India's industrial momentum turns uneven amid softer manufacturing activity

...

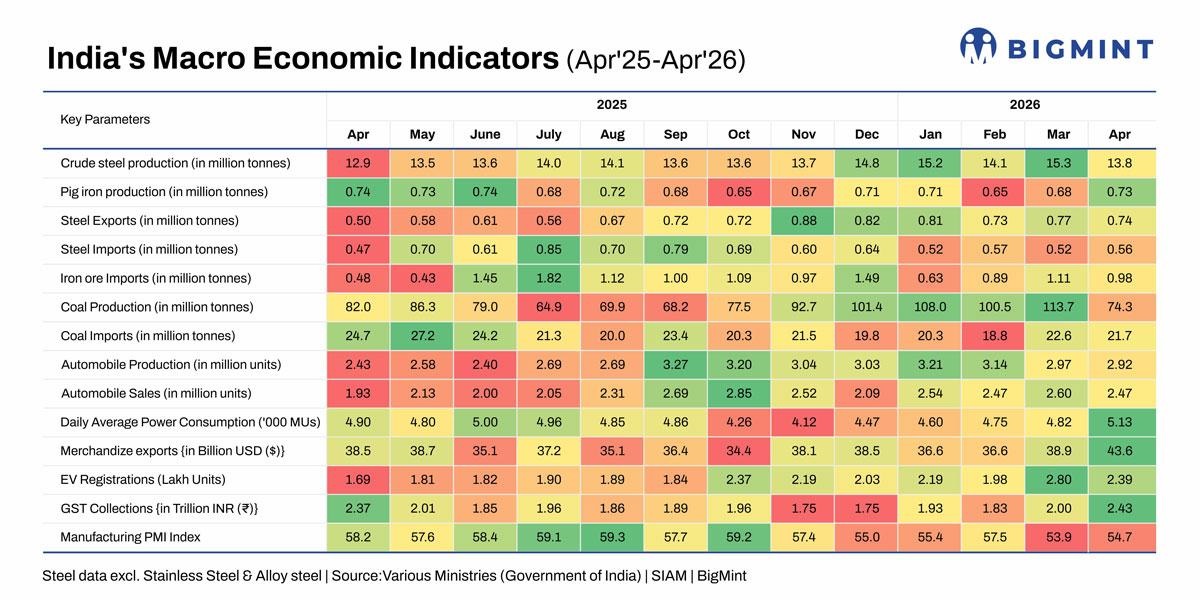

- Crude steel output declines in Apr'26 after strong Q1 performance

- Power demand, GST collections, EV registrations remain resilient

- Exports, manufacturing indicators show moderation

Morning Brief: India's macro-industrial indicators in April '26 pointed to an increasingly uneven growth environment, with domestic consumption-linked sectors remaining relatively resilient even as manufacturing momentum and export-oriented industrial activity softened. The latest data from BigMint suggest that while the broader economy continues to be supported by infrastructure activity, power demand, and formal-sector spending, pressure is beginning to emerge across steel, automobiles, and external trade-linked sectors.

Crude steel production declined to 13.83 million tonnes (mnt) in April from 15.32 mnt in March, reversing part of the strong Q1 momentum. Steel exports also moderated further to 0.74 mnt, while automobile production declined to 2.92 million units, indicating softer industrial activity following the fiscal year-end production surge.

At the same time, domestic macro indicators remained relatively firm. Daily average power consumption rose to 5.13 thousand million units (MUs) in April, GST collections increased sharply to INR 2.43 trillion, and EV registrations remained elevated at 2.39 lakh units, highlighting continued resilience in domestic economic activity despite moderation across parts of manufacturing.

Steel sector enters softer phase after year-end surge

India's steel sector entered a softer phase in April following sustained high utilisation during the previous quarter. Crude steel output fell by nearly 10% m-o-m, while steel exports continued weakening amid subdued global demand conditions and pressure from competitively priced imports in overseas markets.

Steel consumption also moderated after the fiscal year-end surge, particularly in the non-alloy segment, indicating cyclical normalisation rather than a broad-based collapse in industrial activity.

However, the decline in steel production did not fully translate across all metallic segments. Pig iron output increased to 0.73 mnt in April from 0.68 mnt in March, suggesting that industrial and foundry-linked demand remained relatively stable despite weakness in broader steel markets.

The divergence indicates that construction steel and flat steel demand softened more sharply than industrial castings and pipe-related demand, reflecting uneven downstream consumption patterns rather than a broad industrial slowdown.

Trade and manufacturing indicators weaken

India's steel imports remained elevated at 0.56 mnt in April despite safeguard measures and import restrictions, suggesting that domestic buyers continued relying on overseas material for select grades and cost advantages.

Meanwhile, manufacturing-linked indicators weakened across several sectors. Automobile production declined for the third consecutive month, while the Manufacturing PMI moderated to 54.7 in April from 57.5 in February, indicating slower expansion in factory activity.

The moderation in automobile production also suggests increasing operational caution among manufacturers following strong year-end dispatches and inventory build-up during the previous quarter.

Merchandise exports rebounded to $43.56 billion in April, but the broader trend remained volatile amid weak global manufacturing conditions and trade uncertainty.

Domestic demand remains the key stabilising factor

Despite softer manufacturing momentum, domestic demand indicators remained relatively supportive. Strong GST collections and rising electricity consumption suggest that formal-sector activity, infrastructure spending, and summer-related power demand continued to anchor economic activity.

The continued rise in EV registrations also points to ongoing structural growth in domestic mobility and energy-transition sectors, even as broader automobile production moderated.

Importantly, the data suggest that India's current industrial cycle remains primarily domestically anchored. While export-oriented sectors and manufacturing activity have weakened amid softer global demand conditions and post year-end normalisation, internal consumption, infrastructure spending, and power demand continue providing stability to the broader economy.

Outlook

India's industrial momentum is expected to remain uneven in the near term as domestic demand resilience offsets weakness in manufacturing exports and heavy industrial activity.

Steel production and manufacturing indicators may remain under pressure amid softer global trade conditions, cautious industrial procurement activity, and cyclical normalisation following strong Q4 production levels. However, infrastructure spending, resilient power demand, and formal-sector consumption are likely to continue supporting overall economic activity despite the emerging moderation across parts of the manufacturing sector.