Weekly round-up: Indian coal market remains muted amid need-based procurement

...

- Imported coal enquiries weak despite firm global markets

- Monsoon concerns keep industrial procurement cautious

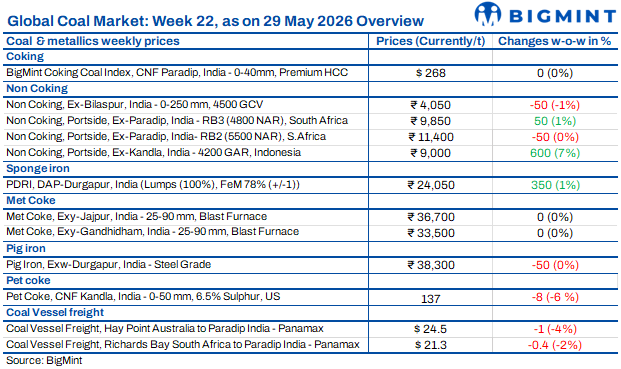

Indian coal market sentiment remained mixed during the week ended 30 May 2026. Domestic coal availability stayed comfortable due to frequent auctions and adequate supplies, limiting aggressive buying interest. Imported coal markets remained largely subdued as buyers continued requirement-based procurement amid weak industrial demand and the approaching monsoon season.

However, sponge iron sentiment improved slightly, while firm international coal prices and supply-side uncertainties continued supporting imported coal offers. Overall, market participants remained cautious, with procurement decisions driven primarily by immediate requirements and cost considerations.

Indonesian coal prices hit 3-year high

Indian portside Indonesian thermal coal prices rose sharply on 29 May, reaching their highest levels in nearly three years amid firm global coal indices, higher freight costs, limited spot availability, and uncertainty over upcoming Indonesian mining regulations.

As per BigMint's assessment, 5,000 GAR coal increased by around INR 100/t w-o-w to INR 10,900/t at Kandla, while 4,200 GAR coal surged by around INR 600/t to INR 9,000/t. Lower-grade 3,400 GAR coal rose by around INR 350/t to INR 6,800/t at Navlakhi.

Despite the rally, buyers continued need-based procurement. Coal inventories at Indian thermal power plants declined to around 49 mnt, although overall national stock levels remain adequate.

South African coal trade stays slow

South African thermal coal trade at Indian ports remained sluggish during the week amid limited enquiries, comfortable coal availability, and cautious industrial buying.

As per BigMint's assessment, portside prices showed mixed trends w-o-w, with ex-Paradip RB2 (5,500 NAR) declining by INR 50/t to around INR 11,400/t, while RB3 (4,800 NAR) increased by INR 50/t to nearly INR 9,850/t. Higher replacement costs, elevated freight rates, and a weaker rupee continued to support offers, but buyers remained reluctant at prevailing levels.

Portside inventories increased 2.4% w-o-w to 15.53 mnt, indicating comfortable supply conditions despite weak downstream demand. Meanwhile, sponge iron sentiment improved marginally, with PDRI Durgapur DAP-prices increasing by INR 350/t w-o-w to INR 24,050/t. However, procurement activity largely remained requirement-based, limiting fresh demand for imported South African coal.

Domestic coal prices remain stable

Domestic coal prices remained largely stable on 29 May amid comfortable availability and frequent CIL auctions. As per BigMint's assessment, 5,000 GCV coal was steady at around INR 5,500/t, while 4,500 GCV coal declined by INR 50/t w-o-w to nearly INR 4,050/t. Adequate domestic supply and regular auction volumes continued to reduce the need for imported coal purchases across industrial sectors. Meanwhile, washed coal offers ex-Bilaspur were heard at around INR 5,000-5,700/t, although some market participants reported limited spot availability in select grades.

US coal faces demand pressure

The US North Appalachian (NAPP) thermal coal market remained under pressure as Indias cement sector reassessed fuel economics and adopted cautious procurement strategies.

US NAPP cargoes for July-September loading were heard around $90/t FOB Baltimore, with freight to west coast India near $45/t, implying replacement costs of about $135/t CFR India. Retail market indications were heard at INR 13,200-14,000/t exw, while BigMint assessed portside US (6,900 NAR) coal at Kandla at INR 13,950/t, up INR 450/t w-o-w.

Port stocks at Kandla and Tuna stood at around 450,737 t as of 25 May. Despite improved weekly lifting of 122,876 t, buying interest remained muted amid comfortable supply and the approaching monsoon season.

Met coke market stays firm

India's met coke market remained firm in the week ended 28 May, supported by stronger global coke and coking coal prices. As per BigMint's assessment, Indonesian-origin BF-grade coke (65/63 CSR) increased by $7/t w-o-w to around $309/t CFR India amid higher FOB offers and freight costs. Trade sources reported two cargo bookings totalling around 55,000 t at $275-276/t FOB Indonesia, while fresh offers were heard near $290/t FOB.

Despite stronger import prices, domestic BF-grade coke prices remained stable at INR 36,700/t ex-Jajpur and INR 33,500/t ex-Gandhidham due to balanced supply-demand conditions and adequate availability. Australian premium hard coking coal (PHCC) prices stayed firm at $241/t FOB Australia. Meanwhile, steel-grade pig iron prices in Durgapur declined by INR 350/t w-o-w to INR 38,100/t, indicating cautious downstream buying sentiment.

Petcoke offers decline further

Imported US-origin petcoke offers into India softened during the week ended 29 May as weak cement demand and competition from alternative fuels weighed on sentiment. US 6.5% sulphur petcoke offers were heard at around $137-142/t CFR east coast India, with freight near $53/t, down by around $8-9/t w-o-w.

Cement producers largely stayed away from the market as many had already secured US thermal coal cargoes earlier at lower prices. Buyers continued waiting for petcoke prices to move closer to $130/t before making fresh purchases. Trading activity remained limited, with most procurement being opportunistic. The approaching monsoon further weakened demand expectations, while comfortable fuel availability and cautious buying behaviour continued putting pressure on sellers.