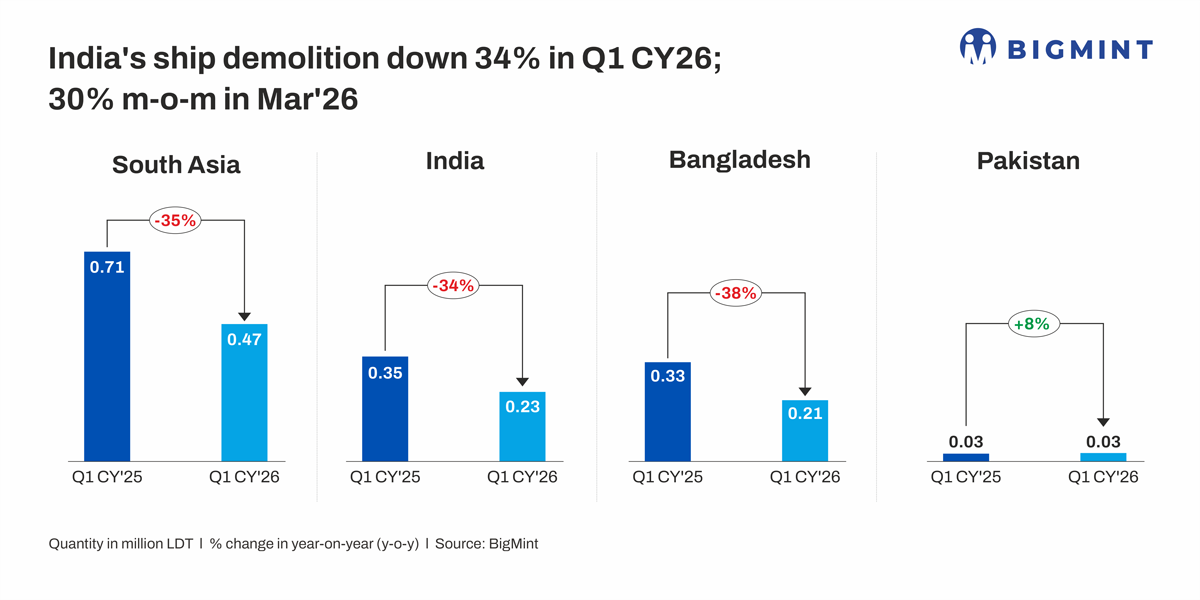

South Asian ship demolition tonnage falls 35% y-o-y in Jan-Mar'26 amid cost pressures, regulatory constraints

...

- Indian arrivals weaken by 34% amid high costs, currency pressure

- India's Alang sees increased arrivals of OFAC-sanctioned vessels

- Bangladesh volumes drop 38% due to regulatory, demand constraints

Morning Brief: Ship-recycling activity across South Asia remained under pressure in Q1CY'26, with total tonnage declining 35% y-o-y to 467,205 LDT from 713,300 LDT in the same period last year. The downturn was driven by comparable drops in Indian (-34%) and Bangladeshi (-38%) volumes and reflects unfavourable price economics and regulatory constraints.

Factors behind lower tonnage in Q1CY'26

Unfavourable pricing limits bookings: Higher dollar-denominated vessel prices impacted the buying appetite of ship breakers.

The ship recycling cycle -- from booking to actual cutting -- typically takes around 45-60 days or more, BigMint learnt from market participants. As a result, arrivals in Q1CY'26 largely reflect booking decisions made in earlier months, that is November-February, when market conditions were less favourable.

During November, domestic scrap prices at Alang were at around INR 30,600/t, while vessel prices near $400/light displacement tonne (LDT) translated to approximately INR 35,000-36,000/t, making procurement relatively expensive. The rupee remained weak, at around INR 88-89 per US dollar, and domestic steel demand was subdued, limiting price visibility and prompting cautious buying.

Similar pricing mismatches persisted through January and February 2026, resulting in lower vessel bookings and consequently reduced arrivals in subsequent months.

