India's iron ore EC capacity rises over 10% in FY'26, utilisation drops on surging mining costs

...

- Captive utilisation falls 4 percentage points as production remains flat y-o-y

- High auction premiums, taxesand complex regulations slow mine development

Data Deep Dive:India's iron ore mining capacity continued to rise in FY'26, but production growth lagged behind. This suggests that India's immediate challenge is not resource availability but the pace at which approved mining capacity can be operationalised.

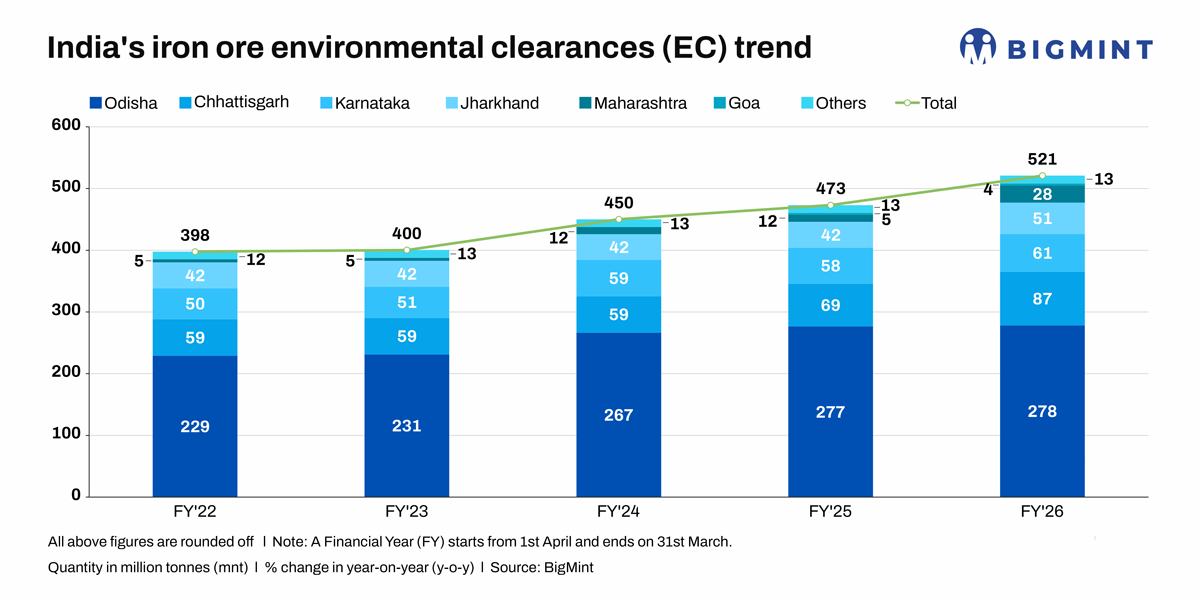

According to BigMint data, the country's approved environmental clearance (EC) capacity increased by 10.1% y-o-y to 521 million tonnes (mnt) in FY'26 from 473 mnt in FY'25. However, iron ore production rose at a slower pace of 7.9% to an estimated 313 mnt from 290 mnt.

Consequently, India's iron ore mining capacity utilisation slipped to 60.1% in FY'26 from 61.3% a year earlier. Moreover, the gap between approved ECs and actual production widened to 208 mnt from 183 mnt.

From FY'15 to May 2026, more than 150 iron ore mines have been auctioned. Out of these, approximately 42 mines have commenced operations so far. These figures exclude the two mines that were allocated to the Odisha Mining Corporation (OMC).

Merchant miners drive output growth

Merchant miners accounted for nearly all of India's production increase in FY'26. Their combined output rose 13% y-o-y to 188 mnt while approved capacity increased 11% to 289 mnt. Capacity utilisation improved marginally to 65.1% from 64.1%.

NMDC remained the country's largest producer, increasing output by 20% to 53 mnt. While its capacity remained broadly unchanged y-o-y at around 65 mnt in FY'26 (10 mnt in Kumaraswamy, 7 mnt in Donimalai, and 48 mnt in Chhattisgarh), it has increased significantly from about 55 mnt in FY24. It seems that the company is focusing on debottlenecking and expanding existing assets rather than acquiring new auctioned mines.

