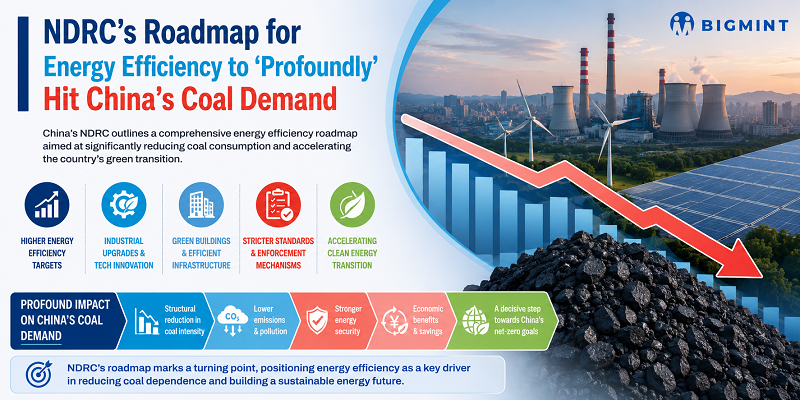

NDRC's roadmap for energy efficiency to 'profoundly' hit China's coal demand

...

- China's coal demand set to shift toward higher-grade as inefficient units exit

- Efficiency mandates may drive consolidation of Chinas coal power sector

Mysteel Global: The three-year campaign unveiled on Monday by China's top economic planning agency, the National Development and Reform Commission (NDRC), to boost energy efficiency in nine key industry sectors including coal-fired power generation will have a huge impact on coal demand and could prompt a structural realignment of coal consumption, according to industry analysts.

Among its many objectives, the 2026-2028 roadmap issued on June 15 by the NDRC and four ministries requires that facilities in the nominated industries operating below benchmark efficiency levels will be largely eliminated as the nation rushes to meet its 2030 climate goals, as Mysteel Global reported.

Retrofitting the country's vast coal-fired power fleet with mandatory targets on efficiency, flexibility and carbon intensity are central to the government's "dual carbon goals" -- namely, peaking carbon emissions by 2030 and achieving carbon neutrality by 2060.

Under the central government's plan, by the end of 2028 the share of coal power capacity meeting benchmark efficiency levels must rise by 15 percentage points, with all sub-benchmark units effectively eliminated. Market sources estimate the share was less than 30% by end-2025 as the government hasn't published specific data.

Last December, the NDRC had issued the 2025 edition of benchmark and baseline levels for clean and efficient coal use in key fields which set two levels for coal-usage projects: a high "benchmark" level for new and upgraded plants, and a basic "baseline" level that all existing plants must meet. Old plants that are below the baseline will have three years to upgrade or face shutdown, as Mysteel Global reported.

As for the coal power sector, the benchmark level is tiered based on unit class and measured by how many grammes of standard coal (7,000 kcal/kg NAR) are used to generate 1-kilowatt-hour of power. For example, for the ultra-supercritical 1,000-megawatt (MW) unit, the standard is set at 268-K g/kWh, where the k is a correction factor to adjust conditions such as coal quality, climate and altitude, while for the subcritical 600-MW unit it stands at 390-K g/kwh, Mysteel Global understands.

The campaign aims to generate cumulative energy savings exceeding 100 million tonnes of standard coal equivalent and cut carbon dioxide emissions by more than 200 million tonnes across all nine energy-intensive sectors, the document said. Besides coal-fired power, the others are steel, electrolytic aluminum, cement, flat glass, oil refining, ethylene, synthetic ammonia and methanol.

For coal power, which accounts for about 60% of China's total coal consumption, the plan imposes three distinct retrofit requirements.

First, energy-saving retrofits using turbine flow optimization, high-efficiency combustion and waste heat recovery must reduce coal consumption by at least 5 grammes of standard coal per kWh for commissioning units with capacity of 300-MW and above.

Second, flexibility upgrades for power-heat cogeneration plants in northern regions must achieve peak-shaving depth of 40% or less through thermal-electric decoupling, which means separating the power generation and heat supply functions in a bid to lower coal consumption and emissions.

Third, low-carbon retrofits through co-firing with biomass, coupling with renewables or adding energy storage must cut carbon emissions per kilowatt-hour by 10% to 20%, with a target of exceeding 20% for units with capacity of 300-MW and above.

Under this plan, larger, state-backed utilities with ample financial resources and advanced technology are well-positioned to meet the retrofit deadlines and expand their market share. In contrast, smaller, older plants -- often operated by private firms with limited capital and outdated equipment -- face a stark choice: either be acquired by bigger peers or risk closure if they cannot afford the required upgrades, analysts noted.

The policy also has a profound impact on coal demand, analysts said. While the overhaul focuses on upgrading existing units rather than mass closures -- and so prevent an immediate demand collapse -- the medium-term effect is a structural realignment of coal consumption.

The phase-out of inefficient sub-benchmark units -- typically smaller 300-MW-or-below plants that burn low-calorific, high-ash, high-sulfur coal -- will steadily shrink demand for lower-grade fuel. In contrast, retrofitted ultra-supercritical and high-efficiency units require higher-quality coal, particularly 5,500 kcal/kg and above, boosting premiums for premium domestic output and overseas shipments from Australia and Russia. The gap between high- and low-grade coal prices is expected to widen considerably.

Beijing has paired the mandates with financial incentives and penalties to ensure compliance. Eligible retrofit projects will receive central government subsidies covering 20% of approved total investment, with priority for projects achieving benchmark efficiency levels, as reported. At the same time, units failing to meet standards by the 2028 deadline will face surcharges of up to Yuan 0.1/kWh on market electricity prices -- a significant cost penalty in China's competitive power market -- and ultimately risk forced closure.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.