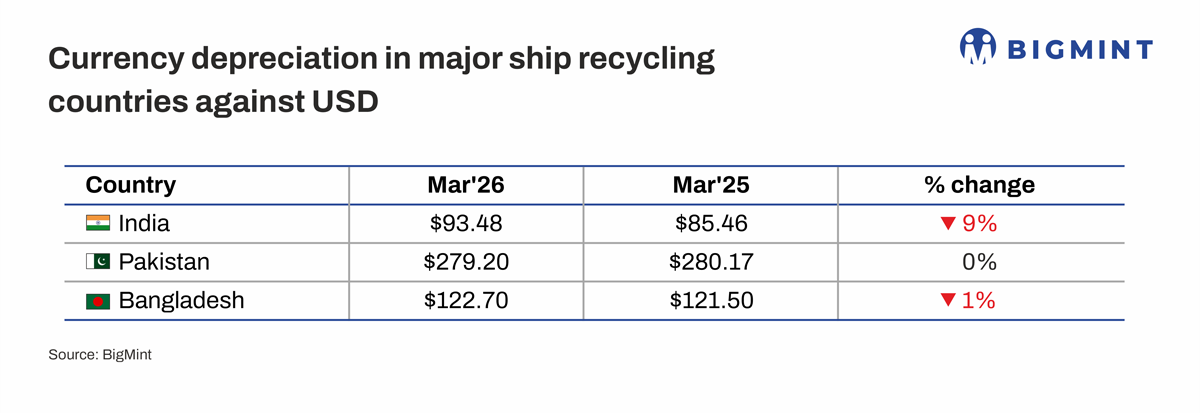

Currency depreciation has further impacted recyclers, particularly in India. The Indian rupee weakened by 5% y-o-y to INR 90.7 against one US dollar in January 2026. In March 2026, the depreciation was sharper, at 9% y-o-y to INR 93.5/US dollar, increasing the cost of vessel imports and limiting aggressive bidding.

HKC compliance hurdles slow down arrivals in Bangladesh, Pakistan: Bangladesh and Pakistan continued to face structural challenges, including regulatory constraints, weaker domestic steel demand, and limited financial flexibility.

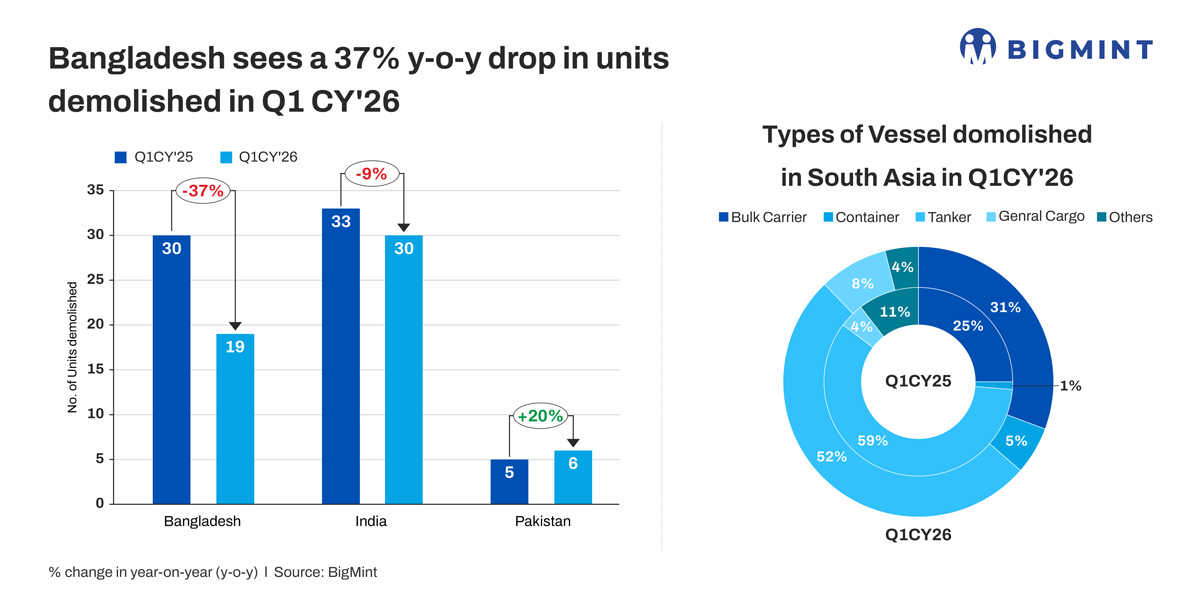

Bangladesh saw a sharp decline in both volumes and vessel count, with compliance issues with the Hong Kong Convention (HKC) and operational delays restricting yard activity. Pakistan, despite a marginal 8% rise in volumes due to selective buying, remained constrained by liquidity issues and currency volatility.

