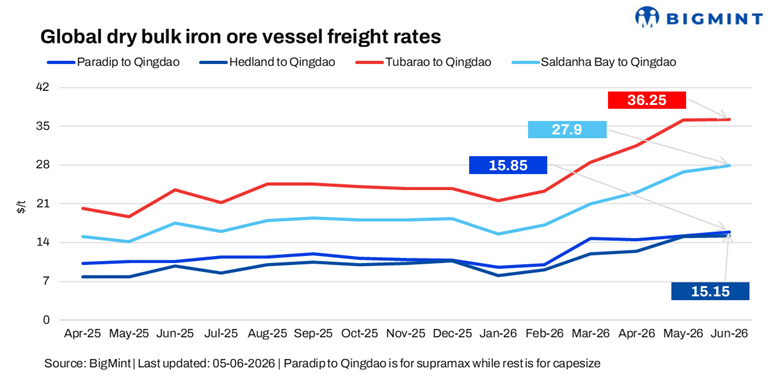

Weak Capesize sentiment drags dry bulk iron ore freight market despite Supramax gains

...

- Market confidence weakens as iron ore futures extend losses

- Lower fixture levels signal cautious chartering sentiment

Dry bulk iron ore freight rates displayed mixed trends w-o-w on 05 June 2026. Supramax freight rates strengthened this week, supported by improved regional cargo demand and tighter vessel availability across key loading regions.

In contrast, freight rates across major Capesize iron ore routes declined amid softer chartering activity, easing cargo volumes, and cautious sentiment from market participants, putting downward pressure on larger vessel earnings.

A shipbroker stated, "Capesize remained under pressure, Panamax softened marginally, while Supramax and Handysize segments were largely stable, with Handysize showing slight positive momentum."

Another source informed, "Fixture activity remains limited as a persistent disparity between owners expectations and charterers bids continues to hinder deal-making. Both parties are largely waiting on the sidelines, fixing only when cargo movement is unavoidable."

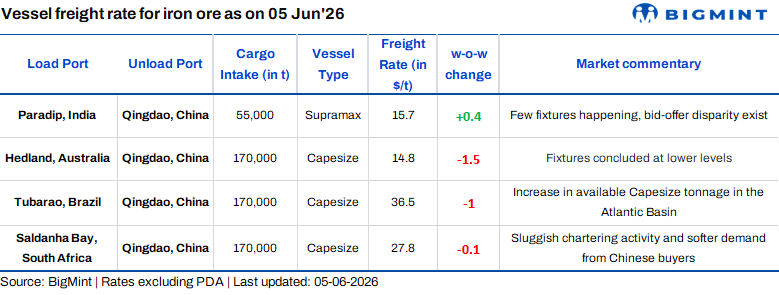

Route-wise update

Factors shaping iron ore freight rates

- Baltic Dry Index (BDI) declines w-o-w: The BDI fell by 6% (189 points) w-o-w to 3,037 on 5 June, weighed down by weaker Capesize sentiment amid subdued iron ore demand and limited chartering activity. The Capesize index dropped by 9% (477 points) to 5,040, while the Supramax index edged up by 1% (15 points) to 1,584, supported by steady minor bulk cargo demand.

- Bunker prices increase w-o-w: Bunker prices increased by $30/tonne (t) w-o-w to $792/t as of 5 June, supported by higher crude oil prices and concerns over tightening fuel supply.

- Brent crude futures rise w-o-w: Brent crude oil (August 2026 contract) was assessed at $95/barrel (bbl) on 5 June, up by $2.9/bbl w-o-w, driven by supply-side concerns, geopolitical tensions in key oil-producing regions, and expectations of stronger seasonal fuel demand.

- DCE iron ore futures fall w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) fell by around RMB 17/t ($2.5/t) w-o-w to RMB 765/t ($113/t) on 5 June, reflecting cautious market sentiment amid softer steel demand expectations and ample raw material supply.

Outlook

Iron ore freight market sentiment is expected to remain weak in the near term, with fixtures continuing to be concluded at lower levels amid subdued demand and ample vessel availability. The recent decline in iron ore futures has further dampened market confidence, suggesting limited upside potential for freight rates unless cargo volumes recover.