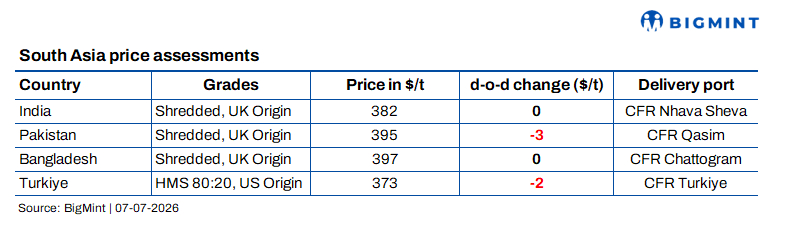

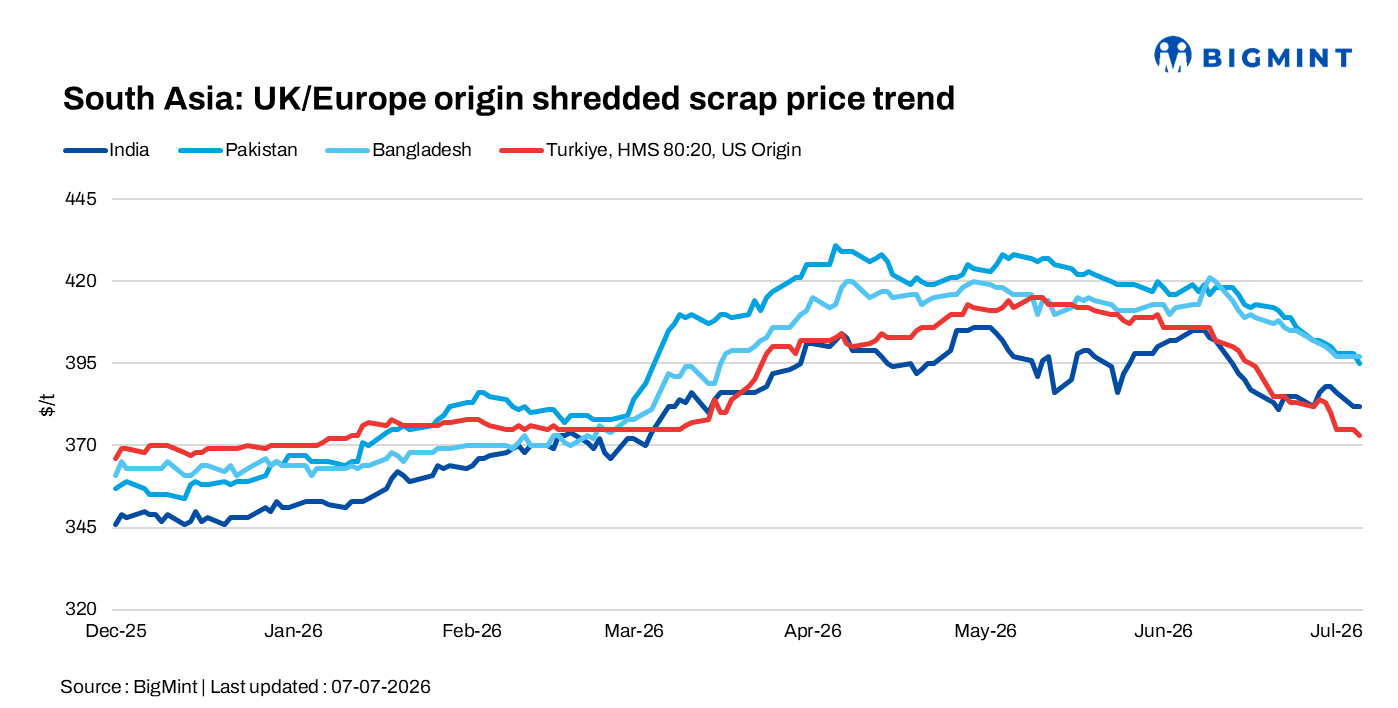

South Asia: Imported scrap prices remain range-bound; Turkish market holds steady

...

- India, Pakistan show need-based buying amid weak demand

- Turkish scrap prices stabilise as freight supports market floor

South Asia's imported ferrous scrap markets remained subdued on 7 July, as weak steel demand, poor import economics and cautious mill buying continued to limit fresh bookings across India, Pakistan and Bangladesh. Meanwhile, Turkish deep-sea scrap prices stabilised amid limited trading activity and higher freight costs.

India: Imported ferrous scrap market remained largely stable, with mills continuing to procure only against immediate requirements amid weak steel demand and poor import economics. Buying interest remained cautious, while offer activity was limited and no firm bids or trades for containerised shredded scrap were reported during the day.

Offer indications included Africa-origin LMS scrap at $290/t C&F Mundra (CAD) and Africa-origin HMS 80:20 at $330/t C&F Mundra (CAD). UK-origin shredded scrap was heard at $380-385/t CFR, although market participants said import viability remained weak despite expectations of softer offer levels.

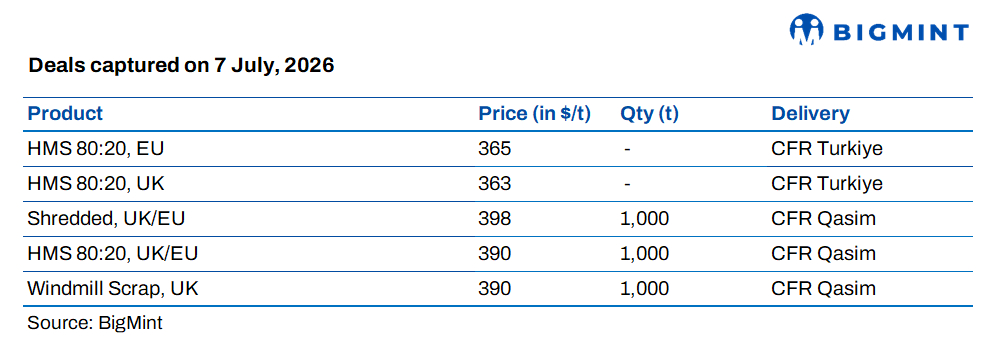

Pakistan: Imported shredded scrap market remained subdued, with buying limited to immediate requirements amid weak steel demand. Offer indications were heard at $398/t CFR Qasim for UK/EU-origin shredded scrap and $390/t CFR for both UK/EU-origin HMS 80:20 and GI bundles, reflecting cautious scrap procurement and sluggish market sentiment.

Bangladesh: Imported ferrous scrap buying remained muted as mills continued to delay fresh bookings amid weak steel demand and declining global scrap prices. UK-origin shredded scrap was heard at $400/t CFR Bangladesh, HMS 80:20 was workable at $360-365/t CFR, while LMS offers were reported at $300-305/t CFR. Rising electricity tariffs and revised tax measures continued to increase production costs, prompting mills to maintain a cautious procurement strategy.

Turkiye: Deep-sea imported ferrous scrap prices remained largely stable on 7 July as trading activity slowed at the start of the week, with limited participation from US and Baltic suppliers creating uncertainty over market direction. Higher freight rates also helped cap further downside, with some sellers indicating the market may have reached a price floor.

A deal for UK-origin HMS 80:20 was heard at $363/t CFR Turkiye for end-July shipment and another deal for Europe oigin was done at $365/t. Tradable values for US-origin HMS 80:20 were reported in the high $370-375/t CFR, while Rotterdam-Turkiye freight was assessed at $31-32/t, supporting sellers' pricing expectations.