India's met coke imports expected to climb to multi-year high in CY'26 - BigMint analysis

...

- Landed costs of imports remain lower despite anti-dumping duty

- High ash content of domestic coke reduces steelmaking efficiency

Data Deep Dive: India's metallurgical coke imports are expected to reach a multi-year-high in calendar year 2026 (CY'26) as overseas material, particularly from Indonesia, continues to offer cost and quality advantages over domestic supply, even after imposition of anti-dumping duties.

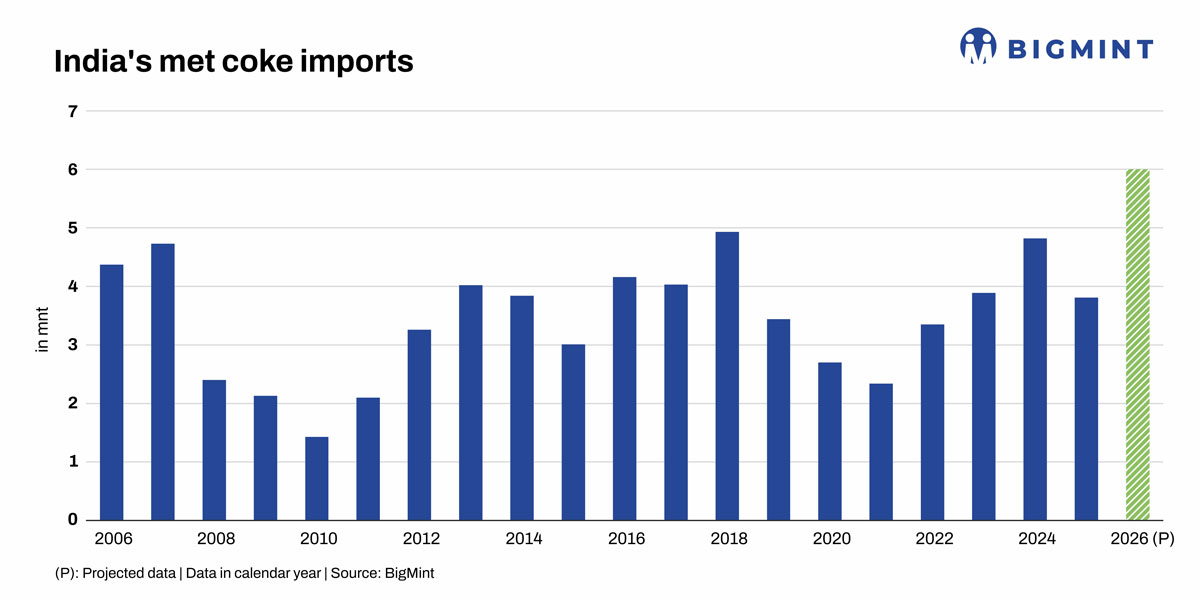

India imported 2.2 million tonnes (mnt) of met coke during January-April 2026, up sharply from 1.3 mnt in the corresponding period last year, according to data maintained by BigMint. At the current pace of roughly 0.5 mnt per month, total imports could reach nearly 6 mnt in CY'26, the highest since BigMint started recording volumes in CY'06.

In comparison, imports had reached 3.81 mnt in CY'25, falling by 21% y-o-y, constrained due to imposition of quantitative restrictions on low-ash met coke from 11 major suppliers. However, the sharp rebound in early 2026, immediately following the withdrawal of the import quotas, suggests underlying demand for imports remains strong.

