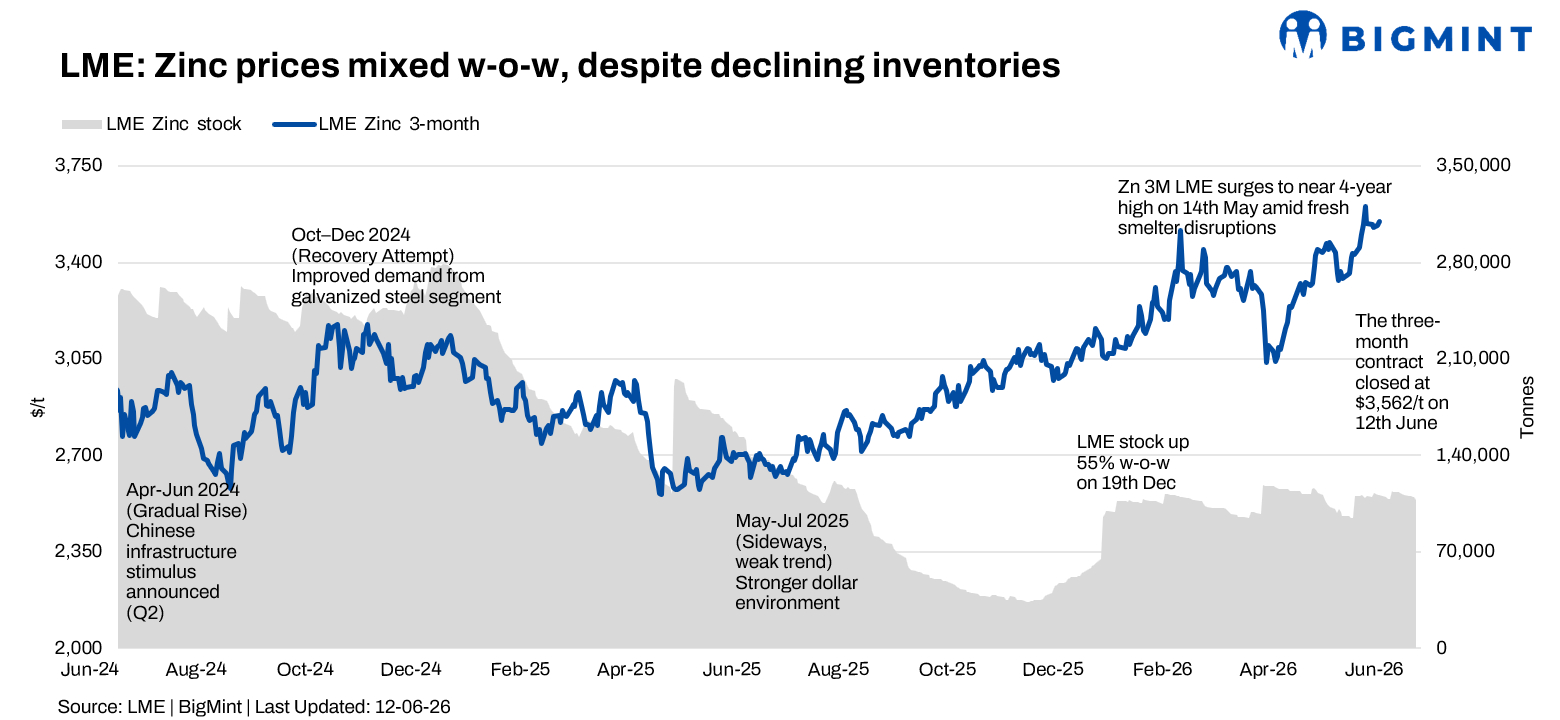

LME zinc remains under pressure w-o-w despite inventory decline

...

- Prices inch down w-o-w despite demand recovery towards weekend

- SHFE zinc closes lower amid uncertain Chinese demand outlook

London Metal Exchange (LME) zinc prices witnessed heightened volatility during the week ended 12 June 2026 as market participants weighed shifting macroeconomic sentiment against tightening exchange inventories. While prices corrected sharply during the middle of the week, a strong recovery towards the close helped zinc finish above key support levels, reflecting continued underlying market resilience.

On a w-o-w basis, LME zinc cash prices eased marginally by around 0.5% from $3,575/t recorded on 5 June, reflecting a correction after recent gains while remaining at historically elevated levels.

Price trends

LME zinc cash settlement prices opened the week at $3,519/t on 8 June and strengthened to $3,576/t on 9 June amid improved buying interest and supportive sentiment across the base metals complex.

However, the market came under pressure during the following sessions, with cash settlement prices declining to $3,486/t on 10 June and further to a weekly low of $3,468/t on 11 June as participants engaged in profit-booking following the previous week's rally.

Buying interest resurfaced towards the close, lifting cash settlement prices to $3,557/t on 12 June.

The three-month contract followed a similar trend, opening at $3,534/t on 8 June, rising to $3,588/t on 9 June before falling to a weekly low of $3,483.5/t on 11 June. The contract recovered to settle at $3,562/t on 12 June. Despite the correction, the forward curve remained relatively firm, indicating continued confidence in near-term zinc fundamentals.

Inventory analysis

LME zinc inventories continued their downward trajectory during the week, providing underlying support to market sentiment.

Stocks declined from 110,950 t on 5 June to 110,650 t on 8 June and further to 110,400 t on 9 June. Inventory drawdowns accelerated during the latter half of the week, with stocks falling to 109,575 t on 10 June, 109,475 t on 11 June, and finally to 107,750 t on 12 June.

Overall, exchange inventories declined by 3,200 t during the reporting week, highlighting tightening visible supply and reinforcing expectations of balanced market conditions despite price volatility.

MCX zinc trends (8-12 June)

On the Multi Commodity Exchange (MCX), zinc futures traded within a broad range during the week, mirroring movements on the LME.

The June contract settled at INR 365,200/t on 8 June before edging higher to INR 365,500/t on 9 June. Selling pressure emerged on 10 June, dragging prices down to INR 359,350/t.

The market subsequently recovered, with prices advancing to INR 364,750/t on 11 June and further to INR 368,800/t on 12 June, marking the highest close of the week.

Open interest remained relatively stable throughout the reporting period, rising from 2,511 lots on 8 June to 2,603 lots on 9 June before easing slightly and closing at 2,544 lots on 12 June. The movement suggests continued market participation, with fresh buying interest emerging towards the week-end recovery.

Trading activity remained healthy as domestic consumers largely maintained need-based procurement amid elevated zinc prices and adequate availability of domestic material.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), zinc prices displayed mixed trends during the week.

SHFE zinc stood at $3,566/t on 8 June before easing to $3,550/t on 9 June and $3,539/t on 10 June amid cautious sentiment in the Chinese market.

Prices rebounded sharply to $3,638/t on 11 June as buying momentum improved. However, the market witnessed a significant correction on 12 June, with prices declining to $3,450/t.

The volatile movement indicates uncertainty surrounding near-term Chinese demand conditions, although elevated price levels continue to reflect generally supportive market fundamentals.

Outlook

BigMint expects LME zinc prices to remain largely stable in the near term as declining exchange inventories and relatively balanced supply-demand fundamentals continue to provide support. However, elevated price levels and cautious downstream purchasing activity may restrict aggressive upside momentum.

Prices are likely to find support in the $3,450-3,500/t range, while immediate resistance is seen around $3,600-3,650/t.