Taiwan starts carbon fee to cut emissions from key industries - will it succeed?

...

- Carbon fee may transition to cap-and-trade system in 2-3 years

- Levy to cover around 55% of country's carbon emissions

Taiwan is set to levy carbon fees this year, with three sub-laws expected to pass by August 2026. According to the country's Ministry of Environment, the carbon fee will operate on a "leading by example" approach and may shift to cap-and-trade in two to three years.

Two main criteria determine who will be subject to the carbon fee. First, the entity must be a regulated emission source registered and inspected by the government, such as power generation, steel, refining, cement, semiconductors, etc. Second, the entity's annual direct and indirect greenhouse gas emissions must reach 25,000 t of carbon dioxide equivalent.

Carbon fee coverage

The primary targets are electricity producers and manufacturers, with over 500 companies expected to be the first to be taxed, accounting for about 155 mnt of carbon emissions or 54% of the nation's total emissions.

The legal basis for Taiwan's carbon fee is the Climate Change Response Act. The phased collection of carbon fees aims to encourage businesses to transition to low-carbon operations, with preferential rates offered to accelerate this process.

The draft 'Voluntary Emission Reduction Plan Management Method' allows companies to apply for lower carbon fee rates by implementing emission reduction measures, such as switching to low-carbon fuels, improving energy efficiency, using renewable energy, upgrading processes, or adopting carbon-negative technologies.

Carbon leakage

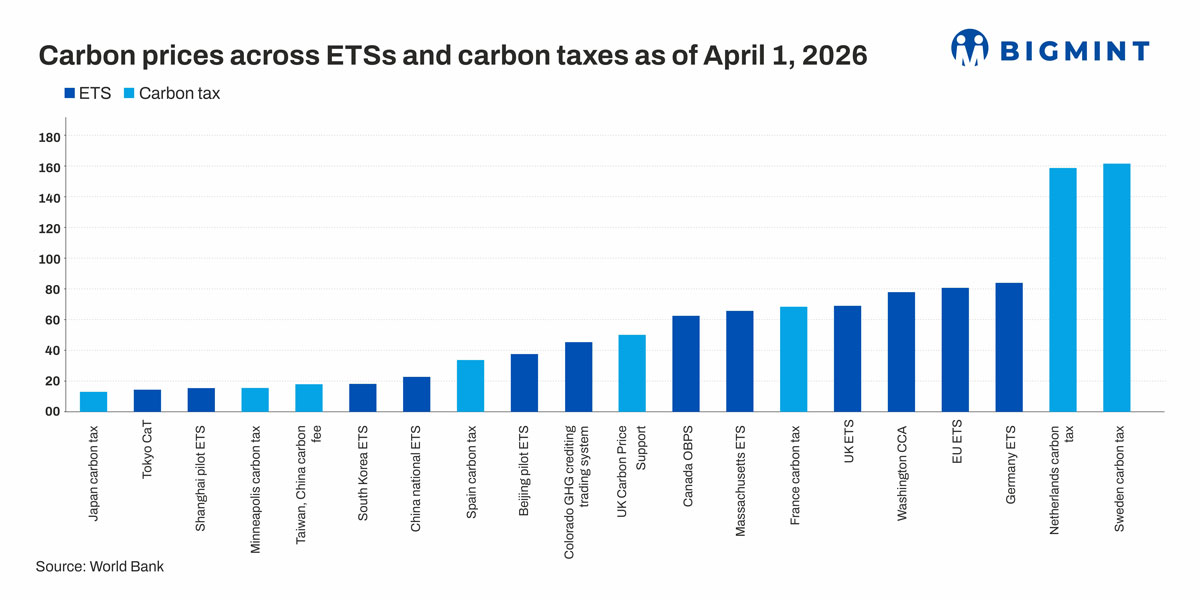

Initially, the government will set the 25,000-t threshold as the starting point, exempting emissions below this level from the fee. Based on discussions, the fee is expected to be set at NT$300/t.

For industries at high risk of carbon leakage, such as steel and cement, although they cannot deduct the 25,000-t free threshold, they can enjoy preferential rates of 20%, 40%, or 60% off depending on the timeline. This gradual adjustment is designed to prevent production lines from moving to other countries, which could increase global carbon emissions.

However, companies must first submit and receive approval for a voluntary reduction plan. If companies apply for the preferential rate, they must ensure that their voluntary reduction targets are met, or they will be required to pay the difference.

Apart from preferential rates, the government also suggests using reduction quotas to offset part of the carbon fee through the purchase of "voluntary carbon credits."

There are three ways to obtain reduction quotas domestically: "voluntary reduction projects," "offset projects," and "early action reduction quotas." Carbon credits obtained from "voluntary reduction projects" or "offset projects" can be multiplied by 1.2 times, but the deduction limit cannot exceed 10% of the total emissions subject to the fee.

For businesses not at high risk of carbon leakage, two other methods are available to offset emissions using carbon credits: using "early action reduction quotas" to offset emissions from 2024 to 2025, with the offset ratio reduced to 0.3, meaning 100 t of early action carbon credits can only offset 30 t of emissions; and using foreign carbon credits recognised by the central competent authority, with a deduction limit not exceeding 5% of the business's emissions subject to the fee.