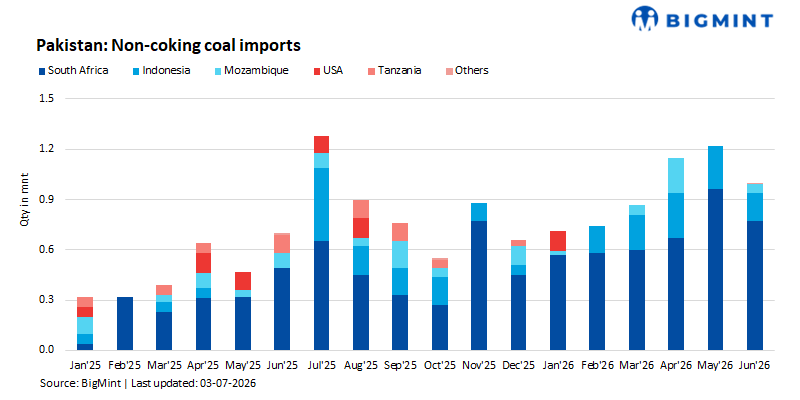

Pakistan's non-coking coal imports surge in H1 CY'26 led by South African supplies

...

- Q2 CY'26 imports surge on stronger buying

- South Africa dominates Pakistan's coal imports

Pakistan's non-coking coal imports from selected minor supplying countries remained firm during Q2 2026, despite a moderation in June arrivals. Imports stood at 1 million tonnes (mnt) in June, down 18% m-o-m from 1.22 mnt in May. However, shipments were 43% higher y-o-y compared with 0.7 mnt in June, indicating stronger import demand than a year earlier.

On a quarterly basis, imports increased to 3.37 mnt in Q2 2026, up 45.9% from 2.31 mnt in Q1, supported by higher cargo arrivals from South Africa, Indonesia and Mozambique.

During January-June, cumulative imports reached 7.87 mnt, compared with 6.36 mnt in year-ago period, registering a 23.7% y-o-y increase, reflecting improved coal procurement during the first half of the year.

South Africa remains Pakistan's dominant coal supplier

Pakistan's non-coking coal imports from South Africa moderated in June, with volumes declining 20% m-o-m to 0.77 mnt from 0.96 mnt in May. The monthly correction was primarily attributed to shipment timing differences, inventory adjustments by importers and relatively softer near-term procurement activity. Nevertheless, imports remained 57% higher y-o-y than 0.49 mnt in June, underscoring South Africa's continued importance in Pakistan's coal import basket.

Indonesian shipments also declined 35% m-o-m to 0.17 mnt from 0.26 mnt, reflecting lower cargo arrivals during the month. Mozambique recorded the sharpest monthly decline, with imports falling to 0.05 mnt from 0.21 mnt in May, partly due to reduced shipment arrivals and scheduling variations. Despite these monthly declines, South Africa retained its position as Pakistan's leading non-coking coal supplier.

During January-June 2026, Pakistan's non-coking coal imports from major origins increased significantly compared with the same period last year, supported by stronger import demand, competitive seaborne prices and greater diversification of supply sources. South Africa remained the largest supplier, with cumulative imports rising 143% y-o-y to 4.15 mnt from 1.71 mnt in Jan-Jun'25, reaffirming its dominant position in Pakistan's import market.

Indonesia recorded the strongest growth among the selected origins, with imports surging 494% to 1.07 mnt from 0.2 mnt in the corresponding period last year, reflecting a substantial increase in procurement during the first half of 2026.

Mozambique also showed improved performance on a quarterly basis, with Q2 imports increasing 225% q-o-q to 0.26 mnt from 0.08 mnt in Q1, indicating a recovery in cargo arrivals and stronger purchasing interest during the quarter. In contrast, exports from Mozambique dropped by 6% in H1 to 0.34 mnt as compared to corresponding period last year.

Limited imports from other suppliers

Imports from the USA remained negligible during the quarter. During Jan-Jun'26, cumulative imports from the USA declined 58.6% to 0.12 mnt from 0.29 mnt in the corresponding period last year. No imports were recorded from Tanzania during the first half of 2026.

Pakistan's non-coking coal imports strengthened during Q2 and the first half of 2026, supported by higher shipments from South Africa and a significant increase in imports from Indonesia. While June volumes eased from the previous month, overall import activity remained well above last year's levels.

Market sentiment and outlook

Pakistan's non-coking coal import market remained firm during the first half of 2026, supported by higher procurement from South Africa and Indonesia. Although imports declined on a month-on-month basis in June, stronger quarterly and half-year volumes indicate resilient demand from the domestic cement and power sectors.

Looking ahead, import volumes are expected to remain stable, with South Africa likely to retain its position as the leading supplier, while Indonesia may continue to expand its market share due to competitive pricing. However, procurement activity will continue to be influenced by international coal prices, freight rates, exchange rate movements, inventory levels and overall domestic industrial demand.