India's HRC-rebar spread widens to 4-year high in Jun'26 as BF rebar prices fall by over INR 5,000/t m-o-m

...

- Construction slowdown causes 9% m-o-m drop in BF rebar prices

- HRC prices fall slightly by INR 200/t amid need-based demand

- Safeguard duty, firm Chinese prices keep HRC prices supported

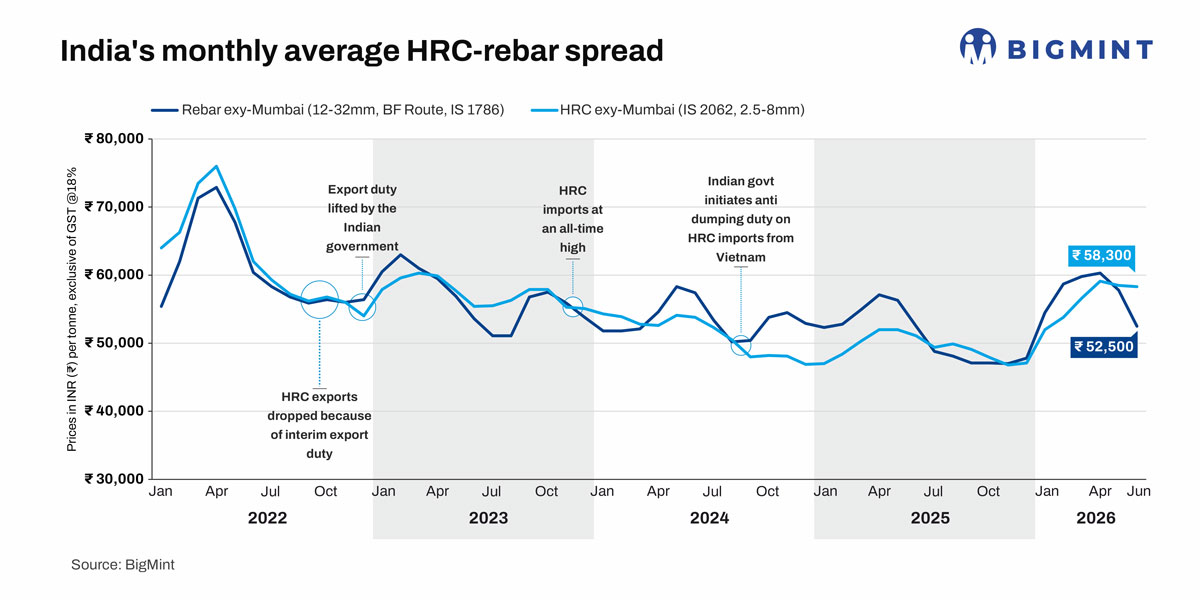

Morning Brief: The spread between India's hot-rolled coil (HRC, IS 2062, 2.5-8 mm) and blast furnace (BF)-route rebar (12-32 mm, IS 1786) prices widened sharply to INR 5,800/t ($61/t) in June from INR 700/t ($7/t) in May, based on BigMint's analysis of monthly average prices.

This is the widest differential since January 2021 and marks a return to the long-term average of around INR 4,500-5,000/t ($47-53/t) for the first time in three years. Notably, the price spread has remained negative or near parity for much of the past two years, as elevated Chinese HRC imports had eroded the premium that HRC generally commands due to its usage in higher-value manufacturing sectors.

The expansion was driven almost entirely by a sharp 9% m-o-m correction in BF-route rebar, while HRC prices fell by less than 0.5% m-o-m. BF rebar prices fell by INR 5,300/t ($56/t) m-o-m to INR 52,500/t ($552/t) as inventories swelled across the supply chain and construction activity slowed with the onset of the monsoon. In comparison, HRC prices eased by INR 200/t ($2/t) to INR 58,300/t ($613/t) amid need-based demand, though prices were supported by the safeguard duty and firm global prices. Both prices are exy-Mumbai and exclude GST at 18%.

Rebar prices fall sharpest in 4 years amid construction slowdown

BF-route rebar recorded its steepest m-o-m correction in more than four years, as integrated mills prioritised inventory liquidation amid weak construction activity. Prices in June were around INR 5,500/t ($58/t) higher than November levels, when prices had hit a five-year low.

Tier-1 mills cut June list prices by INR 1,000-4,000/t ($11-42/t) after mill inventories reportedly increased around 35% m-o-m. As weak demand persisted, stocks continued building across the supply chain. Distributor inventories climbed from 25-30 days in early June to more than 35-40 days by month-end, forcing traders to offer aggressive discounts.

