India: US NAPP coal demand slows as petcoke prices correct

...

- High stocks, weak monsoon demand pressure US NAPP coal prices

- Sellers continue to defend offers, buyers resist fresh purchases

The Indian market for US Northern Appalachian (NAPP) coal is entering a softer phase as cement producers reassess fuel economics following a sharp correction in fuel-grade petroleum coke (petcoke) prices. After gaining significant traction earlier this year when petcoke prices surged to multi-month highs, US NAPP coal is now facing renewed competition from cheaper petcoke, comfortable portside inventories, and weakening seasonal demand ahead of the monsoon quarter.

Market participants report that buying activity has slowed considerably in recent weeks, with most consumers adopting a wait-and-watch approach while monitoring developments in petcoke prices, freight markets, and monsoon-driven demand trends.

Retail stocks rebuild as demand softens

Retail stocks of NAPP and Illinois Basin (ILB) coal at India's key import hubs continue to remain comfortable despite steady weekly dispatches.

Combined inventories at Kandla and Tuna stood at approximately 406,000 t as of 15 June, up from around 349,000 t a week earlier. Tuna accounted for about 215,000 t, while Kandla held approximately 191,000 t.

Weekly lifting recovered to around 129,000 t in Week 24, compared with 95,600 t in Week 23. However, traders noted that the improvement largely reflected routine consumption and scheduled dispatches rather than any meaningful recovery in buying sentiment.

Several market participants indicated that cement producers remain adequately covered for near-term requirements and are showing little interest in building additional inventories at current price levels.

Large vessel pipeline weighs on sentiment

The supply outlook remains comfortable.

Market estimates indicate that approximately 225,000 t of retail NAPP coal remains in the floating pipeline, while industrial consumers have close to 900,000 t of additional cargoes either afloat or scheduled to arrive over the coming weeks.

Discharge activity continues across major ports, including Tuna, Kandla, Gangavaram, Dhamra, Dahej, Ennore, and Karaikal.

The sizeable arrival programme raises the possibility of inventories rebuilding further during the monsoon period if consumption slows as expected. Traders, therefore, remain cautious about taking large speculative positions, preferring to focus on clearing existing stocks.

Prices hold but momentum weakens

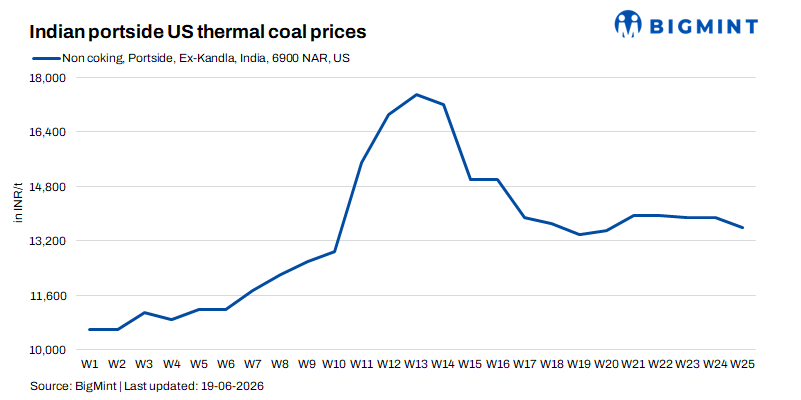

US NAPP coal prices at Kandla and Tuna are currently being heard largely in the range of INR 13,500-14,000/t ex-works, although firm buying interest remains limited.

Several traders reported that while sellers continue to defend offer levels, buyers are increasingly resisting fresh purchases, anticipating further softening if petcoke prices remain weak and inventories continue to build.

Market participants described sentiment as subdued, with most transactions being concluded only for immediate operational requirements.

One trader summarized current market conditions as "need-based buying only," reflecting the lack of urgency among consumers.

Petcoke regains competitiveness

The most important development affecting the NAPP market has been the sharp correction in international petcoke prices.

After reaching multi-month highs during April and early May, fuel-grade petcoke prices have fallen steadily as supply availability improved and buying interest weakened. US-origin high-sulphur petcoke is now being heard in the low-to-mid $130s/t CFR India, significantly below recent peaks.

The correction has narrowed the economic advantage previously enjoyed by US NAPP coal.

Earlier this year, NAPP coal offered a clear discount to petcoke on a delivered energy basis, prompting many cement producers to increase coal consumption and reduce petcoke usage. That advantage has now largely disappeared

With NAPP coal being heard around $133-134/t CFR equivalent and petcoke available at broadly similar levels, buyers are increasingly evaluating fuels based on delivered heat value rather than absolute price.

This has led several cement producers to return to petcoke procurement for incremental requirements.

Cement sector shifts focus to margin preservation

The changing fuel mix is occurring against a backdrop of softer near-term cement market conditions.

The onset of the southwest monsoon is expected to slow construction activity across several regions, prompting cement producers to adopt a more cautious approach toward both production planning and fuel procurement.

While leading cement companies continue to target volume growth ahead of industry averages over the longer term, the immediate focus has shifted toward profitability and cost management. Market participants indicate that recent attempts to raise cement prices have met with mixed success, raising concerns over the sustainability of price increases during the seasonally weaker monsoon quarter.

This has increased the importance of fuel economics.

The recent decline in petcoke prices is expected to generate meaningful savings for cement manufacturers, with industry estimates suggesting potential fuel-cost reductions of around INR 70-80/t of cement production once lower-priced cargoes begin flowing through inventories. Although much of this benefit is expected to be reflected during the September quarter, procurement strategies are already adjusting in anticipation.

As a result, many cement producers are favouring a highly opportunistic purchasing approach, selecting fuels primarily on the basis of delivered heat cost rather than maintaining fixed consumption patterns.

The emphasis on protecting margins rather than pursuing aggressive volume growth is likely to reinforce the current trend toward need-based buying, limiting support for US NAPP coal demand during the monsoon period.

US export market also softens

The international backdrop has become less supportive for US thermal coal.

Recent export data showed US thermal coal shipments declining week-on-week, while FOB values at both Baltimore and New Orleans have softened from recent highs.

India nevertheless remains one of the most important destinations for US thermal coal exports, underlining the continued relevance of the trade despite current demand weakness.

Freight remains a key variable. Any easing in vessel rates could allow suppliers to reduce CFR offers and improve coal's competitiveness. Conversely, renewed geopolitical tensions or freight disruptions could quickly alter the landed-cost equation for both coal and petcoke.

Outlook

The near-term outlook for US NAPP coal in India remains cautious to bearish.

Comfortable inventories, a substantial vessel pipeline, weaker seasonal cement demand, and renewed competition from petcoke are expected to keep buyers on the sidelines.

The market is likely to remain driven by replacement demand rather than fresh stock-building. Unless NAPP coal re-establishes a meaningful discount to petcoke on a delivered energy basis, cement producers are expected to continue favouring flexible, opportunistic fuel procurement strategies.

While any rebound in petcoke prices, tightening freight availability, or geopolitical disruptions could improve NAPP coal's competitiveness, current market conditions suggest spot activity will remain subdued through much of the monsoon quarter.

The balance of risks, therefore, points toward continued pressure on ex-wharf prices, with sellers likely to compete more aggressively for limited buying interest.