Tight global supply keeps APAC aluminium producers in a strong position

...

- Integrated producers gain from higher prices

- Supply security remains key market driver

Aluminium smelters across the Asia-Pacific region are expected to maintain strong profitability as tightening global primary aluminium supply continues to support metal prices. Producers in China, India, and Indonesia are particularly well positioned to benefit, owing to their integrated raw material supply chains and relatively stable power costs, which help contain cost inflation.

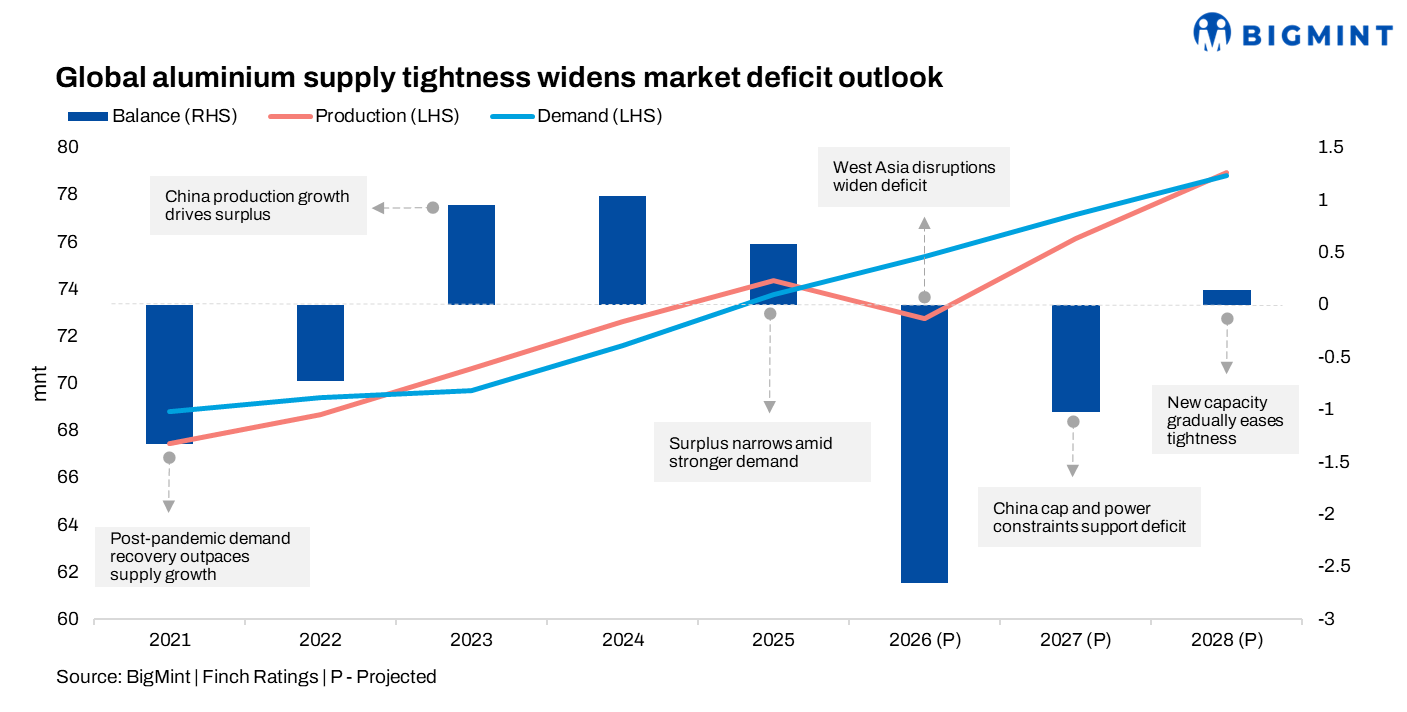

Global primary aluminium markets have tightened following supply disruptions in the Middle East, reducing the availability of metal in the seaborne market. With replacement supply remaining limited, aluminium prices have risen by around 20% since the onset of the Iran conflict in late February 2026. The higher price environment is expected to support stronger earnings and cash flows for regional producers capable of maintaining output while managing costs effectively.

Integrated operations provide a competitive advantage

Several major aluminium producers in the region have strengthened their financial profiles through improved profitability, higher commodity prices, and greater backward integration. Integrated operations continue to offer a competitive advantage, particularly during periods of supply disruption and raw material volatility.

Producers with integrated bauxite, alumina, and smelting operations remain less exposed to fluctuations in spot raw material markets. Long-term access to raw materials, coupled with increasing reliance on renewable and captive power sources, is helping reduce earnings volatility and improve cost competitiveness.

Stable alumina costs support smelter margins

Smelter economics are also benefiting from a favourable relationship between aluminium and alumina prices. While aluminium prices have increased significantly, alumina costs have remained relatively stable due to ample supply availability. Restrictions on new smelting capacity in China have helped keep alumina markets balanced despite intermittent operational disruptions.

Market participants expect China to maintain its 45 mnt cap on primary aluminium smelting capacity, given the sector's high power consumption and broader decarbonisation objectives. The combination of elevated aluminium prices and relatively softer alumina costs continues to support margins for integrated producers across the region.

Export demand remains a key growth driver

On the demand side, export-oriented manufacturing remains a key source of support despite softer domestic economic conditions in China. Strong growth in electric vehicle and automotive exports has helped offset weaker construction activity and slower consumer demand. During January-April 2026, China's electric vehicle exports increased by approximately 120% y-o-y, while automotive exports rose by over 60%.

Indonesia's expansion faces power constraints

Indonesia is expected to contribute additional aluminium supply in the coming years as several smelting projects progress. However, power availability remains a key constraint and could limit the pace of production growth through late 2026 and early 2027. In some industrial parks, electricity is already being reallocated from other metals operations to prioritise aluminium production, highlighting the challenges associated with expanding captive power capacity.

Outlook

Overall, tightening global supply conditions, stable alumina costs, and resilient export demand are expected to support strong margins and favourable operating conditions for APAC aluminium producers in the near term.