Japan's ferrous scrap exports decline in Q1CY'26 amid tighter supply, higher prices

...

- Export prices climb up, reducing competitiveness of Japanese scrap

- Vietnam turns to alternative suppliers, reducing imports from Japan

- Bangladesh imports rise due to short sailing times, quality preferences

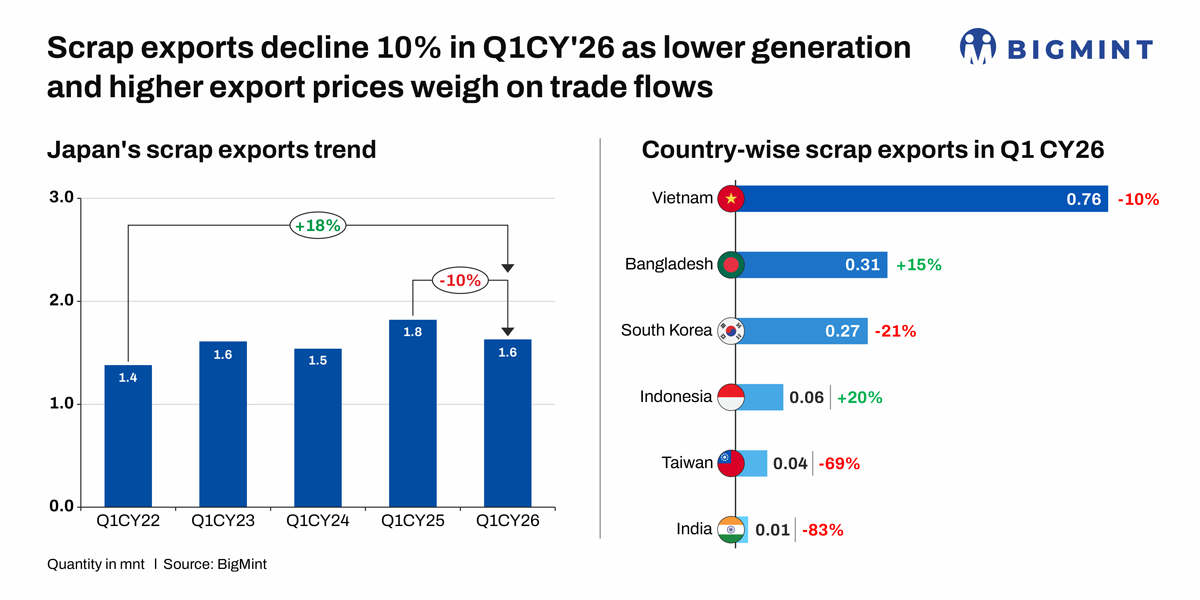

Morning Brief: Japan's ferrous scrap exports declined 10% y-o-y to 1.6 million tonnes (mnt) in Q1CY'26 from 1.8 mnt in the corresponding period last year, according to data compiled by BigMint. While scrap generation declined, demand from traditional importers such as Vietnam, South Korea, Taiwan, and India weakened as export prices remained high.

