63%) index for Raipur, rose by INR 200/t w-o-w to INR 9,100/t ($96/t) DAP on 26 June. Pellet prices in the Raipur cluster have increased by INR 200/t this week, following strong trading activity witnessed at reduced price levels last week. The price recovery comes after buyers aggressively booked material, considering the recent correction as an attractive procurement opportunity ahead of the monsoon season.

- On 22 June, of the offered 296,000 t, around 244,000 t of iron ore were booked at NMDC's auctions from Karnataka. From Kumaraswamy, 116,000-t lumps (10-40 mm, Fe 60.97-62.40%) were booked at INR 4,232-4,610/t against base prices INR 4,232-4,600/t; 84,000-t fines (Fe 61.89-62.65%) were booked at a base price of INR 3,740-3,900/t. In Donimalai mines, 44,000-t lumps (10-40 mm, Fe 53%) were booked at base prices of INR 2,177/t.

- SAIL conducted auctions for 92,000 t of iron ore fines from its Bolani and Barsua mines on 24-26 June. About 80,000 t dump fines (Fe 59.27-61.5%) were sold at INR 3,710-4,930/t (ex-mines/ FOR rake loaded). Meanwhile, in SAIL's auction on 25 June, 12,000 t of Barsua fresh fines (Fe 59.5%) were booked at INR 3,750/t (FOR loaded into rake basis). Prices included royalty, DMF, NMET, and additional premium.

Ferrous scrap

- The imported ferrous scrap market remained subdued during the week, with buying activity continuing to weaken as mills preferred domestic scrap and sponge iron amid better cost competitiveness. Weak steel demand and poor import economics kept procurement largely need-based.

- Offer indications were heard at $325-330/t CFR for UK-origin HMS 80:20 and $380-385/t CFR for UK-origin shredded scrap. Market participants reported that containerised shredded scrap prices remained largely unchanged during the week despite persistently weak buying sentiment. Domestic scrap remained the preferred raw material, particularly in central India, while mills continued to prioritise local procurement over imports due to better cost competitiveness.

- During the week, around 3,500-4,000 t of imported scrap arrived in India, comprising 1,300-1,500 t of HMS and 1,500-2,000 t of LMS, with buying largely limited to containerised, need-based cargoes.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices rose by INR 150/t ($2/t) w-o-w to INR 76,200-77,300/t ($807-819/t) across key markets. Prices edged higher as limited spot availability supported the market. Most producers remained occupied with fulfilling bulk orders booked through spot deals and auctions, restricting fresh material availability. Tight supply conditions lent support to prices.

- Meanwhile, HC 65-16 silico manganese export prices edged up by $1/t to $924/t FOB Vizag/Haldia.

- Ferro manganese: Indian ferro manganese (70%) prices rose by INR 200/t ($2/t)w-o-w to INR 79,200/t ($838/t) in Raipur and by INR 300/t ($3/t) to INR 79,300/t ($840/t) in Durgapur. Increased cost pressures across the production chain encouraged suppliers to revise offers upward, leading to a modest price gain. Meanwhile, export prices of the 75% grade also remained largely stable with a slight rise of $1/t w-o-w to $930/t FOB Vizag/Haldia.

- Ferro silicon: Indian ferro silicon (Si 70%) prices fell by INR 3,000/t ($32/t) w-o-w to INR 91,500/t ($969/t) ex-works Guwahati, while Bhutan prices also fell by INR 2,000/t ($21/t) to INR 92,000/t ($974/t). Prices fell as buying activity remained cautious and need-based, prompting sellers to lower offers.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si 4%) prices remained unchanged w-o-w to INR 123,200/t ($1,305/t) ex-works Jajpur. Prices were steady amid a stable response at both OMC's chrome ore and Vedanta-FACOR's ferro chrome auction.

- At Vedanta-FACOR's ferro chrome auction conducted on 24 June, the entire offered volume was sold. The larger lot (Cr: 57% min, 10-150 mm) achieved an H1 price of INR 122,700/t ($1,299/t) exw, exceeding the base price by INR 1,500/t ($16/t).