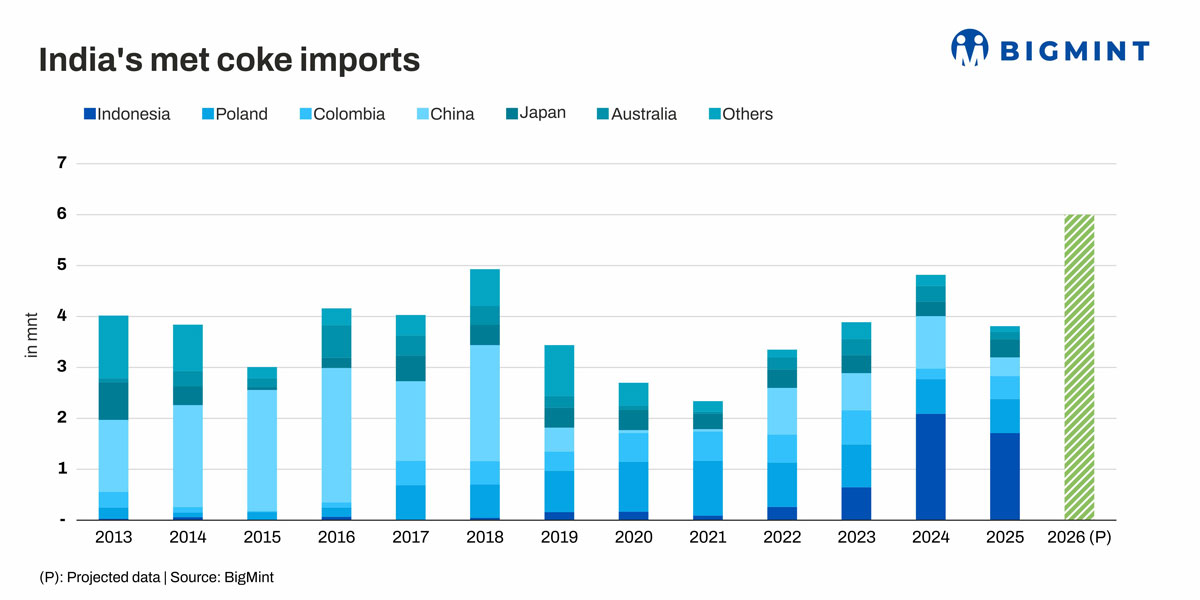

The surge has been led overwhelmingly by Indonesia, with shipments tripling to 1.6 mnt in January-April from 0.5 mnt a year earlier. Other key suppliers included Poland, Colombia, Japan, and the US.

Indian hot metal production, which rose at a compound annual growth rate (CAGR) of 5.9% during CY'20-25, and pellet output, which rose at 8.45% CAGR over the same period, have significantly outpaced met coke production growth at 3.05% CAGR. This has raised the question whether domestic supply will be able to fully meet consumption requirements.

"India, overall, is a met coke deficit country and will need coke imports to catch up with finished steel production targets set by the government," an executive at a global trading firm said. The Indian steel industry accounts for roughly 75% of met coke requirement. Low-ash met coke, which forms the bulk of imports, is used exclusively in the steelmaking process.

Cost advantage sustains imports

The biggest factor supporting the surge in imports over January-April has been the widening price gap between domestic and imported coke. Met coke comprises around 35-40% of steel production costs in the blast furnace-based steelmaking route.

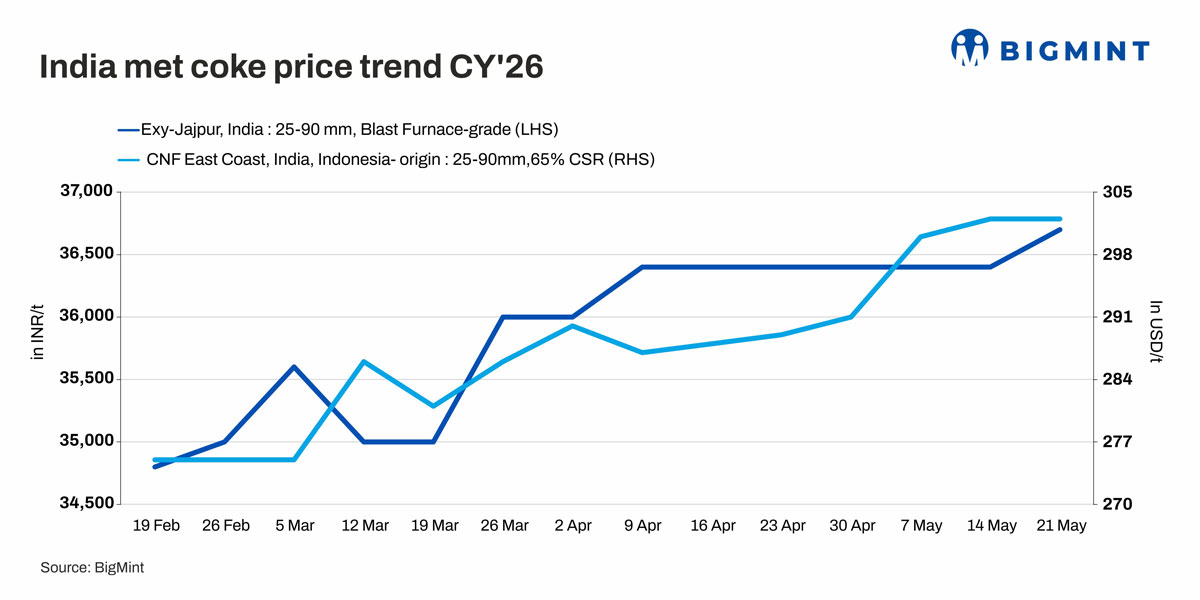

Domestic met coke prices in eastern India rose from around INR 32,000/tonne (t) ex-works Jajpur at the end of December to INR 36,000/t by end-March, marking an increase of about 13%.

