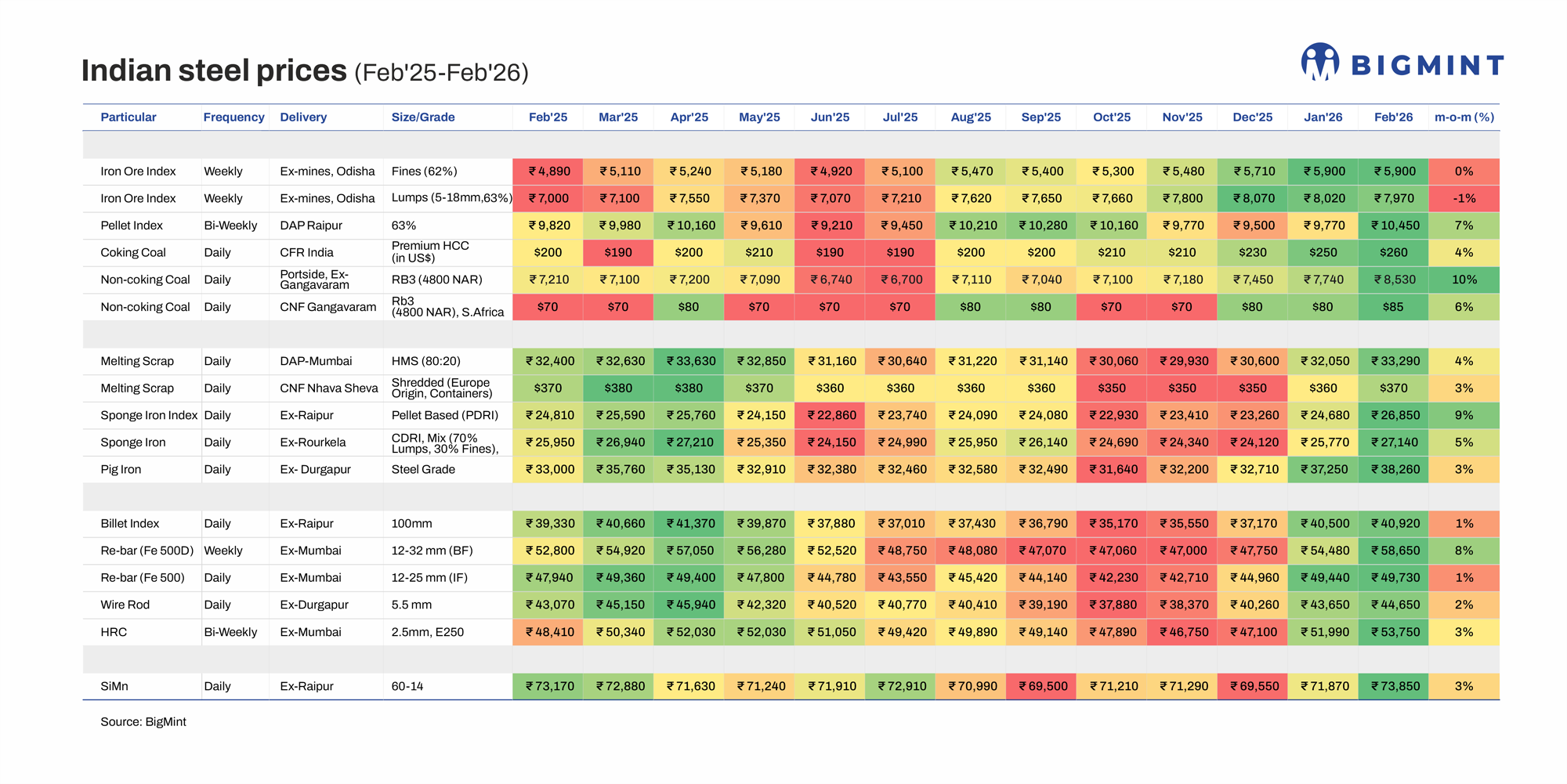

Indian steel prices rise again in Feb'26 but at slower pace as bullish sentiment fades

...

- Steel demand slows from mid-Feb amid price resistance, Holi

- Rising coal, firm iron ore prices support steel price uptrend

- BF rebar records sharpest hike among finished steel at 8% m-o-m

Morning Brief: Indian steel prices continued to increase in February 2026 (as per monthly averages), but the pace of growth slowed sharply compared to January. Where January had recorded percentage increases in the range of 9-14% m-o-m across semi-finished and finished steel, in February, the growth was limited to a modest 1-3%, except for rebars produced through the blast furnace (BF) route, whose prices surged by 8% m-o-m.

Price growth slowed, as the earlier optimism around the safeguard duty on flat steel imports and anti-dumping duty on met coke imports faded. Following active restocking in January, buyers also slowed steel purchases, refraining from trading at higher prices, especially from the third week of February. Demand slowed down further during the month-end as Holi (4 March) approached, with labour shortages and transport disruptions expected during the holidays.