The company intends to start commercial mining from the 7-mnt Deposit 4 at Bailadila in Chhattisgarh and the 10-mnt Deposit 13 in Q2FY'27, which will take its EC to 82 mnt in FY'27. NMDC is targeting 100 mnt of capacity by 2030, with around 86 mnt from Bailadila and the rest from Donimalai.

Odisha Mining Corporation (OMC) increased capacity to 51 mnt from 47 mnt following commissioning of the Dubuna-Sakradihi mine with an EC for approximately 3 mnt. OMC's EC has more than tripled since FY'20, with the addition of mines such as Jilling Langalota (6.28 mnt) and Guali (5.7 mnt) in FY'21 and expansion of Daitari to 6 mnt in FY'22. Subsequently, capacity increased 17% in FY'24, with the expansion of Guali to 12 mnt and then in FY'25 with the scaling of Jilling Langalota to 10 mnt.

Lloyds Metals emerged as the fastest-growing producer. Its approved EC surged to 26 mnt from 10 mnt while production more than doubled to 22 mnt. The increase was driven by capacity enhancements at its Surjagarh mine in Maharashtra, considered India's largest, amid long-term plans to integrate mining growth with future steelmaking expansion. The company plans to expand Surjagarh's EC to 55 mnt in the future, though a specific timeline has not been provided.

Production by Vedanta, which operates iron ore mines in Odisha (ESL Steel), Karnataka, and Goa, declined marginally to 10 mnt despite stable capacity (25 mnt). While production has started in Goa, output from some Odisha assets remains below approved capacity. Production appears to be aligned with captive requirements and market economics.

Captive miners build headroom for future steel growth

Captive producers expanded approved capacity by 8.4% y-o-y to 232 mnt, while production remained broadly flat at 125 mnt. Consequently, capacity utilisation declined to 53.9% from 57.9%.

SAIL recorded the largest capacity addition among steelmakers, with approved mining capacity rising 21% to 82 mntfollowingadditions in Jharkhand, Odisha,and Chhattisgarh. However, production increased only 7% to 36 mnt.

A substantial portion of the unutilisedcapacity is located in Jharkhand, where SAIL has secured approvals for both run-of-mine extraction and tailingsrecovery projects that are still being gradually commissioned. Notably, there has been aprolonged delay in obtaining Stage-II Forest Clearance for SAIL's South-Central Block at Kiriburu-Meghahatuburu. Despite fulfilling afforestation and other statutory compliance requirements, the clearance has remainedpending since 2010.

In Chhattisgarh, SAIL's capacity growth in FY'26 was led by the Rowghat mine, where evacuation and infrastructure constraints continue to limit production ramp-up. Meanwhile, production growth has also been influenced by steel market conditions and internal ore requirements rather than mining capacity alone.

Tata Steel increased production by 14% to 42 mnt while approved capacity rose faster, by 21% to 67 mnt from 56 mnt. The company has expanded output from existing captive mines and secured additional resources through auctions as part of its long-term raw material security strategy. At present, the company sources entirety of its requirement through captive mines. However, due to steep auction premiums and unviable mining costs, Tata Steel plans to reduce this share to 50% after leases for four of its mines expire in CY'30.

Similarly, Jindal Steel increased approved capacity to 14 mnt from 11 mnt, while production rose to 6 mnt. The company commissioned the Roida-I mine, which has an EC of 3 mnt, although commercial production remains limited, pending operational clearances and ramp-up.

In contrast, JSW Steel's approved mining capacity declined sharply to 29 mntfrom 45 mnt, while production fell to 18 mntfrom 24 mnt. The reduction was primarily due to the surrender of the Jajang iron ore mine in Odisha, one of the company's key captive assets. The mine's surrender reduced annual production by around 5-6 mnt, andJSW nowpartiallyrelieson imports and merchant market purchases due to lower captive availability.

Notably, India's crude steel capacity will continue expanding over the coming five years, with integrated steelmakers comprising 48% of the national total. This has prompted steelmakers to secure captive iron ore resources well ahead of actual requirements. As a result, mining capacity creation is also being driven by future demand expectations rather than just current needs.