Demand remained largely need-based across both retail and project segments. Heavy rainfall, delayed project execution, labour shortages, and temporary restrictions on construction activity in parts of Mumbai (due to water shortages in late June) further weakened steel consumption. Project prices consequently declined to INR 49,000-50,000/t ($515-526/t) landed by end-June from INR 55,000-56,000/t ($578-589/t) in late May.

Competition from induction furnace (IF)-route producers added further pressure. IF-route rebar prices declined by around INR 1,500/t ($16/t) during June to INR 45,700/t ($481/t), prompting integrated mills to reduce prices more aggressively. The BF-IF price spread narrowed from nearly INR 10,000/t ($105/t) at the beginning of June to around INR 6,000/t ($63/t) by month-end, improving BF rebar's competitiveness but failing to revive demand.

Lower raw material costs also enabled mills to reduce prices. Odisha iron ore fines (Fe 62%) declined by around INR 350/t ($4/t) during June to INR 5,000/t ($53/t) ex-mines, though premium hard coking coal remained broadly stable at around $265/t CNF Paradip.

HRC remains supported despite slower manufacturing growth

Domestic HRC prices remained comparatively resilient, remaining at around three-year highs and around INR 11,500/t ($121/t) higher than December 2025 levels. Unlike long steel demand, which entered its seasonal off-period in June, flat steel demand remained supported by the safeguard duty on imports, continued expansion in manufacturing activity, and firm global prices. Consequently, at the start of the month, mills largely maintained pricing discipline, keeping list prices stable.

However, HRC prices inched down, as market sentiment was cautious, with trading largely driven by immediate requirements as distributors delayed restocking. Payment collection issues and the onset of the monsoon also weighed on downstream demand.

Manufacturing activity remained in expansion territory, although momentum weakened. India's manufacturing purchasing managers' index (PMI) eased to 54.2 points in June from 55.0 in May, the second-lowest reading in four years. Growth slowed across output, new orders, and exports, particularly in capital goods, but consumer and intermediate goods sectors continued to support flat steel demand.

Domestic pricing also benefited from favourable trade dynamics. Imported HRC remained significantly more expensive than domestic material, with landed prices assessed at INR 64,000-65,600/t ($673-690/t) against the domestic benchmark of INR 58,300/t ($613/t). The premium of INR 5,700-7,300/t ($60-77/t) effectively removed the incentive for fresh imports. Bulk HRC imports moderated to 209,731 t by 26 June compared to 423,925 t in May.

As for international benchmarks, Chinese export HRC prices eased by $2/t to around $516/t FOB Rizhao during June but remained at a 20-month high due to elevated raw material costs.

Bulk HRC exports moderated to 176,704 t by 26 June compared to 231,749 t in May. The HRC export index to the EU weakened by $19/t or 3% to $619/t FOB main port India. Export demand slowed ahead of the implementation of the EU's revised country-specific quota regime, coupled with elevated inventory levels. Meanwhile, the HRC export index for the Middle East and Southeast Asia fell by $2.5/t to $550/t FOB main port, India. Weak demand, geopolitical uncertainties, elevated freight costs, delayed vessel berthing, and the summer holiday season continued to limit trade to the Middle East.

Outlook

We believe that the divergence between flat and long steel markets will continue through July.

Construction activity is likely to remain subdued during the peak monsoon period, while elevated inventories and competition from IF-route producers should keep BF-route rebar under pressure. BigMint has heard that integrated mills may reduce July list prices by INR 1,000-2,000/t ($11-21/t), while trade prices could decline by a further INR 2,000-3,000/t ($21-32/t) during the month.

HRC fundamentals remain comparatively stronger, although momentum is softening. The safeguard duty's protection and healthy manufacturing activity should continue to support domestic prices. However, weaker manufacturing PMI, slower capital goods activity, softer export order growth, and rebates of around INR 1,000/t ($11/t) offered by mills during June indicate that demand is gradually cooling.

The export outlook has also become more challenging. The EU's revised country-specific quotas are expected to restrict HRC shipments to India's largest overseas market. However, the impact is likely to be limited this month, as greater clarity regarding the quotas could encourage buyers to close deals.

Therefore, BigMint expects domestic HRC prices to ease modestly in July, although the correction is likely to be significantly smaller than that in BF-route rebar. Consequently, the HRC-rebar spread is expected to widen through the monsoon quarter before narrowing as construction activity recovers.