India's coated flat steel industry records moderate FY'26 growth amid downstream expansion, price volatility

...

- Integrated steelmakers strengthen coated steel market share in FY'26

- South Korea and Japan remain key suppliers of specialised coated steel imports

- Geopolitical tensions drive coated steel rally before prices soften post-ceasefire

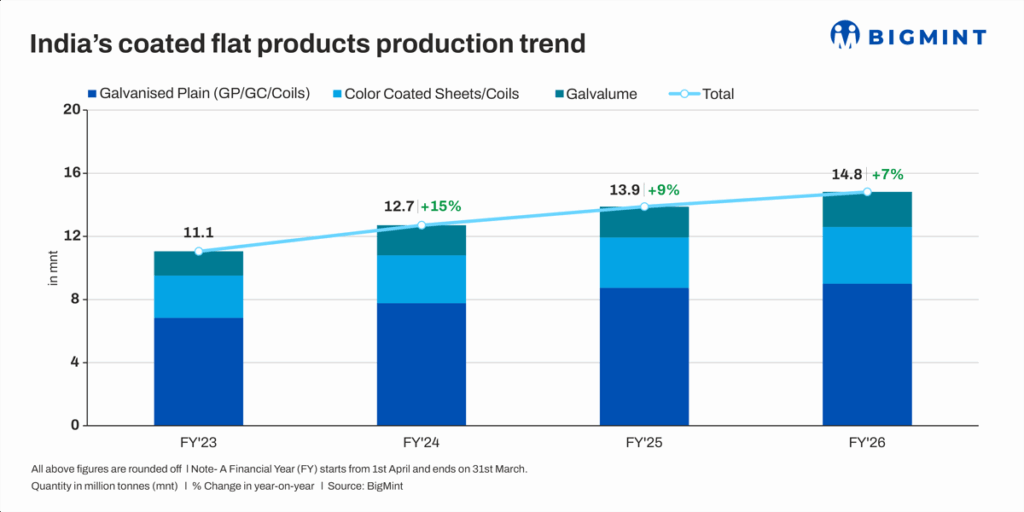

Morning Brief: India's coated flat steel industry recorded moderate growth across major product categories in FY'26, supported by higher production from leading integrated steelmakers and rising investments in downstream and value-added steel capacities. Long-term demand drivers from infrastructure, automotive, appliances, and construction continued supporting the segment, while major steelmakers further strengthened their market share in coated flat products.