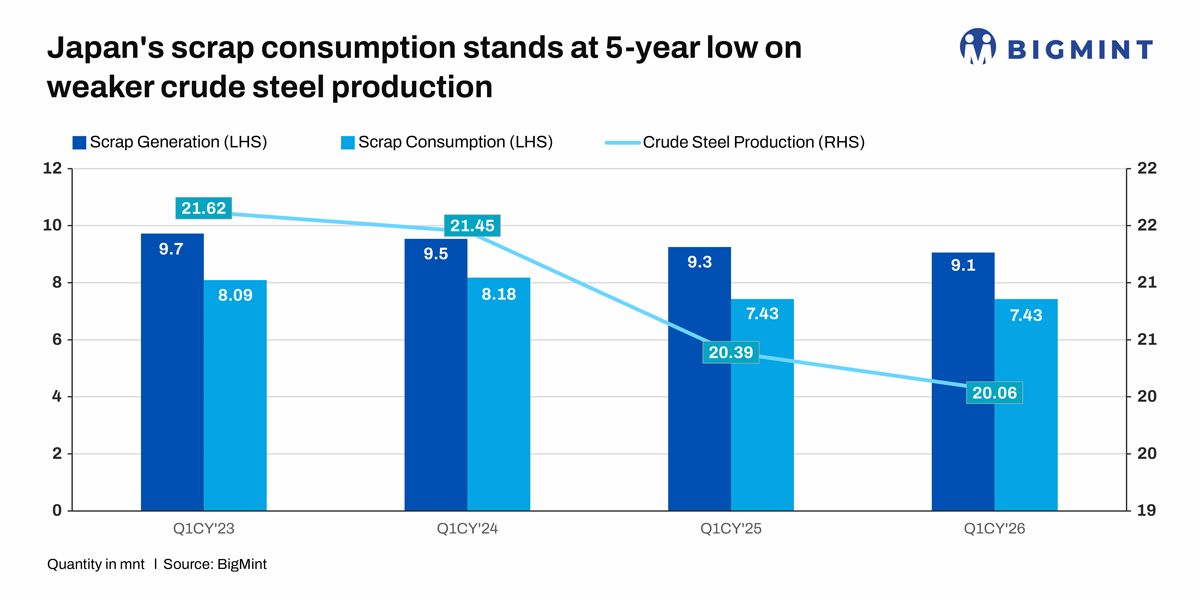

Notably, Japan is one of the largest exporters of high-quality ferrous scrap (H2 and premium grades such as HS and Shindachi) to Asia, particularly to Vietnam, Bangladesh, and South Korea. The country's exports hit a five-year high of around 7.5 mnt in CY'25, up 19% y-o-y, as crude steel production fell 4% y-o-y to 80.7 mnt, a 57-year low last seen in 1968.

