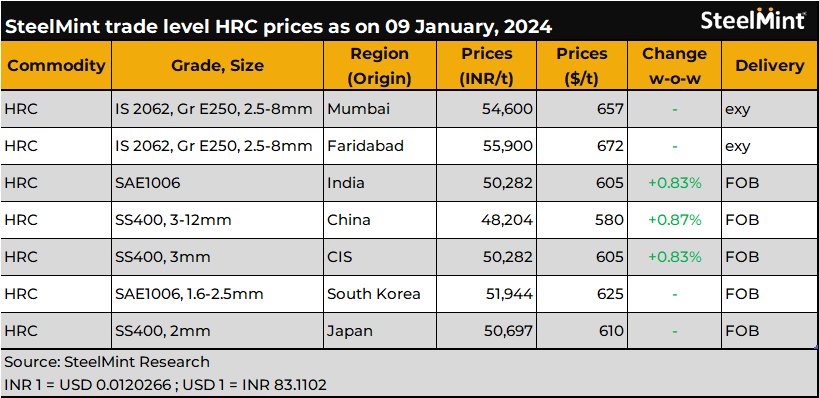

India: Trade-level HRC, CRC prices remain range-bound amid ample availability of cheaper alternatives

...

The prices of trade-grade hot-rolled coils (HRCs) and cold-rolled coils (CRCs) exhibited a stable range within the evaluated markets throughout the review timeframe. Prevailing sluggish trade, coupled with subdued market sentiments, influenced by more affordable domestic alternatives, exerted considerable pressure on prices. Furthermore, despite efforts by mills to implement price increases, they were ineffective in instilling optimism within the market.

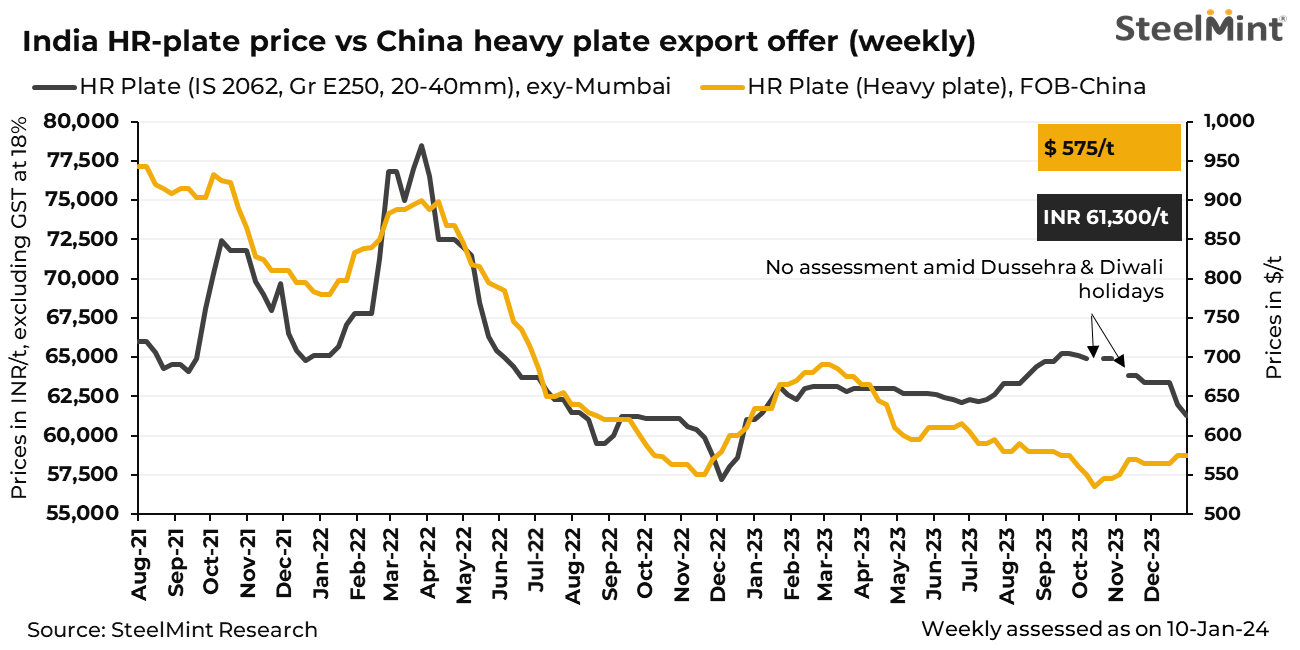

Meanwhile, SAIL put its plate mill at Bhilai Steel Plant under maintenance as of 10 January 2024. Total production loss to be incurred is estimated at around 186,000 tonnes (t) in the 45 days maintenance timeline. Technical upgradation, general maintenance, and re-calibration of rollers are the primary activities to be carried out, informed a few industry sources.