As of March 2026, only two yards are HKC-compliant in Pakistan. In Bangladesh, 25 of 100 yards have completed the required HKC upgrades.

In comparison, India continued to benefit from relatively stronger compliance standards, infrastructure, and operational readiness, helping it maintain its lead in the region.

Changing vessel composition

South Asia's recycling mix shifted notably in Q1CY'26. Tanker volumes declined sharply by 42% y-o-y, acting as the primary drag on overall activity, while bulk carrier volumes also fell 21% y-o-y.

In contrast, container vessel volumes surged significantly from a low base, supported by improved availability. General cargo vessels recorded moderate growth, while volumes in the others category dropped sharply.

Notably, a number of vessels sanctioned by the US Office of Foreign Assets Control (OFAC) were beached at India's Alang in the last quarter due to competitive prices. These vessels often sell for scrap at a lower price than "clean" ships, as they are blacklisted by the US and face restricted access to international ports, insurance, and financing. As such, their owners are often willing to offload them at a discount just to exit the market.

Generally, Indian ship-breakers avoid buying these vessels due to bank payment issues and compliance risk. However, lower prices have prompted ship breakers to increasingly turn to these.

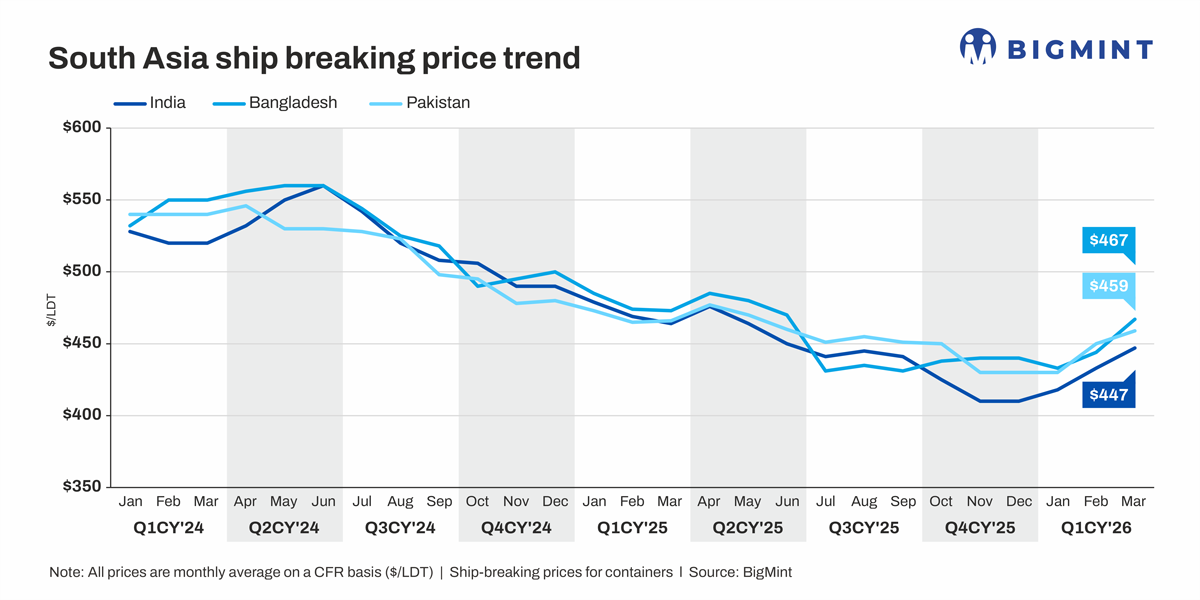

Prices across key recycling markets

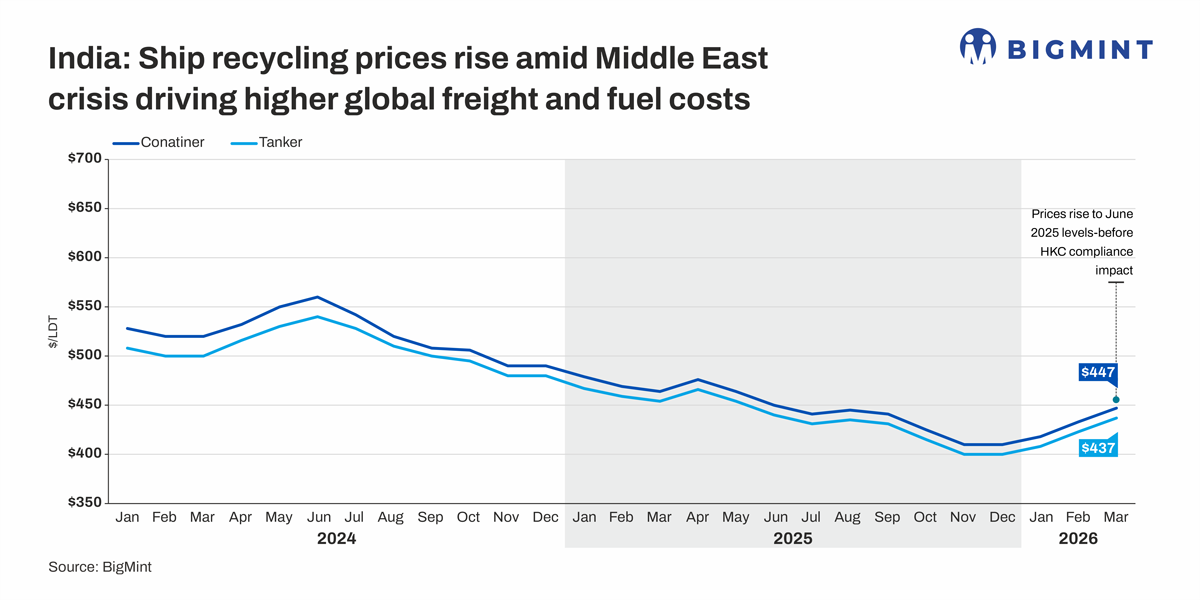

Ship-breaking prices fell y-o-y across all three South Asian markets. The decline was steeper in India, where container vessel prices decreased 8% y-o-y to a quarterly average of $433/LDT, while Bangladesh and Pakistan recorded corrections of 6% and 5% to $448/LDT and $446/LDT, respectively.

However, considering monthly prices, container vessel prices in South Asia showed a mild recovery in Q1CY'26, with India rising to $447/LDT in March from $418/LDT in January, supported by improved buying sentiment and limited vessel availability. Bangladesh and Pakistan followed similar trends, with prices rising to $467/LDT and $459/LDT, respectively, in March 2026, though still below earlier highs.