In contrast, Indonesian low-ash met coke offers increased at a slower pace, rising to $290-295/t CFR India by end-March from $270-275/t at the start of January. Market participants said the landed cost of imported coke remained cheaper than domestic material even after accounting for logistics and financial charges.

On 26 May, BigMint assessed the landed cost of Indonesian met coke (25-90 mm, 65% CSR), taking into account the anti-dumping duty of $67.50/t, at around INR 36,300/t CFR India excluding freight charges. In comparison, domestic blast-furnace met coke (25-90 mm) was at INR 36,700/t exy-Jajpur and INR 33,500/t exy-Gandhidham.

The Directorate General of Trade Remedies' proposed reduction in the anti-dumping duties on low-ash met coke imports could further improve import economics and encourage fresh bookings this year. "Despite the imposition of anti-dumping duty, the viability of coke imports is expected to sustain as imported material still offers pricing advantages over certain domestic alternatives," an Indian trader said.

Meanwhile, India's steel ministry has urged the Ministry of Finance to reconsider and withdraw the anti-dumping duty imposed on imported met coke, citing concerns over limited domestic availability and rising input costs for steelmakers.

Such a move would enable further growth in met coke imports.

Quality gap keeps imports relevant

Apart from pricing, Indian steelmakers continue to rely on imports because of quality constraints in domestic coke production.

Domestically produced met coke generally carries higher ash content (29-40%), which increases slag generation and raises blast furnace operating costs. Imported low-ash coke (12-14% ash content), especially from Indonesia, remains preferred for efficient blast furnace operations and consistent hot metal quality.

This quality differential is becoming increasingly important as Indian steelmakers push for higher productivity and lower fuel consumption amid tighter margins.

Indonesia strengthens position as dominant supplier

Indonesia's emergence as India's dominant met coke supplier is being reinforced by rapid capacity additions and integrated industrial infrastructure.

The country's coke production is concentrated at the Indonesia Morowali Industrial Park, where Chinese-invested enterprises, including those of Risun Group, the largest Chinese coke producer, have expanded aggressively.

Output from the industrial cluster rose to 8.2 mnt in CY'25 from 6.47 mnt a year earlier, while installed capacity reached 15.5 mnt per year by the end of CY'25, leaving significant room for further production growth.

Indonesia also benefits from logistical proximity to Australian coking coal suppliers. Freight movement from northern Australian export terminals such as Hay Point and Dalrymple Bay generally takes five to 10 days, enabling stable feedstock sourcing and competitive production economics.

Industry participants said integrated infrastructure, including captive energy supply, ports, and logistics support, has helped Indonesian producers lower costs and scale exports rapidly.

"India's imports will increase, and total imports from Indonesia alone may exceed 2 mnt," a global coal trader said.

"The competitiveness of Indonesian coke is likely to persist unless suppliers see stronger demand from alternative markets such as China or Vietnam," the Indian producer said.

Outlook

BigMint believes India's met coke imports will continue increasing, at least in the medium term, as domestic production capacity is insufficient to fully meet blast furnace requirements, particularly for low-ash grades. The long-term anti-dumping duty framework is unlikely to be a major hurdle given its limited magnitude.

India's met coke demand from the steel industry is projected to rise at a 7% CAGR to 52 mnt in FY'30 from 37 mnt in FY'26. However, domestic production growth has lagged demand expansion in recent years, while quality limitations persist. As a result, we believe a large part of the incremental requirement will be met through imports.

However, as met coke imports remain small compared with Indias coking coal imports of around 62 mnt in CY'25, higher met coke shipments are unlikely to significantly affect India's coking coal procurement.

To know more on what's happening inIndian coke industry, join theBigMint India Ferrous Week (BIFW 2026),which will take place in Kolkata from19-21 August 2026.