Why Japan's scrap exports fell

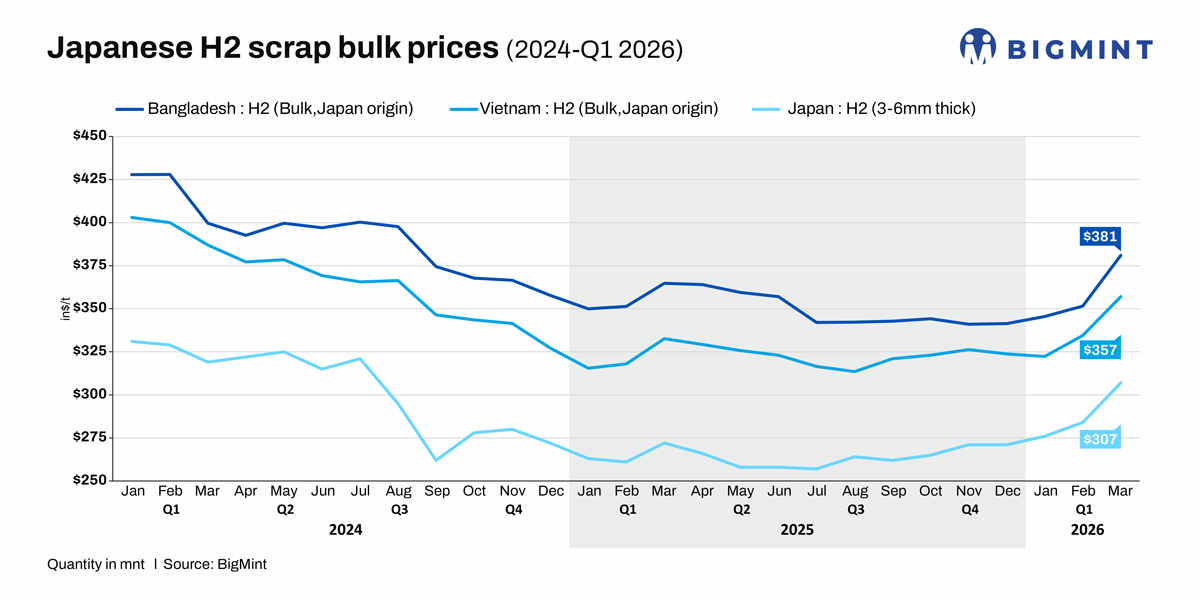

Japanese H2 scrap prices averaged $289/t FOB Tokyo Bay in Q1CY'26, up from $265/t in Q1CY'25, according to BigMint's assessments. The price increase was supported by tighter domestic scrap availability, steady consumption, and continued demand from Bangladesh and Southeast Asian buyers.

Domestic mills also remained active in the spot market, competing with export buyers for available material and helping keep Japanese scrap prices elevated. However, stronger prices reduced the competitiveness of Japanese scrap against alternative origins. Buyers in several markets, already grappling with weak finished steel demand and rising shipping costs, became increasingly cautious, leading to slower booking activity.

The decline in exports was not solely demand-driven. Japan's crude steel production fell to 20.06 mnt in Q1CY'26 from 20.39 mnt a year earlier, while scrap generation declined to 9.1 mnt from 9.3 mnt. Domestic scrap consumption, meanwhile, remained largely stable at 7.43 mnt.

The reduction in scrap generation outweighed the decline in steel output, tightening the pool of exportable material. With domestic consumption remaining stable and Japanese mills continuing to compete for scrap procurement, less surplus material was available for export despite supportive overseas prices.