![]()

Odisha's EC volumes remain stable, Maharashtra logs fastest growth

Odisha remained India's largest iron ore producing state in FY'26, accounting for around half of national output with production of 158 mnt and approved capacity of 278 mnt. However, both capacity and production remained largely unchanged y-o-y.

Odisha's approved mining capacity has increased significantly from around 193 mnt in FY'21. In FY'26, while new mines entered production, capacity additions were partly offset by the surrender of assets such as JSW's Jajang mine.

Meanwhile, Maharashtra emerged as the fastest-growing mining region, with a capacity utilisation of 80%. Capacity more than doubled to 28 mnt and production doubled to 22 mnt, largely due to Lloyds Metals' expansion at Surjagarh.

Additionally, Chhattisgarh's capacity increased 26% to 87 mnt, while production rose 23% to 54 mnt.

In both FY'25 and FY'26, Karnataka recorded capacity utilisation of around 80%. Production growth remains constrained by the Supreme Court-imposed iron ore extraction ceiling of 50 mnt, which has limited the scope for significant capacity additions despite robust utilisation levels.

Goa also recorded a modest increase in approved capacity following the resumption of mining and lease auctions. However, production remainssignificantly below historical levels and continues to be more relevant for export-grade ore than domestic steelmaking demand.

![]()

Capacity additions face execution challenges

The fact that the rapid increase in approved mining capacity has not translated into equivalent production growth and around 40% of capacity remains unutilised reflects the challenges miners face in operationalising new assets.

Operational challenges hinder minedevelopment:Many recently auctioned mines in Jharkhand, Chhattisgarh, and Maharashtra were awarded as composite licences. Following auction, exploration, environmental approvals, forest clearances, and mine development can take several years before commercial production begins, particularly in forested regions such as in eastern India. Production ramp-up is also often constrained by inadequate rail connectivity, limited loading and evacuation infrastructure, and delays in developing supporting facilities.

Consequently, future raw material security will depend not only on mine ownership but also on the industry's ability to efficiently develop, beneficiate, and transport iron ore from existing assets.

Unfavourable economics disincentivise production: Many iron ore mines auctioned carry substantial revenue-sharing commitments to state governments, with winning bid premiums exceeding 100% of the Indian Bureau of Mines (IBM) average sale price. Such high statutory payments significantly increase the effective cost of ore production.

During periods of strong iron ore prices, miners can absorb these costs while maintaining profitability. However, when merchant market prices soften or regional demand weakens, margins become compressed, particularly for mines selling into the open market rather than supplying captive steel operations.

In such conditions, operators may prioritise production only to the extent required for captive consumption or contractual obligations rather than maximising output, leading to lower utilisation of approved capacities.

Moreover, India commands high royalty rates among mining geographies (15% of ASP on ad valorem basis), other taxes,and additional premium for ore sales by public sector units (PSUs) in the open market.India's royalty rate is much higher than major mining geographies such as Australia and Brazil, which are mostly in single digits.

Outlook

BigMint estimates India's iron ore requirement at around 300 mnt in FY'27, against expected production of more than 330 mnt. While output will continue rising as recently auctioned mines gradually ramp up operations, EC volumes are likely to increase faster as miners and steelmakers focus on building capacity for future steel demand rather than current consumption.

Overall, the industry's current challenge seems to beextracting value from existing assets rather thansecuring mining rights. In fact, despite the latest capacity additions, India's iron ore quality profile is deteriorating, which has led to concerns over the availability of suitable feedstock for blast furnaces and pellet plants.

Notably, the share of Fe 65%+ ore produced dwindled to 11% of India's total in FY'26 compared to 20% in FY17, while 60-62% rose to 20% in FY'26 from 14% in FY'17. Lower bands such as Fe 55-58% and Fe 51-55% expanded to a combined 20% in FY'26 from 13% in FY'17. Persistent constraints in high-grade ore availability could sustain demand for imported ore and pellets among coastal steelmakers. It also underscores the need for accelerated operationalisation of new auctioned mines.