Weekly round-up: Coal markets remain subdued amid weak demand and rising domestic preference trends

...

- Imported coal demand weak amid domestic preference and rising supply

- Fuel switching rises as petcoke loses edge to domestic coal

Coal market sentiment remained cautious this week, with weak industrial demand and limited buying activity keeping overall momentum subdued. Imported coal faced pressure due to persistent bid-offer gaps and ample availability, while domestic coal gained preference amid stable supply and competitive pricing. Fuel switching trends strengthened as users moved away from expensive alternatives. Overall, the market stayed balanced but soft, with participants adopting a wait-and-watch approach.

Indonesian coal prices remain stable

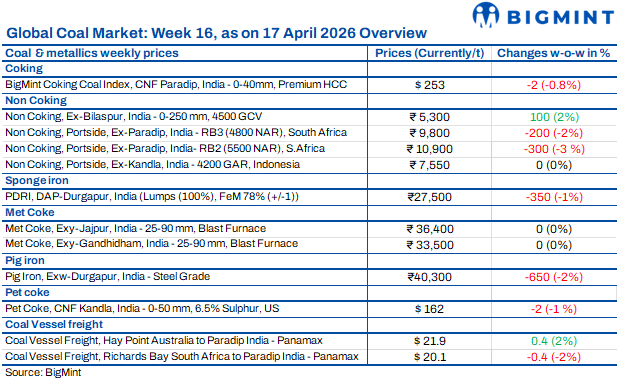

Indian portside Indonesian coal prices remained stable w-o-w as of 17 Apr'26, with 5,000 GAR at INR 9,300/t (Kandla) and INR 9,200/t (Vizag), while 4,200 GAR held at INR 7,550/t and INR 7,450/t respectively. Lower-grade 3,400 GAR declined slightly to INR 5,250/t. Weak ceramic demand kept buying subdued, though inventories eased to 13.33 mnt. Power plant stocks remained comfortable at 58.83 mnt. Global prices edged up, but muted demand kept the market range-bound.

South African coal prices decline

South African thermal coal prices at Indian ports declined w-o-w by INR 200-300, with ex-Paradip RB2 (5,500 NAR) at INR 10,900/t and RB3 (4,800 NAR) at INR 9,800/t. Limited trades were reported, with deals near INR 10,800/t levels. Seaborne offers remained weak, with FOB at $92-94/t and CFR India at $112-113/t, while freight stayed firm. Buying remained cautious amid weak demand, bid-offer gaps, and increasing preference for domestic coal.

Domestic coal prices edge up

India's domestic non-coking coal prices increased by INR 100/t w-o-w as on 17 Apr'26, with 5,000 GCV at INR 6,700/t and 4,500 GCV at INR 5,300/t, supported by strong SECL auction premiums. However, buying remained limited due to weak sponge iron demand. As per sources, higher offered volumes in upcoming SECL auctions may pressure prices, with market sentiment turning cautious despite steady industrial demand.

US coal gains over Petcoke

India's high-CV US coal market witnessed a structural shift as buyers moved away from expensive petcoke. Over 2.5 mnt of US coal was floating towards India, while portside prices remained stable at INR 14,500-15,600/t amid limited urgency. Petcoke offers stayed elevated at $168-170/t against bids near $155/t, making the market largely non-tradable. Imports of petcoke dropped sharply to just over 100,000 t in February from over 1 mnt y-o-y. Retail stocks stood near 405,000 t, while industrial buyers secured over 1.4 mnt. The shift towards coal remained firm, driven by cost advantage and supply disruptions in petcoke markets.

India met coke prices stable

India's BF-grade metallurgical coke prices remained stable w-o-w as of 16 April 2026, reflecting balanced fundamentals. Prices held at INR 36,400/t ex-Jajpur in east and INR 33,500/t ex-Gandhidham in west, while foundry-grade coke stayed at INR 36,400/t ex-Rajkot. Import parity supported the market, with Indonesian coke at $288/t CFR India. Australian coking coal prices eased by $5/t to $231/t FOB, offering limited relief. China's market remained largely stable with minor corrections and firm operations. Overall, domestic prices stayed range-bound, supported by costs and steady steel demand, though cautious buying and softer pig iron prices limited any sharp upside.

Petcoke demand weakens amid coal shift

India's petcoke market weakened as buyers shifted to cheaper coal amid high prices. Delivered offers stayed at $168-170/t against bids near $155/t, keeping the market largely inactive. US coal inflows exceeded 2.5 mnt, replacing petcoke demand across cement and industrial sectors. Despite tight supply, with USGC FOB at $103/t and CFR India near $158/t, buying remained weak. Cement players relied on coal and inventories, reducing petcoke usage. With ample coal arrivals and high prices, petcoke demand stayed subdued, and market sentiment remained cautious.

Coal freight rates firm up on key routes

Dry bulk coal freight rates to India increased w-o-w, with Richards Bay-India east coast routes at around $23-24/t and west coast near $21-22/t. Indonesian routes (East Kalimantan-Navlakhi) rose to ~$19.9/t. Strength in Panamax and Supramax segments supported sentiment, while the Baltic Index rose to 2,523. Bunker prices declined to $739/t, offering some relief. Despite firm trends, fixing activity remained uneven amid regional imbalances and cautious market sentiment.