India: West African demand supports bulk rice freight rates despite drop in export prices

...

- Non basmati rice export prices drop 1.5% w-o-w

- Freight volatility and weather risks keep market cautious

India's rice freight market showed mixed trends in the week ended 24 June 2026. Steady demand from West Africa continued to support breakbulk freight sentiment, while container routes remained under pressure as shipping lines adjusted pricing amid muted market activity.

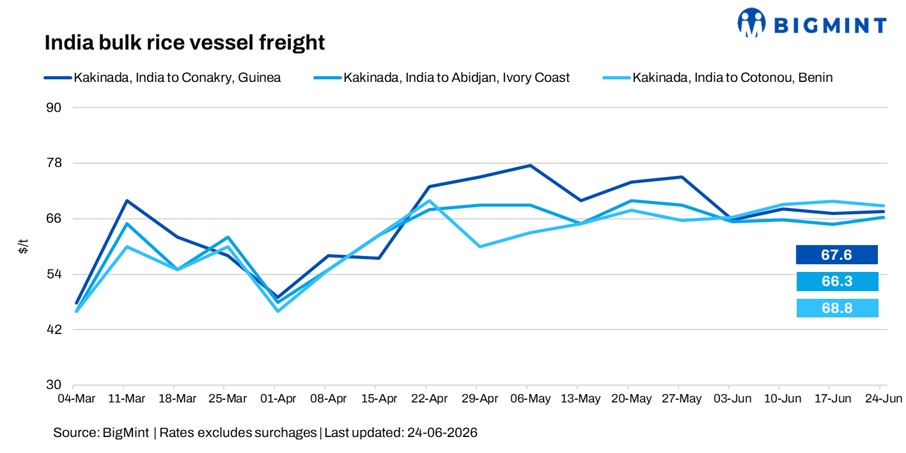

West Africa remained the key market driver during the week, with ongoing enquiries towards destinations such as Cotonou and Mombasa supporting cargo movement. However, market participants noted limited fresh stems during the week, with monsoon-related disruptions contributing to a cautious market mood.

A shipbroker told BigMint, "Rates to West Africa are currently hovering around the $63-69/t range," indicating that the breakbulk market has largely held its ground despite recent freight volatility.

Some traders, however, adopted a cautious approach. A market source said, "I've stopped offering cargoes for now because freight rates have been fluctuating too much. There is no major impact from the monsoon on West Africa shipments yet, although transit times may stretch." The participant added that fixture activity has remained relatively quiet over the last few days.

Route-wise update

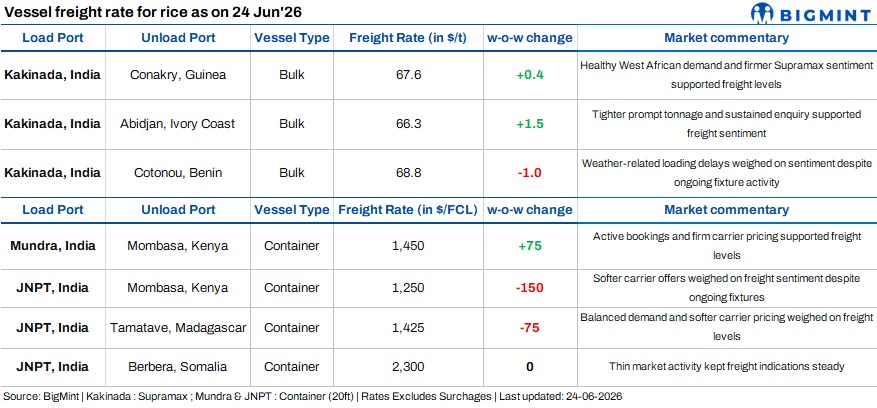

Container market loses momentum

Unlike the breakbulk segment, the container market remained comparatively weaker during the week. Softer carrier offers on select East African routes and limited fresh booking interest weighed on sentiment, even as fixtures continued to be heard in the market.

A shipbroker noted, "Breakbulk freight remains relatively stable, while the container market continues to face pressure," highlighting the contrasting trends across the two segments.

Weather risks in focus

Beyond freight fundamentals, weather developments are also being closely monitored. Concerns surrounding a strengthening El Nino and a delayed monsoon have increased uncertainty around the upcoming kharif season.

An exporter quoted, "Historically, El Nino years have been associated with weaker crop outcomes in Chhattisgarh and Andhra Pradesh. With forecasts pointing towards a stronger El Nino this year, weather-related risks remain elevated."

Another trader added, "Rice prices are already trading at higher levels. If weather-related risks persist during the kharif season, prices could remain firm going forward."

Non basmati rice export prices drop 1.5% w-o-w

BigMint's assessment for Non Basmati parboiled rice export FOB Kakinada fell 1.5% w-o-w to $333/t. Exporters expected domestic basmati prices to come under pressure as cargo movement slowed and uncertainty increased among overseas buyers.

Outlook

Freight sentiment is expected to remain mixed in the near term. West African demand is likely to continue supporting breakbulk freight, while container routes may remain sensitive to carrier pricing and booking activity.

Meanwhile, monsoon progress, El Nino developments and their potential impact on rice availability will remain key factors influencing market sentiment in the coming weeks.