Weekly round-up: Coal markets remain firm despite cautious industrial buying and monsoon concerns

...

- Indonesian coal supported by supply concerns

- Steel demand continued influencing procurement decisions

Coal market sentiment remained mixed during the week ended 5 June. Indonesian coal continued to find support from strong Chinese demand and supply-side uncertainties, while South African coal trade stayed subdued amid weak sponge iron demand and preference for domestic coal. Domestic coal availability remained comfortable due to regular auctions and adequate supplies. In the steel raw materials segment, firm global coking coal and coke prices supported sentiment, although downstream steel and pig iron demand remained cautious. Buyers across most coal segments continued following requirement-based procurement strategies ahead of the monsoon season.

Imported coal prices remain firm

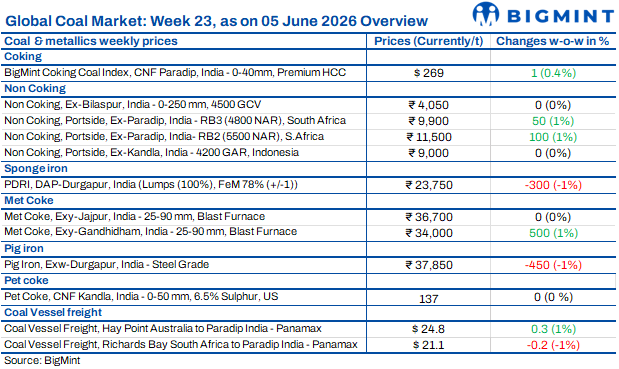

Indian portside Indonesian thermal coal prices remained firm during the week ended 5 Jun'26, supported by strong Chinese buying, limited spot cargo availability and uncertainty surrounding Indonesia's new export governance framework. Premium 5,000 GAR coal remained stable at INR 10,900/t at Kandla and INR 10,800/t at Vizag, while 4,200 GAR prices were unchanged at INR 9,000/t and INR 8,900/t, respectively. Meanwhile, 3,400 GAR coal increased by INR 50/t w-o-w to INR 6,850/t at Navlakhi amid steady industrial demand. Thermal coal inventories at Indian ports remained comfortable at 15.61 mnt, while power plant stocks declined to around 48 mnt. Firm global coal prices and tighter Indonesian spot availability continued supporting market sentiment despite cautious domestic buying.

South African coal trade slows

South African thermal coal trade remained subdued during the week despite firm global market support. Ex-Paradip RB2 (5,500 NAR) increased by INR 100/t w-o-w to INR 11,500/t, while RB3 (4,800 NAR) rose to INR 9,900/t. At Vizag, RB2 declined by INR 200/t to INR 11,100/t, while RB3 remained stable at INR 9,800/t. Indian thermal coal inventories increased marginally by 0.6% w-o-w to 15.61 mnt, reflecting comfortable supply conditions. Buyers largely preferred domestic coal, with 5,000 GCV assessed stable at INR 5,500/t and 4,500 GCV at INR 4,050/t. Weak sponge iron demand continued weighing on sentiment, with PDRI DAP-Durgapur prices falling by INR 300/t w-o-w to INR 23,750/t. High freight costs and firm global prices supported offers, but buying remained limited.

Domestic coal prices stable

Domestic coal market sentiment remained stable during the week amid comfortable supply and regular coal auctions. BigMint assessed 5,000 GCV coal unchanged at INR 5,500/t, while 4,500 GCV coal remained stable at INR 4,050/t. Buyers continued requirement-based procurement as adequate availability reduced urgency for fresh purchases. Washed coal offers were heard around INR 5,600-5,700/t Exw-Plant Bilaspur, while domestic coal remained more competitive than imported alternatives across sponge iron and industrial sectors.