Country-wise importers

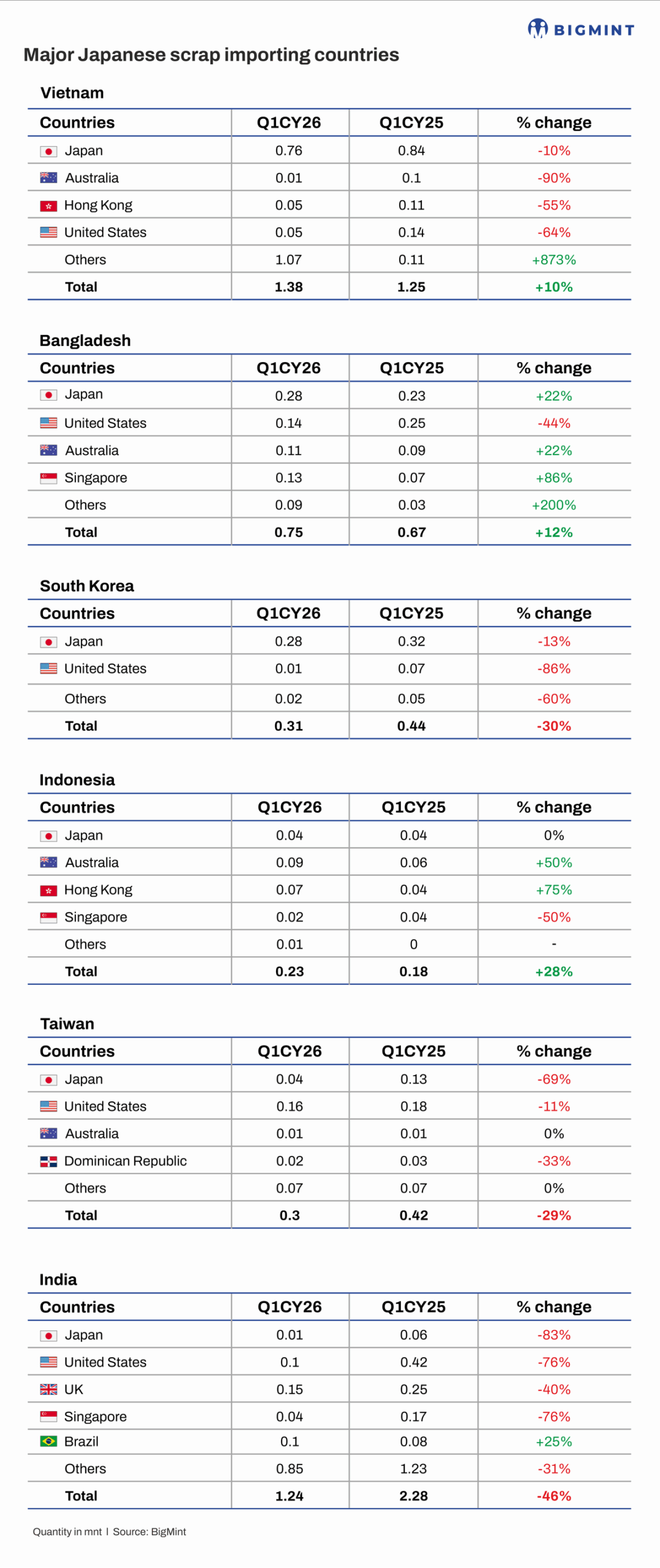

Vietnam remained Japan's largest export destination, accounting for nearly half of total shipments. However, imports declined 10% y-o-y to 0.76 mnt as buyers diversified sourcing and maintained cautious procurement strategies amid volatile steel market conditions. Rising Japanese export prices encouraged some Vietnamese buyers to evaluate alternative suppliers, particularly when finished steel margins remained under pressure.

South Korea's imports fell 21% y-o-y to 0.27 mnt from 0.34 mnt in Q1CY25, while Taiwan's purchases plunged 69% to just 0.04 mnt. Weak steel demand, elevated inventories, and cautious mill buying continued to suppress import requirements in both markets.

India recorded the sharpest decline among major destinations, with imports from Japan dropping over 80% y-o-y from 0.06 mnt to only 0.01 mnt. Weak imported scrap demand, poor steelmaking margins, and the availability of lower-priced alternatives significantly curtailed buying activity throughout the quarter.

Bangladesh, Indonesia provide support

While traditional northeast Asian buyers reduced purchases, demand from Bangladesh and Southeast Asia helped cushion the decline. Bangladesh emerged as the standout growth market during the quarter, with imports of Japanese scrap increasing 15% y-o-y to 0.31 mnt. Competitive freight costs, shorter sailing times, and the reliable availability of Japanese cargoes continued to support buying interest.

The country's growing significance was further reflected in the Kanto Tetsugen export tenders. Bangladeshi buyers secured all three monthly H2 cargoes offered during Q1CY'26. A 20,000-t cargo was awarded in January at JPY 46,771/t FAS, followed by another 20,000 t cargo in February at JPY 48,083/t FAS and a further 20,000 t cargo in March at JPY 50,121/t FAS. The successive awards highlight sustained demand despite rising Japanese export prices.

Indonesia also recorded stable buying interest, with imports increasing 20% y-o-y as expanding EAF-based steelmaking capacity and infrastructure-related steel consumption continued to support raw material requirements.

Outlook

Japan's export market is expected to remain supported by steady demand from Bangladesh and Southeast Asia, particularly Indonesia and Vietnam, where EAF-based steelmaking capacity continues to expand.

At the same time, Japan is preparing to increase domestic availability of high-grade scrap under its Green Transformation (GX) steel strategy. The initiative aims to support future green steel production exceeding 3 mnt annually through investments in AI-based sorting technologies, advanced shredding facilities, and recycling infrastructure. As Japanese steelmakers gradually expand EAF-based production and decarbonisation initiatives, competition for premium scrap grades could intensify, potentially increasing domestic retention of material that has traditionally been available for export.

While Japan is expected to remain a key regional scrap supplier, weaker demand from northeast Asia and tighter domestic scrap availability are likely to limit export growth in the near term. As a result, Bangladesh and Southeast Asian markets are expected to play an increasingly important role in shaping Japan's scrap trade flows going forward.