Semi finished

- India's semi-finished steel market remained under pressure during the week, with billet prices declining across key producing regions as cautious buying and subdued downstream demand continued to weigh on sentiment. As per BigMint's assessment, domestic billet prices fell by INR 100-800/t ($1-8/t) w-o-w across major markets. However, prices in Chennai, Mandi Gobindgarh, and Goa remained unchanged, supported by balanced supply and stable local market conditions. Market activity was limited this week amid weak finished steel demand. Producers adopted a balanced pricing strategy while maintaining disciplined spot supplies, helping prevent a significant correction in billet prices despite limited buying interest.

- The sponge iron market also softened during the week. Prices across key regions declined by INR 50-400/t ($0.5-4/t) w-o-w as buyers continued to procure only on a need basis. In contrast, sponge iron prices in Ramgarh and Jharsuguda remained unchanged, driven by limited activity.

- On the export front, Indian direct reduced iron (DRI) offers weakened further due to subdued demand from neighbouring markets. Export offers to Nepal declined by $4/t w-o-w to $300/t CPT Raxaul, while offers to Bangladesh fell by $7/t to $305/t CPT Benapole, reflecting limited buying interest and weak regional demand.

- SAIL-Bokaro Steel Plant (BSL) auctioned 14,000 t of steel-grade pig iron on 24 June, with the entire quantity sold at an average price of INR 36,400/t ex-works, up INR 800/t from the previous auction on 17 June, when 7,000 t was fully booked at INR 35,600/t. The higher price, coupled with full allocation, suggested stronger buyer participation and improving market confidence.

- SAIL-Rourkela Steel Plant (RSP) sold its entire 3,500 t offering on 25 June at an average price of INR 37,100/t ex-works, up INR 300/t from the previous auction on 15 June. The complete allocation at a higher price reflected healthy buying interest despite the softer trend in the broader semi-finished steel market.

- NMDC's Nagarnar Steel Plant auctioned 10,000 t of steel-grade pig iron on 25 June, selling 6,100 t at the base price of INR 35,800/t ex-works. Although the auction price declined marginally by INR 100/t from the previous sale on 19 June, the higher booked volume compared with 4,200 t in the earlier auction indicated an improvement in buyer participation following the slight price correction.

Finished long steel

- IF-rebar: IF-route rebar prices softened across most major markets this week, registering a decline of INR 50-800/t w-o-w amid subdued demand except in the Jaipur market, where prices increased by INR 300/t. Trading activity remained limited as market participants largely confined purchases to immediate requirements, reflecting continued caution amid weak sentiment. Demand remained subdued, keeping transaction volumes under pressure across key markets. Inventory levels were maintained at around 10-15 days, while dispatches continued without any major disruptions, indicating adequate material availability despite the sluggish trading environment. The near-term outlook remains cautious, with weak demand expected to keep prices under pressure. Prices are likely to stabilise only after a sustained pickup in end-user demand.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 41,200-41,600/t exw Raipur and INR 44,800-45,400/t exw Jalna.

- BF-rebar: Market sentiment remained bearish as weak demand, elevated inventories, aggressive buyer negotiations, and monsoon disruptions continued to pressure BF-route rebar prices.

- BF-route rebar prices in Mumbai were at INR 51,000/t ($540/t) exy-Mumbai, down INR 700/t w-o-w, with the BF-IF price spread in Mumbai stable w-o-w at INR 6,000/t. Project segment prices ranged within INR 49,000-50,000/t ($525-546/t) landed.

Flat steel

- Trade-level prices of hot-rolled coils (HRC) and cold-rolled coils (CRC) in India remained largely stable during the assessment period. BigMint's bi-weekly benchmark assessment for HRC (IS 2062, Gr E250, 2.58 mm/CTL) remained unchanged at INR 58,200/t as of 26 June 2026, while the benchmark assessment for CRC (IS 513, Gr O, 0.9 mm/CTL) also held steady at INR 65,200/t. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

- In the trade market, buying activity remained need-based despite a marginal improvement in enquiries. A distributor from north India noted that purchasing interest was slightly better than the previous month; however, transactions continued to be restricted to immediate requirements. Market participants remained cautious ahead of the monsoon season, which is expected to slow construction activity and temper steel consumption in the coming weeks.

- India's bulk HRC imports reached 156,780 t as of 19 June, with an additional 160,305 t of cargoes expected to arrive by mid-July. Meanwhile, bulk HRC exports stood at 91,076 t as of 19 June, with a further 106,600 t scheduled for shipment in the coming weeks.