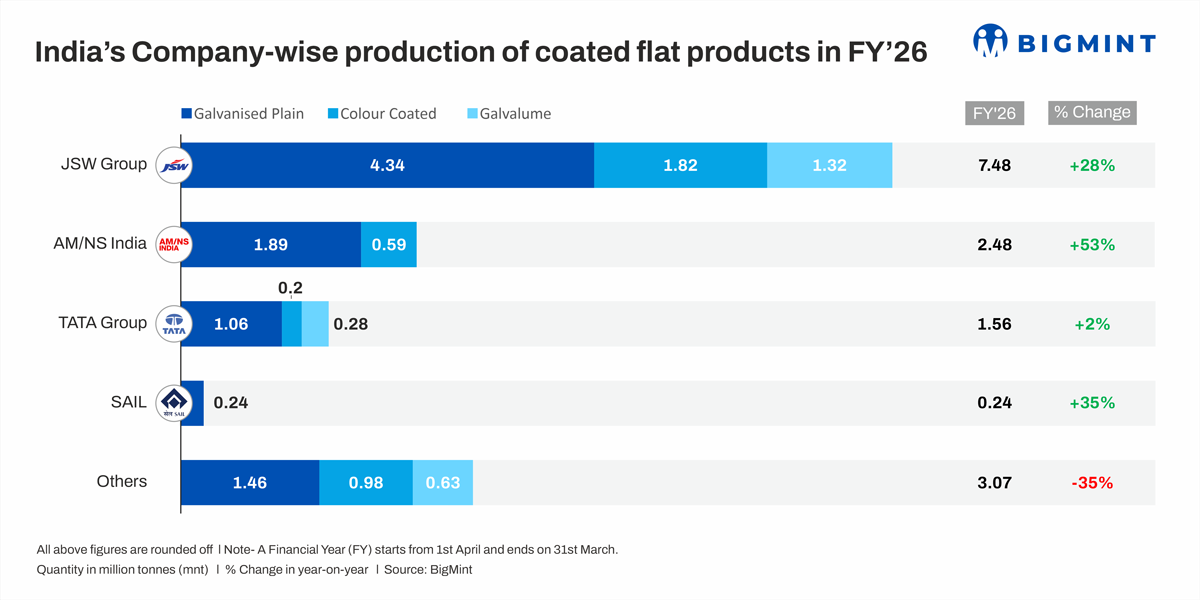

GP/GC production increased by 0.26 million tonnes (mnt) y-o-y to 9 mnt in FY'26, driven mainly by higher output from JSW Group and AMNS. JSW Group retained its leadership position with production rising to 4.34 mnt, while AMNS output improved to 1.89 mnt. However, lower contribution from smaller producers limited overall growth momentum during the year.

In the colour-coated segment, production rose by 0.39 mnt y-o-y to 3.6 mnt, supported by stronger output from JSW Group and AMNS amid steady demand from infrastructure and downstream applications. JSW Group remained the largest producer with 1.82 mnt output, while AMNS production increased to 0.59 mnt.

Galvalume production also increased by 0.27 mnt y-o-y to 2.23 mnt in FY'26, led by improved output from JSW Group and Tata Group. JSW Group continued dominating the segment with production reaching 1.32 mnt, while Tata Group's contribution increased marginally.

Overall, the data indicates that India's major steelmakers, particularly JSW Group, continued consolidating their share in the coated flat steel market amid gradual improvement in production levels during FY'26.

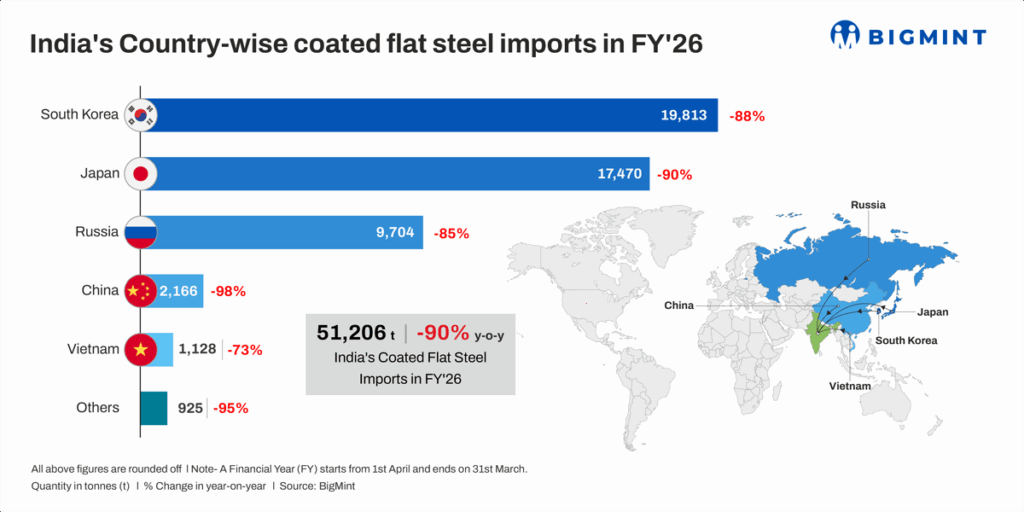

South Korea and Japan remain dominant import suppliers

India's coated flat steel imports in FY'26 remained concentrated among Asian suppliers, with South Korea emerging as the largest exporter to India at 19,813 t, followed by Japan at 17,470 t, as per projected figures. Together, both countries accounted for a significant share of total imports, reflecting their strong presence in specialised and value-added coated steel grades.

Russia also maintained a notable share with exports of 9,704 t, while China contributed comparatively lower volumes of 2,166 t during the period.

Among other suppliers, Vietnam exported 1,128 t, followed by Indonesia at 536 t and France at 266 t. Imports from the United States and Italy remained marginal at 99 t and 24 t, respectively.

The import pattern indicates India's continued dependence on East Asian suppliers for specialised coated flat steel requirements, particularly in high-grade and value-added segments.

