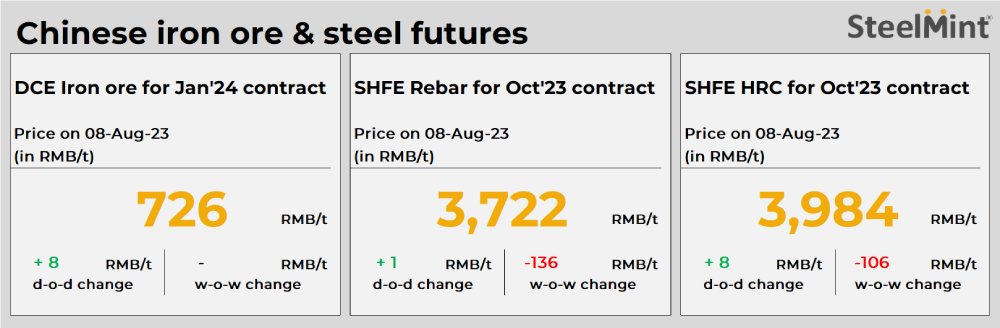

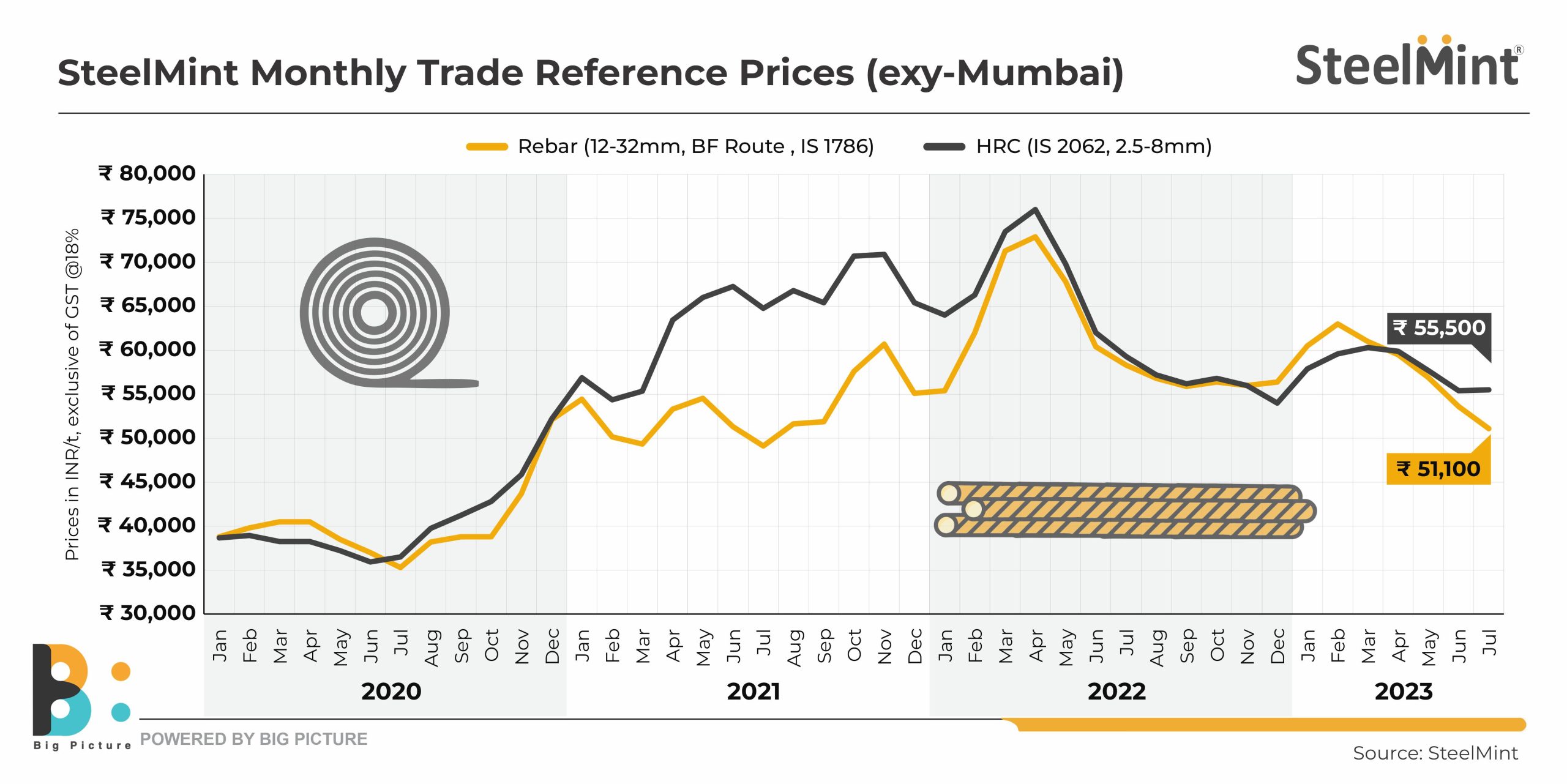

Indian HRC-rebar spread widens to over 15-month high in Jul'23

...

The hot rolled coil (HRC)-rebar spread widened to a 17-month high of INR 4,400/tonne (t) ($53/t) in July 2023. It is also the highest level seen so far this calendar. The last time similar levels were reached was in February 2022.

HRCs are usually sold at a premium to rebars. However, the spread had reversed towards the beginning of the year with rebars selling at a premium to HRCs. Now, the trend is seen normalizing with the spread settling at current levels.

Thus, benchmark HRC prices were at INR 55,500/t ($670/t) in July 2023. But rebars touched a lower INR 51,100/t ($617/t).

Why has the spread normalized?

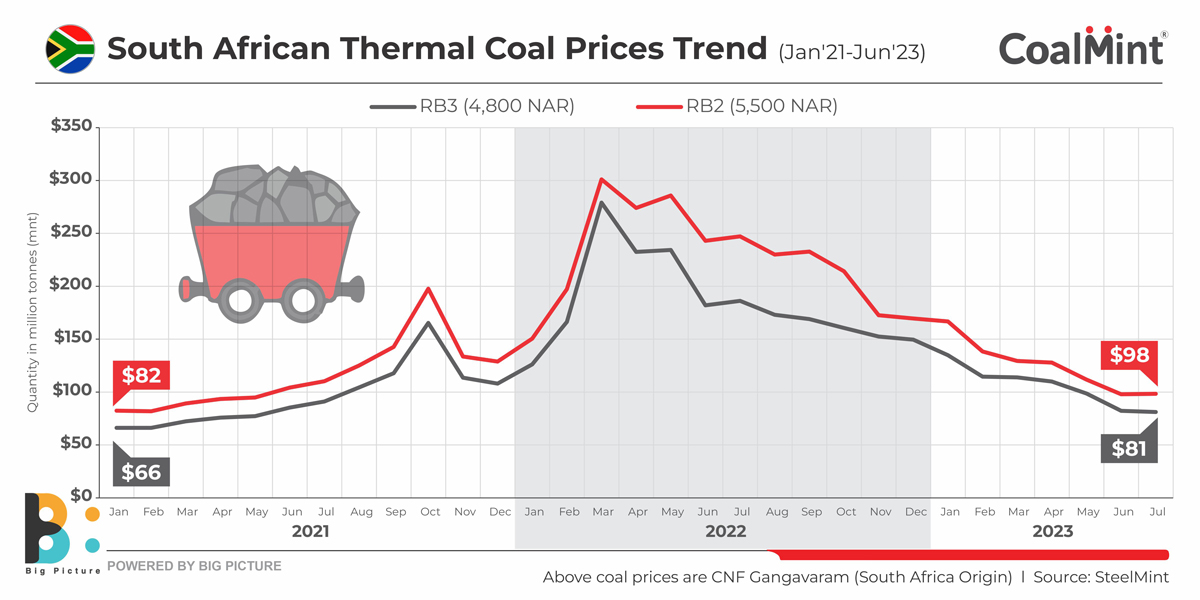

Energy prices loose steam: Out of the total rebar production, 60-65% emerges from the electric arc furnaces (EAFs) and induction furnace (IF) mills which fall back heavily on thermal coal to fire their furnaces. That apart, sponge iron, used as feed by these mills, use thermal coal of certain specifications as fuel, a substantial portion of which was being imported since domestic coal availability for the non-power sector was limited.

Imported as well as domestic thermal coal prices had skyrocketed last year on the back of several factors. These included high gas prices which forced Europe to revive its coal-fired plants, putting pressure on South African coal as Russian supplies to Europe dried up in the face of embargoes from the West. Secondly, logistics issues at South Africa's Transnet disrupted supplies. Thirdly, sliding currencies globally made imports costlier. In domestic, Coal India diverted the lion's share of its production to the power sector, leaving the smaller mills high and dry.

