India: Zinc dross, oxide prices extend gains despite LME correction

...

- Secondary zinc market supported by higher replacement costs

- Procurement activity remains need-based amid volatile conditions

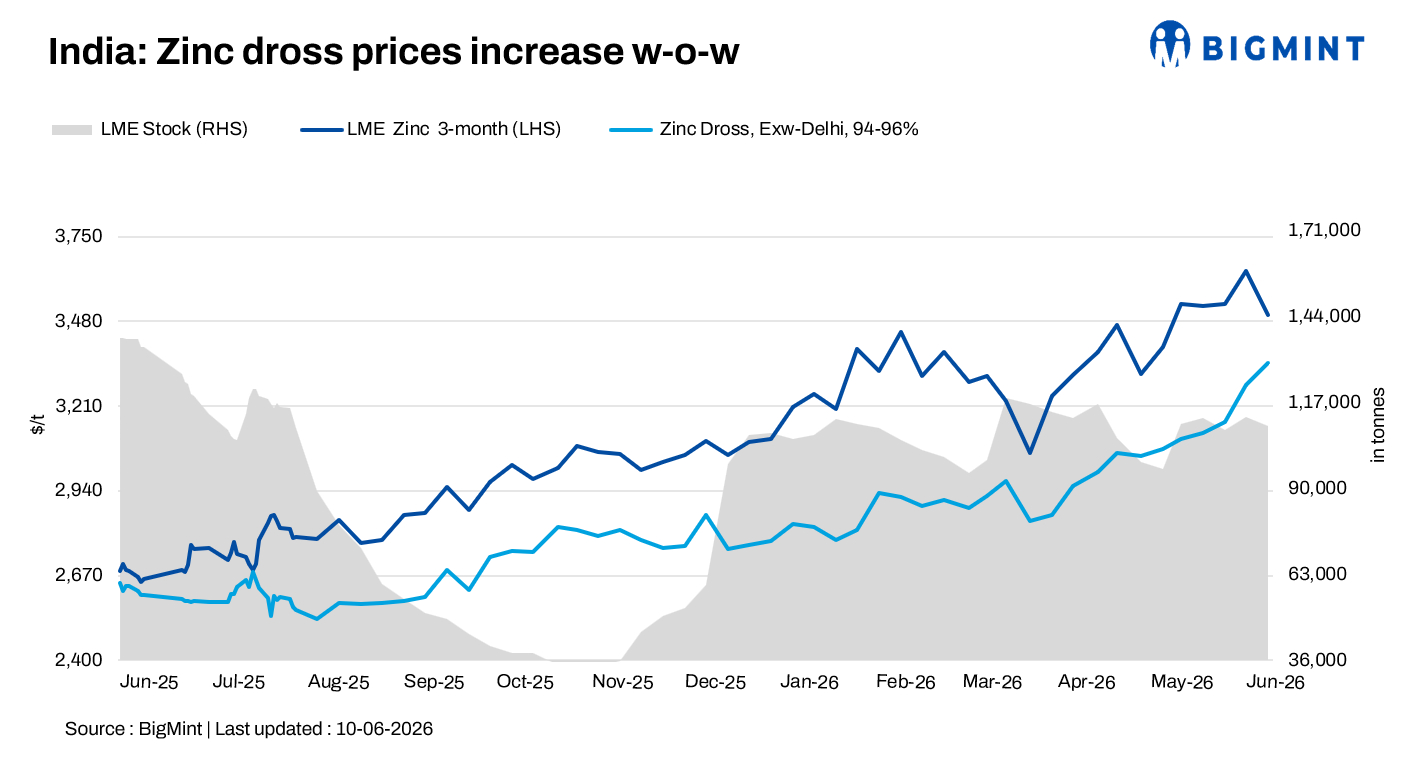

India's zinc dross and zinc oxide prices increased further w-o-w as of 10 June 2026, supported by firm replacement costs and the strength seen in London Metal Exchange (LME) zinc prices during the previous weeks. Although benchmark three-month LME zinc prices corrected during the assessment week, domestic secondary zinc markets continued to reflect the impact of earlier gains in the global market.

Benchmark three-month LME zinc prices averaged around $3,548/t during the week ended 10 June, compared with approximately $3,615/t a week earlier. Meanwhile, LME zinc inventories declined to 109,575 t on 10 June from 112,525 t recorded on 3 June, indicating continued withdrawals from exchange warehouses.

Despite the correction in LME prices, domestic market sentiment remained firm, supported by elevated replacement costs and stable demand from key consuming sectors. However, buying activity continued to be driven largely by immediate requirements, with market participants maintaining a cautious approach amid ongoing price volatility.

Zinc dross, oxide price movements

Domestic zinc dross prices increased by around INR 6,900/t w-o-w to approximately INR 321,400/t ex-Delhi. In western India, zinc dross prices were heard at around INR 318,000-319,000/t ex-Mumbai, reflecting continued strength in secondary zinc values despite fluctuations in international markets.

Meanwhile, zinc oxide (99% Zn) prices rose by around INR 8,400/t w-o-w to INR 308,000/t ex-Delhi. Market participants reported stable demand from the rubber and chemical sectors, while higher feedstock costs continued to lend support to oxide prices.

The improvement in realizations across the secondary zinc segment helped sustain positive producer sentiment during the week.

Scrap segment trends

In the north Indian zinc scrap market, large-sized Tukdi (97% Zn) prices were heard at around INR 304,000-305,000/t ex-Delhi. Regular-grade Tukdi was assessed at INR 300,000-301,000/t, while small-sized Tukdi was heard at INR 297,000-298,000/t.

Scrap prices remained largely firm during the week, supported by higher secondary zinc values and limited availability of quality material. However, most buyers continued to avoid aggressive inventory building, preferring to procure material only against confirmed orders and immediate production requirements.

Market sentiments

Market participants indicated that domestic secondary zinc prices continued to draw support from higher replacement costs despite the correction witnessed in LME zinc prices during the week. The decline in exchange inventories also helped support broader market sentiment.

At the same time, buyers remained cautious amid uncertainty over the short-term direction of global zinc prices. Most market transactions continued to be concluded on a need-based basis, with limited speculative activity observed across the market.

Outlook

In the near term, zinc dross and zinc oxide prices are expected to remain supported by firm domestic fundamentals, stable downstream demand, and relatively tight scrap availability. However, continued volatility in LME zinc prices may influence buying sentiment and limit aggressive price increases. Market participants are expected to closely monitor developments in global zinc markets, inventory trends, and domestic demand conditions for further price direction.