Steelmakers accelerate downstream and coated steel investments

India's coated flat steel industry is witnessing fresh investments in downstream and value-added capacities as major steelmakers strengthen their presence in premium coated products amid rising demand from automotive, infrastructure, appliances, and construction sectors.

Recently, John Cockerill secured a $32 million contract from JSW Steel Coated Products Limited to supply a continuous galvanizing line (CGL) at JSW's Khopoli facility in Maharashtra, with commissioning targeted by May 2028.

Similarly, Tata Steel announced multiple downstream expansion initiatives, including a 0.7 mntpa Hot Rolled Pickling and Galvanizing Line (HRPGL) at Tarapur to cater to automotive applications and support import substitution. The company also approved engineering work for a 2.5 mntpa thin slab caster and rolling facility at Meramandali and a 4.8 mntpa expansion at Neelachal Ispat Nigam Limited (NINL).

Meanwhile, Jindal India announced a INR 1,500 crore investment to expand capacity to 1.6 mnt, focusing on coated flat products, pipes, and crash barriers.

The automotive-grade coated steel segment is also witnessing increased investments. ArcelorMittal Nippon Steel India recently inaugurated a 2 mntpa Pickling Line and Tandem Cold Mill (PLTCM) at its Hazira plant in Gujarat as part of its INR 60,000 crore expansion programme. The facility, inaugurated by Keiichi Ono, will support domestic production of Advanced High Strength Steel (AHSS), galvanised (GI), galvannealed (GA), and press hardened steel (PHS) products for automotive applications.

Industry participants noted that rising urbanisation, infrastructure development, and increasing localisation in the automotive sector are driving demand for high-quality coated and corrosion-resistant steel products. Consequently, steelmakers are increasingly investing in advanced downstream facilities to improve product mix, support import substitution, and strengthen competitiveness in value-added steel segments.

Geopolitical tensions drive coated steel rally before prices soften

GP (0.8mm, CTL, 120gsm) and PPGI (0.5mm, CTL, 90gsm) prices remained largely stable between October and December 2025 before entering an upward trend from January 2026.

The sharp escalation in geopolitical tensions during February 2026 acted as a major trigger for the rally, as supply chain disruptions, weaker import competitiveness, and higher logistics and input costs strengthened domestic mills pricing power.

GP prices increased by around INR 8,000-9,000/t from January lows to touch a three-year high of INR 79,100/t by end-April 2026, reflecting an increase of nearly 12-13%. Similarly, PPGI prices rose by around INR 7,000-8,000/t to INR 86,900/t during the same period, marking a gain of approximately 9-10%.

The spread between GP and PPGI prices remained largely stable at around INR 7,500-8,000/t, supported by steady value-added demand, with coated products remaining relatively less exposed to spot-market volatility than commodity flat steel.

Compared to HRC and CRC, coated steel demand remained comparatively more stable, aided by steady enquiries and tighter spot availability due to gas supply constraints at select mills.

However, following the ceasefire announcement in April 2026, the geopolitical premium began fading, leading to softer prices and cautious market sentiment. Elevated inventories, weak project-led demand, and slower bookings pushed buyers towards need-based procurement, while BGL prices remained comparatively stable due to tighter supply availability.

Overall, market sentiment remains bearish, with subdued demand and cautious trading activity expected to continue in the near term.

Outlook

India's coated flat steel market witnessed moderate growth in FY'26, supported by higher production from major integrated steelmakers such as JSW Group and AMNS, along with rising investments in downstream and value-added coated steel capacities.

Demand from infrastructure, automotive, and appliances continued supporting the segment, while imports remained largely dependent on South Korea and Japan for specialised grades.

Coated steel prices surged during February-April 2026 amid geopolitical tensions, supply disruptions, weaker import competitiveness, and higher input costs, with GP and PPGI prices reaching multi-year highs.

However, following the ceasefire announcement, prices softened as the geopolitical premium faded and market sentiment turned cautious due to elevated inventories, subdued project demand, and slower bookings.

Going forward, the long-term outlook for coated steel remains positive, driven by infrastructure growth, urbanisation, and automotive localisation. However, in the near term, the market is expected to remain under pressure, with soft pricing trends, cautious procurement activity, and weak spot demand likely to persist across major regions.