US coal market softens

India's US NAPP coal market remained under pressure as falling petcoke prices reduced coal's competitiveness in the cement sector. Inventories at Kandla and Tuna ports declined to 350,950 t as of 1 Jun from a peak of 587,805 t, although supplies remained comfortable. Weekly lifting fell 19% w-o-w to 99,486 t in Week 22, reflecting cautious buying and adequate inventories. Market participants estimated around 2.5 mnt of US coal was scheduled to arrive in India during Jun-Jul, raising concerns over oversupply during the monsoon period. Ex-wharf prices remained around INR 13,500-14,000/t, while softer petcoke prices near $135.50/t CFR India continued to pressure coal demand from cement producers.

Met coke sentiment stays firm

India's metallurgical coke market remained firm during the week ended 4 Jun'26, supported by stronger global coke and coking coal prices. Indonesian-origin BF-grade coke (65/63 CSR) increased by $4/t w-o-w to $313/t CFR India, while Australian PHCC prices rose by $1/t to $242/t FOB Australia. Domestic BF-grade coke prices remained stable at INR 36,700/t ex-Jajpur, while ex-Gandhidham prices increased by INR 500/t to INR 34,000/t. Market participants closely monitored the anti-dumping duty on imported met coke, which is due to expire at the end of Jun'26.

PHCC prices edge higher

India's PHCC market remained firm during the week ended 5 Jun'26, supported by higher global coke and coking coal prices. BigMint's PHCC index increased by $1/t w-o-w to $269/t CFR Paradip amid tightening supply concerns and limited material availability. Australia-to-India Panamax freight rates rose by $0.3/t to $24.8/t. In China, the fifth round of coke price hikes of RMB 50-55/t ($7-8/t) was fully implemented, supporting global sentiment. Meanwhile, Indian steelmakers rolled over June flat steel prices amid cautious buying, while Indonesian BF-grade met coke prices increased by $4/t w-o-w to $313/t CFR India. Domestic BF-grade coke prices remained stable at INR 36,700/t ex-Jajpur.

Petcoke prices continue falling

India's imported petcoke market remained under pressure as buyers delayed purchases ahead of the monsoon season. US-origin petcoke offers fell from around $145-150/t CNF India in mid-May to $137-142/t by month-end, while buyer indications moved closer to $130/t. CFR India 6.5% sulphur petcoke was assessed at $135.50/t, down from the May average of $148.75/t, while FOB US Gulf Coast values declined to $79/t. Cement producers remained adequately stocked and focused on consuming existing inventories rather than replenishing. Interest shifted towards August-delivery cargoes amid expectations of further price declines. The correction improved petcoke's competitiveness against US NAPP coal, which was indicated around $150-160/t delivered, although procurement activity remained limited.

Domestic petcoke prices show mixed trend

Domestic petcoke prices witnessed mixed revisions in Jun'26. Nayara Energy reduced its petcoke price by INR 1,670/t to INR 19,330/t, while CPCL lowered prices by INR 450/t to INR 19,300/t amid improved supply following refinery maintenance completion and softer imported petcoke prices. In contrast, BPCL increased prices sharply, with Bina prices rising by INR 2,000/t to INR 21,000/t and Kochi prices increasing by INR 1,500/t to INR 19,500/t. MRPL also raised petcoke prices by INR 270/t, taking rake prices to INR 15,590/t. Meanwhile, imported US-origin 6.5% sulphur petcoke prices averaged around $149/t CNF Vizag in May, down by $17/t m-o-m, reflecting weaker demand and improved availability.

Coal freights show mixed trend

India's coal freight market showed mixed trends in the week ended 5 Jun'26. The Australia-India Panamax route increased by $0.3/t w-o-w to $24.8/t, supported by improved cargo volumes and tighter vessel availability. Similarly, East Kalimantan-Navlakhi Supramax freight rose by $0.2/t to $21.8/t amid healthy cargo enquiries. In contrast, RBCT-Paradip Panamax freight declined by $0.2/t to $21.1/t due to cautious sentiment and balanced vessel supply. The Baltic Dry Index fell 6% w-o-w to 3,037, while bunker prices increased by $30/t to $792/t. Brent crude futures also rose by $2.9/bbl w-o-w to $95/bbl, supporting freight costs despite mixed vessel market fundamentals.