The Middle East crisis contributed to this recovery by pushing up global freight and fuel costs, thereby increasing the replacement costs.

Operational disruptions emerge in Mar'26 due to gas supply constraints

Gas shortages across South Asia, including India, have affected ship recycling operations by slowing cutting activity and reducing yard productivity. In India, intermittent gas supply has led to delays in processing and created operational inefficiencies at yards.

However, industry feedback indicates that gas shortages are not a primary factor influencing vessel arrivals or beaching volumes, as their impact is largely limited to the post-arrival processing stage rather than procurement decisions.

According to a market participant, "Ship-cutting activities are ongoing, as PNG supply is still being received. This has enabled recyclers to maintain operations, although at a slightly constrained pace."

Outlook

The Q2 outlook for South Asia's ship recycling market remains subdued. While recent price recovery and supply-side disruptions offer some support, underlying demand conditions remain weak.

India is expected to retain its leadership position, supported by better compliance and infrastructure. However, challenges such as high input costs, gas shortages, and tight liquidity are likely to keep sentiment cautious.

Bangladesh and Pakistan may continue to face slower inflows unless regulatory frameworks and financial conditions improve. Market participants also highlight that continued exclusion from the EU-approved list, potentially influenced by external pressures, may limit access to higher-quality vessels, thereby impacting long-term growth prospects for the region.

Ongoing tensions in the Middle East remain a key risk, as any escalation could further disrupt global trade flows, increase freight and fuel costs, and alter vessel availability dynamics, thereby reshaping the ship recycling market.