LME base metals rise on supply-side cues; oil swings as geopolitical signals remain mixed

...

- Nickel-led gains lift base metals as inventories tighten across the complex

- Oil softens on easing geopolitical tone, though Hormuz risks keep volatility intact

Base metals prices on the London Metal Exchange (LME) closed largely higher d-o-d on 14 Apr'26, with most metals registering gains except aluminium. Nickel led the upside, rising 2.87% to $18,206/t, followed by copper up 1.77% to $13,284/t, zinc up 0.75% to $3,342/t, and lead gaining 0.68% to $1,935/t. In contrast, aluminium declined 1.22% to $3,563/t.

Inventory trends were largely on the downside across base metals, indicating tightening availability. Aluminium stocks fell 0.51% to 397,100 t, nickel inventories declined 0.45% to 280,392 t, zinc stocks edged lower by 0.13% to 111,775 t, and lead inventories dropped 0.32% to 277,325 t. Copper was the only exception, with stocks rising 1.63% to 399,150 t, reflecting relatively higher exchange inflows.

Domestic market overview

India's non-ferrous scrap market witnessed a firm trend d-o-d, reflecting improved buying interest. Aluminium tense scrap (loose), ex-Delhi, increased to INR 289,000/t, up by INR 6,500/t or 2.3% from INR 282,500/t. Similarly, ex-Chennai prices rose to INR 297,000/t, gaining INR 4,000/t or 1.4% from INR 293,000/t, indicating stronger regional demand.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, also edged higher to INR 1,135,000/t, up by INR 6,000/t or 0.5% from INR 1,129,000/t, reflecting steady-to-firm buying activity in the market.

Other market updates

LME Nickel Rallies on Indonesia Policy support

LME nickel prices surged on 15 April, with 3M futures rising $508/t to $18,206/t and spot prices up $501/t to $17,981/t, supported by strong macro and policy cues.

The rally was driven by Indonesia's revised ore pricing mechanism, which lifted raw material costs, alongside a weaker US dollar and easing inflation pressures in the US.

Additionally, declining LME inventories, down 1278 t to 280392 t, and improving macro indicators in China further supported sentiment.

Near-term outlook remains firm, with price direction dependent on macro developments and geopolitical cues.

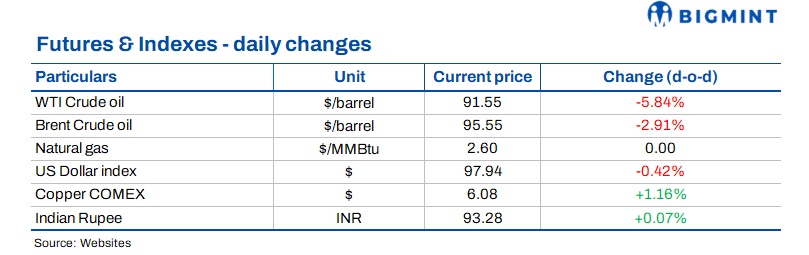

Oil prices fall for second day on US-Iran talks optimism

Oil prices declined for a second consecutive session on 15 April, pressured by expectations of renewed US-Iran negotiations that could ease supply disruptions.

Brent crude traded near $95/bbl, while WTI hovered around $91/bbl, as markets factored in potential resumption of flows from the Middle East.

The downside was driven by improving diplomatic sentiment, with talks likely to resume in Pakistan, raising hopes of easing sanctions and reopening supply channels.

However, volatility persists as the Strait of Hormuz remains largely restricted, keeping supply uncertainty elevated despite optimism around negotiations.

Sanctioned tanker turns back in Hormuz amid US blockade

A US-sanctioned tanker, Rich Starry, reversed course in the Strait of Hormuz after failing to breach the newly imposed US blockade on Iran-linked vessels.

The move came within 24 hours of the blockade, during which no ships were able to pass, with at least six vessels complying with orders to turn back.

The disruption highlights escalating maritime restrictions and rising uncertainty for global oil trade, shipping routes, and insurance markets amid ongoing geopolitical tensions.

US-Iran seek further talks amid Hormuz blockade

The US and Iran are exploring a second round of ceasefire talks in the coming days, even as tensions escalate in the Strait of Hormuz, a key global oil transit route.

The ongoing US-led blockade has disrupted shipping flows, worsening the global energy crisis and complicating diplomatic progress despite initial negotiations held in Pakistan.

Markets remain volatile as the standoff continues to restrict oil movements, with any breakthrough in talks seen as critical for easing supply concerns and stabilising prices.