Weak finished steel offtake pressures southern India's steel prices

...

- Slow trading activity increases inventory pressure

- Logistics issues in western India weigh on trade

Steel prices in southern India declined by around INR 500-1,000/t w-o-w, primarily due to weak demand in the finished steel segment. Subdued buying activity across key markets kept overall sentiment under pressure.

Additionally, increased sales pressure in raw materials -- particularly sponge iron in the Bellary region -- led manufacturers to reduce their offers. This further contributed to the downward trend in steel prices across the southern market.

Sponge iron, melting scrap

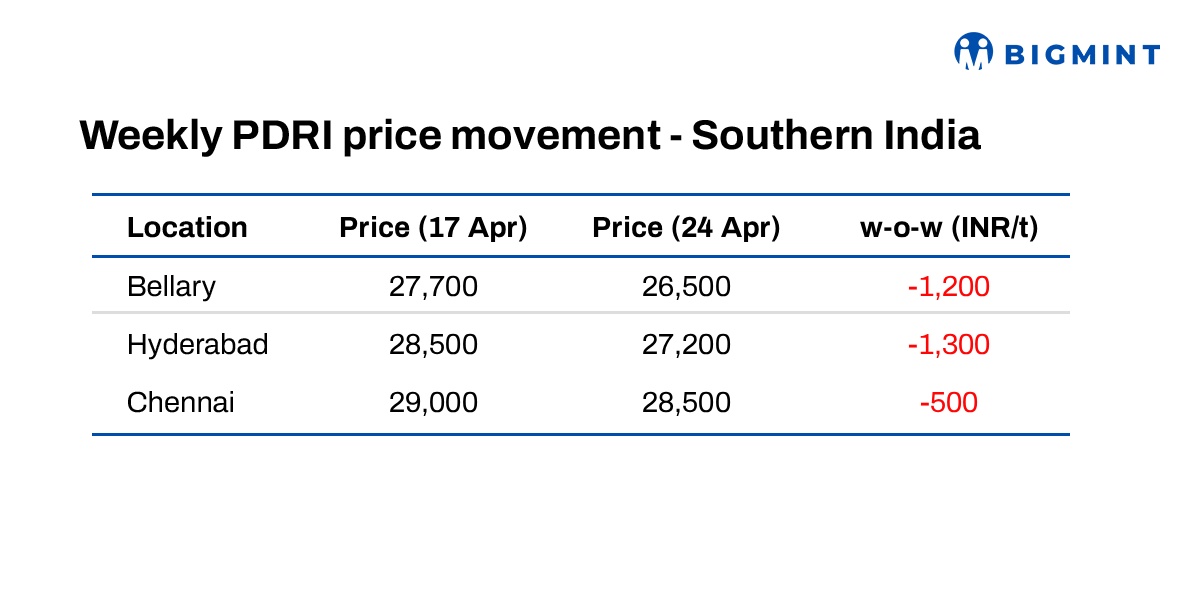

Sponge iron prices in the Bellary region declined sharply by around 5% (INR 1,200/t) to approximately INR 26,500/t w-o-w as of 24 April 2026. The primary reason for this correction is weak demand from the finished steel segment, as buyers had already booked sufficient quantities in previous months.

Additionally, falling raw material prices and steel prices in the central region have further dampened buying interest, with market participants resisting purchases at current price levels in anticipation of further short-term corrections.

Logistical challenges in the local market also disrupted the movement of supplies, resulting in limited fresh bookings, mainly restricted to local and nearby markets.

Meanwhile, pellet prices (620 mm, Fe 63%) declined by INR 150/t to INR 11,100/t ex-Bellary as of 24 April 2026. RB2 coal prices were assessed at around INR 10,900/t ex-Gangavaram Port.

In the Chennai market, melting scrap prices eased slightly by around INR 500/t w-o-w to INR 36,000/t as of 24 April 2026. The decline is attributed to weak demand from steel manufacturers and a downward trend in global scrap prices, which has pressured domestic suppliers to reduce their offers.

Additionally, trading activities in Chennai slowed down due to the general assembly elections in Tamil Nadu.

Imported HMS (80:20) scrap of Australian origin was at around $384/t CNF Chennai.

