Mapping Indian cement industry's sustainability parameters and the road ahead - BigMint report

...

- Indian cement sector among best globally in energy consumption

- Domestic industry's clinker ratio far lower than global average

- RE and biofuels, blended cements, CCUS key decarbonisation levers

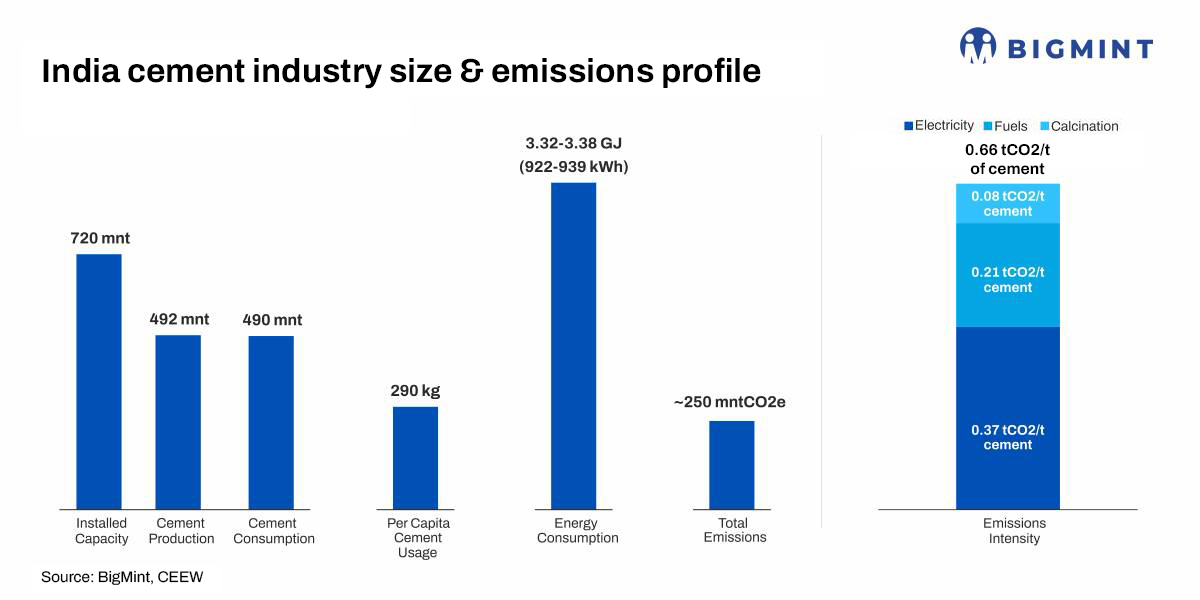

Morning Brief: The Indian cement industry is growing at a phenomenal pace, and production has increased sharply by 50% since FY'20. India produced around 492 million tonnes (mnt) of cement in FY'26 and total installed capacity has exceeded 700 mnt. With GDP growth at around 7%, rapid urbanisation, housing and infrastructure development will push cement consumption many notches higher in the coming decades.

The energy-intensive concrete and cement sector accounts for 7% of global emissions. In 2023, cement manufacturing contributed roughly 2.4 GtCO2e of Scope 1 and 2 emissions worldwide, according to Global Concrete & Cement Association (GCCA). The Indian cement sector accounts for annual emissions of over 250 mntCO2e.

Emissions intensity

The global average emissions intensity of 1 tonne of cement production is around 0.6 tCO2/t, and the carbon intensity of the Indian industry is almost at a similar level. Research conducted by the Council on Energy, Environment & Water (CEEW) shows that the average emissions intensity of the Indian cement sector stands at around 0.66 tCO2/t of cement.

Nearly 56% per cent of the total 0.66 tCO2 is produced due to the calcination of limestone in kilns. Most of the remaining 32% of emissions is due to the combustion of fuels for process heating applications, while only a small portion 12% precisely is due to the electricity used for manufacturing.

Technological maturity

The Indian cement industry is technologically mature. Many cement plants in India now operate at energyefficiency levels comparable to the best performers worldwide. This has been achieved through investment in modern equipment and better plant operation. The wider use of highefficiency kilns with preheaters and precalciners has reduced the energy required per tonne of cement, helping cut fuel use and emissions.

Adoption of state-of-art technology is due to the fact that the domestic cement industry is a relatively young one, with the major chunk of its capacity being added after 2005. Many domestic producers have also voluntarily adopted ISO 50001, which ensures implementation of structured, systematic and continuous improvements in energy efficiency.

The Indian industry's specific energy consumption (SEC) in terms of thermal and electricity energy stands at par with the global best. Same goes for clinker ratio, which in India is around 67.5% compared with the global average of 75%.

The domestic industry has gradually transitioned to greener variants of Ordinary Portland Cement (OPC). Increased production of Portland Pozzolana Cement (PPC) and Portland Slag Cement (PSC) has contributed to CO2 reductions and circularity. CRISIL data shows that production of blended cement (PPC + PSC + composite) stood at 76-78%, while OPC had a share of 20-22%.

CO2 mitigation

A NITI Aayog study claims that cement sector emissions in India are projected to rise to over 1.32 bnt by 2070 in a BAU case. The main levers identified for a net-zero pathway are:

- Alternative fuels

- Decarbonisation of electricity

- Adopting substitute or supplementary cementitious material

- CCUS

Of these, while CCUS is still some way off, it is expected to deliver the highest rate of emissions mitigation at 35-54% by 2070. The usage of Municipal Solid Waste (MSW) is calculated at around 4% in the domestic cement industry and that proportion may increase due to efficient sorting, segregation and logistics.

Usage of supplementary cementitious materials (SCM) like hydraulic (granulated blast furnace slag) and pozzolanic (calcined clay) materials and bio-ash can boost circular economy and helps in effective waste management. This is expected to deliver overall emissions reductions of 11-15% till 2070. The clinker to cement ratio in India is approximately 67.5% currently and it can go to approximately 62%, according to NITI Aayog.

However, existing standards may not adequately support widespread adoption of clinker substitutes due to specific prescribed composition of cements. Industry bodies have appealed to the government for BIS to set adequate standards for adoption of blended cements and clinker substitutes.