However, with time, energy prices started normalizing. Gas prices dropped in Europe, which in turn eased the pressure on South African supplies. Blends with cheaper Russian varieties helped to ease prices too. Thus, portside ex-Gangavaram South African RB2 prices started tapering off from their historic peak of INR 22,000/t ($266/t) in May 2022 to the current levels of INR 9,000/t ($109/t).

In domestic, availability to the non-power sector rose with a 12% increase in CIL's production in FY2022-23, the fastest growth rate in the last few decades. This allowed CIL to allocate higher volumes for e-auctions compared to the usual. It also projected higher production of 780 mnt this fiscal. Consequently, prices of the G-9 (4600-4900 kCal/kg), widely used in electric furnaces, fell by around 18% so far this year as per National Coal Index data.

Thus, the cost of rebar production eased significantly in the last 15-odd months.

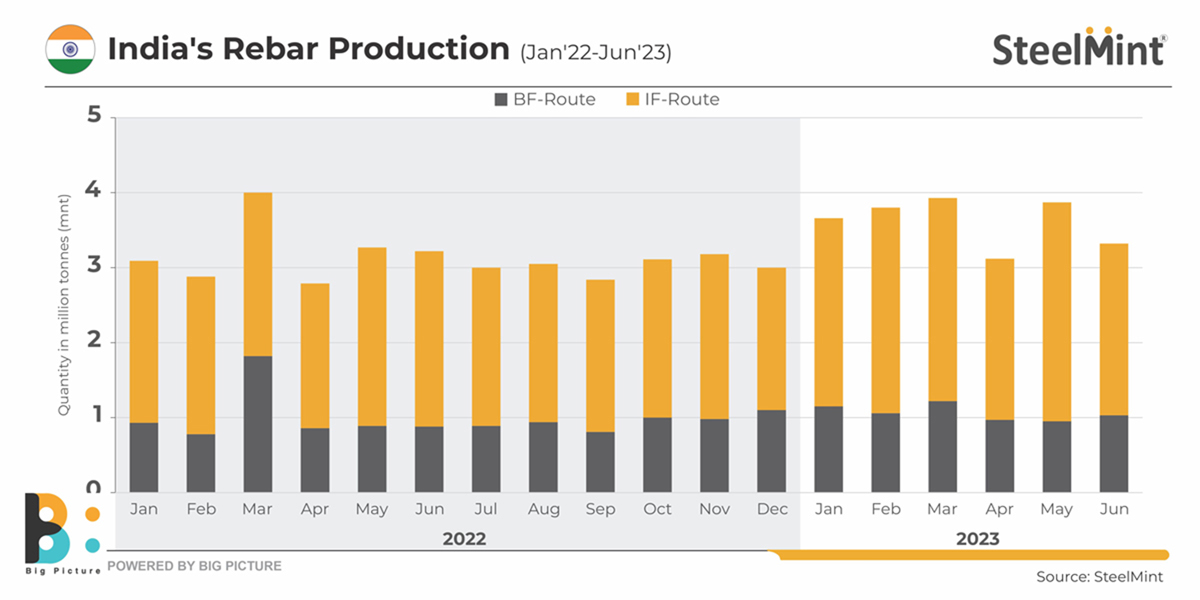

Rebar production increases: Several of the large mills increased production in the last one year. SteelMint's data reveals, while rebar output in the entire calendar of 2022 was at 37 million tonnes, volumes in the first half of January-June, 2023, touched 60% of last year's volumes at around 22 mnt.

Weak export demand for longs: Exports of rebars fell more steeply compared to flats. From around 1.05 mnt in 2021, these dropped sharply to 0.42 mnt in 2022 and a mere 96,000 tonnes in January-June, 2023. In comparison, HRC/plates exports declined from 6.42 mnt in 2021 to 3.26 mnt in 2022 and 1.95 mnt over January-June, 2023. Longs are experiencing weak export demand as intake globally for longs is subdued because of high interest rates that are impacting housing demand. Plus, Asia, where longs are exported, is already glutted with material from China, Malaysia, Gulf countries and Indonesia.

Outlook

Looking at the near term, flats are expected to stay firm as two large mills have already announced a hike in HRC list prices by INR 750/t ($9/t) and INR 1,000/t ($12/t) for cold rolled coils.

Rebar prices may spurt slightly, driven by increased raw material cost push.