LME base metals gain amid mixed fundamentals; oil prices stay elevated as geopolitical uncertainty persists

...

- Base metals rise on LME; mixed inventory trends signal uneven demand

- Oil prices fall sharply; Middle East tensions keep markets volatile

Base metals prices on the London Metal Exchange (LME) closed largely higher d-o-d on 13 April 2026, with most metals gaining except zinc, while lead remained flat. Aluminium rose 3.12% to $3,607/t, nickel increased 2.65% to $17,698/t, and copper gained 1.62% to $13,053/t. In contrast, zinc declined 0.48% to $3,317/t, while lead remained unchanged at $1,922/t.

Inventory trends were mixed across base metals. Aluminium stocks declined 0.62% to 399,150 t, zinc inventories fell 0.11% to 111,925 t, and lead stocks decreased 0.20% to 278,225 t. Meanwhile, nickel inventories edged up 0.13% to 281,670 t, and copper stocks rose 2.43% to 392,750 t, indicating relatively higher exchange availability.

Domestic market overview

India's non-ferrous scrap market witnessed a mixed trend d-o-d, reflecting moderate demand conditions. Aluminium tense scrap (loose), ex-Delhi, increased to INR 282,000/t, up by 0.71% from the previous day. Similarly, ex-Chennai prices rose to INR 292,000/t, registering a 0.34% gain d-o-d, indicating marginal improvement in regional demand.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, remained stable at INR 1,129,000/t, unchanged from the previous day, pointing to steady buying interest in the market.

Oil markets remain volatile amid geopolitical uncertainty

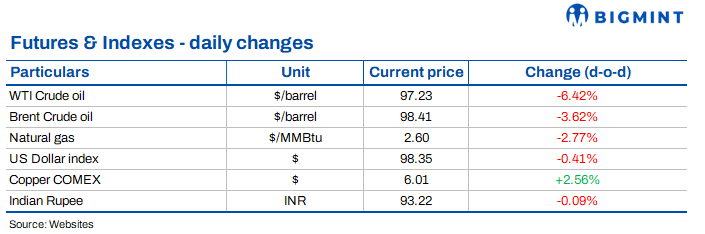

While oil prices recorded a notable decline, with Brent crude falling by 3.62% to $98.41/bbl, prices still remain sharply elevated compared to prices before the US-Iran conflict began. Natural gas prices also declined by 2.77% to $2.60/MMBtu.

Global oil markets remain volatile amid ongoing Middle East tensions impacting both supply and sentiment. While potential US-Iran dialogue offers some hope for de-escalation, disruptions such as port blockades and constrained trade routes continue to tighten supply conditions.

At the same time, cautious demand signals and trading uncertainties are adding to market instability, keeping oil prices highly sensitive to geopolitical developments and shifting sentiment.

Middle East tensions drive volatility across energy, currency, and inflation outlook

Ongoing Middle East tensions continue to create mixed signals across global markets, impacting currencies, inflation outlook, and energy supply dynamics. The safe-haven US dollar weakened amid expectations of a potential diplomatic breakthrough between the US and Iran, even as actual energy flows remain constrained due to port blockades and restricted Gulf shipments.

At the same time, concerns over an energy shock driven by the conflict have prompted central banks such as Singapore to tighten monetary policy, highlighting rising inflation risks alongside slowing economic growth. While disruptions to oil supply persist, market sentiment is being supported by cautious optimism around renewed negotiations, keeping volatility elevated across commodities and financial markets.