MS billets

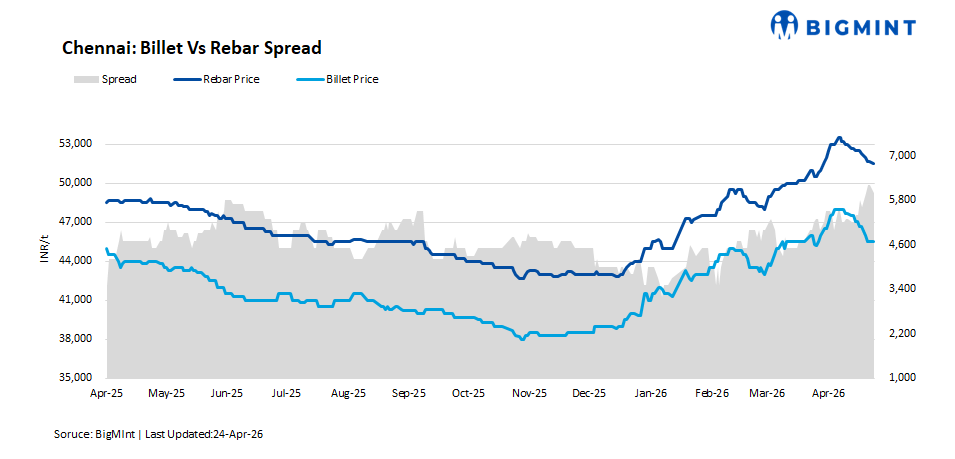

MS billet prices in the southern Indian markets declined by around INR 500-1,000/t, particularly in the Chennai and Hyderabad regions. The primary reason for the fall is weak demand from re-rollers, as demand for finished steel products slowed down.

Due to subdued offtake, billet manufacturers were compelled to reduce their offers. At the same time, declining raw material prices have manufacturers maintain conversion margins, allowing some flexibility in pricing adjustments.

The HMS (80:20) to MS billet conversion spread was at around INR 9,500/t in the Chennai market.

As of 24 April 2026, MS billet prices in the Hyderabad market were assessed at approximately INR 43,500/t ex-works.

Rebar

Induction route rebar prices declined sharply in southern markets, primarily due to weak demand from end-users. In certain areas, trading activity slowed down due to general assembly elections, while in others, buyers had already booked adequate quantities in the previous weeks.

As a result, there was downward pressure on prices. Current inventory levels for induction route rebars were estimated to be in the range of 12-18 days, depending on production capacities and product mix offered by manufacturers.

Meanwhile, blast furnace route rebar prices were assessed at around INR 60,000/t ex-works in the Hyderabad market.

The price gap between induction route and blast furnace route rebars was approximately INR 10,000/t in the Hyderabad region.

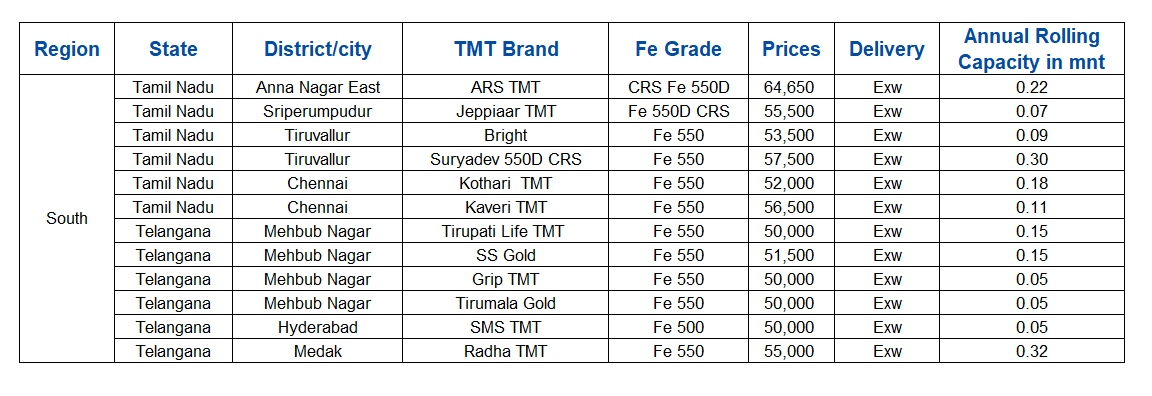

Leading steel manufacturers continue to offer induction route rebars in the local market at prevailing price levels, although selective discounts are being extended in offers to attract buying interest of customers :

Outlook

The outlook for steel prices appears cautiously positive in the near term, as prices across segments are currently hovering near their bottom levels. Despite recent corrections, raw material costs remain relatively elevated, which is putting pressure on steel manufacturers margins. In many cases, producers are operating close to or even below their break-even levels, limiting further downside in prices.

Additionally, the recent slowdown in demand was largely influenced by temporary factors such as elections and previously built-up inventories in the market. With the conclusion of the general assembly elections in Chennai (Tamil Nadu), steel trading activities and market sentiment are expected to improve gradually.