Meanwhile, apart from iron ore, prices of steelmaking raw materials and scrap and metallics also rose, providing cost support for price hikes. However, raw material prices increased faster than steel, suggesting additional cost pressures on mills, particularly in the induction furnace (IF) segment. Additionally, supply shortages emerged in select segments, lending upward momentum to prices.

Snapshot of steel, raw material price movements in Feb'26

Iron ore

Fines, lumps: BigMint's Odisha iron ore index remained stable m-o-m in February, supported by tight supply as miners' environmental clearance (EC) limits approaching expiry in March. However, buyers' resistance to prices, need-based procurement by steelmakers, a fall in bids at the Odisha Mining Corporation (OMC) auction, and price corrections in sponge iron and steel in the second half of February prevented price hikes in fines and dragged down lumps prices.

Pellets: BigMint's PELLEX, tracking pellet prices in Raipur, jumped m-o-m, as demand from sponge iron players improved. Raw material costs also increased, as the National Mineral Development Corporation (NMDC) raised iron ore prices by INR 100/t, while supply tightened, as some pellet plants closed sales during the second half of the month, when sponge iron prices weakened.

Coal

Coking coal: Premium hard coking coal (PHCC) prices imported into India increased by 4% in February, slower than January's 9%. Supply remained tight due to cyclonic disruptions in Australia in January. However, as the month progressed, availability improved, and buyers were able to negotiate down prices.

Non-coking coal: South African thermal coal prices rose sharply in February as supply remained tight. Earlier, in January, South African exports to India fell around 50% m-o-m due to logistics disruptions, leading to limited stocks at key ports in India such as Dhamra, Gangavaram, and Haldia in February. Moreover, demand from sponge iron manufacturers was also strong initially, though it gradually waned towards the second half due to high prices.

Ferro alloys

Silico manganese: Domestic silico manganese prices edged up on the back of an increase in raw material costs, as MOIL raised its prices and imported ore also became more expensive. Suppliers tried to keep offers firm but had to give in to lower bids from buyers as steel demand softened.

Scrap and metallics

Domestic scrap: Indian HMS 80:20 prices increased, facilitated by supportive steel market sentiment. Additionally, domestic scrap sellers capitalised on limited arrivals of imported material.

Imported scrap: Imported scrap prices inched higher on tight supply overseas, with recyclers in the US and Europe -- major exporting regions to India -- facing winter-related collection constraints. However, overall, trade was cautious, as a weak rupee kept landed costs high and rebar demand eventually moderated.

Sponge iron: Sponge iron prices climbed up in line with rising costs of raw materials -- pellets and South African thermal coal. Demand was also moderately strong, except during the second half of February. The pellet-based variant rose a sharper 9%, as supply tightened for a brief period following several manufacturers closing sales amid compressed margins. Meanwhile, the lump-based variant rose more modestly due to the slight correction in lumps prices.

Pig iron: Rising input costs -- of met coke and coking coal -- lifted pig iron prices in February. Met coke prices increased by 5% m-o-m to INR 34,725/tonne (t), driven by escalating coking coal prices. Demand also remained robust, while firm finished steel prices lent support.

Steel

Billet: Cost support from higher raw material prices led to a marginal increase in billet prices during February. However, uneven, need-based demand, cautious buyer sentiment, and weaker finished steel offtake prevented price gains.

Rebar: Both BF and IF rebar prices climbed up m-o-m, but there was a stark divergence in terms of magnitude. Primary mills implemented several list price hikes throughout the month, driven by robust bookings and substantial order backlogs. Production by a major steelmaker has also been limited since September 2025 due to the shutdown of a blast furnace for capacity upgradation. Consequently, material shortages emerged in the distribution channel. Moreover, demand from the project segment remained healthy.

Meanwhile, IF rebar prices increased marginally. Price gains from higher raw material costs in early-February were wiped away as buyers turned cautious mid-month and sellers reduced offers to secure orders. Inventory holding periods increased to 10-12 days by February-end from a comfortable 8-10 days at the start of the month.

Wire rod: Similarly, wire rod prices inched up by a minor 2%. Prices peaked mid-month but then softened as trading momentum moderated.

HRC: Prices of hot-rolled coils (HRCs) climbed up slightly, primarily due to mill-led price hikes and tightening supply in select regions. Demand was moderately strong initially, but buyers began to hold off on purchases in anticipation of price corrections. Some sellers began to offer discounts to liquidate inventories and book profits, as despite the price drops, values remained higher than in previous months.

Outlook

Indian steel and raw material prices are set for a broad-based uptrend in March due to a couple of reasons: First, miners' ECs are getting exhausted, which has tightened iron ore supply and will keep prices firm. Second, given that March is the end of the fiscal year, infrastructure and construction companies will be in a rush to procure material to meet project deadlines. Other segments, such as manufacturing, may also witness a similar pick-up in demand. Moreover, the US-Iran war is likely to push up coal prices temporarily because of disruptions in sea routes and the impact on gas and oil supply. Scrap imports may also be impacted, potentially causing tight supply in India.