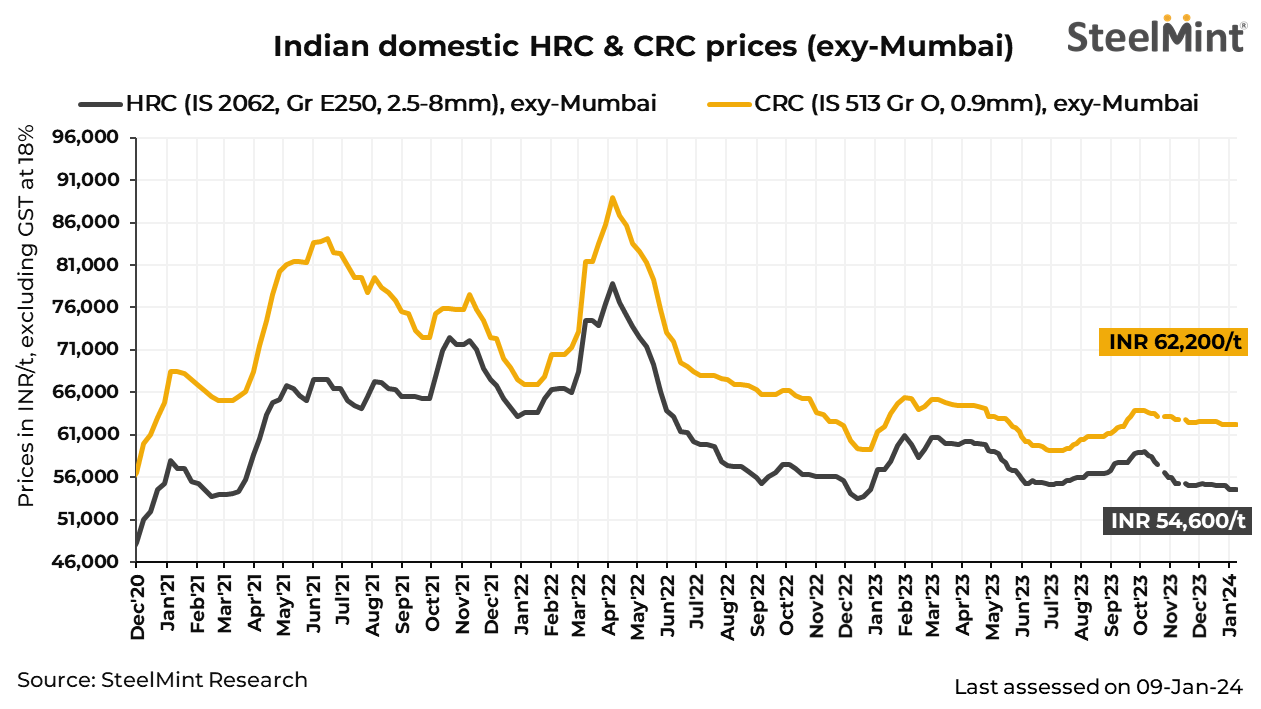

SteelMint's bi-weekly benchmark evaluation for HRC (IS2062, Gr E250, 2.5-8mm) maintained stability on 9 January, 2024, reaching a settlement at INR 54,600/t ($656/t). Concurrently, the prices of CRC (IS513, Gr O, 0.9mm) also exhibited stability, remaining at INR 62,200/t ($748/t) during the same period. (Exchange rates: INR 1 = USD 0.0120236 ; USD 1 = INR 83.1698)

Meanwhile, the weekly assessed hot-rolled plates (IS2062, Gr E250, 20-40mm) prices dropped by INR 700/t ($8/t) to hover at an average INR 61,300/t ($737/t) within the wider range of INR 57,000-65,000 ($685-781/t). The previous week's levels were in the range of INR 57,500-67,000/t ($691-805/t) exy-Mumbai. Private mills continued to enjoy good order books with exports and business-to-customer (B2C) sales orders. These prices are on an exy-Mumbai basis and exclude GST at 18%.

Market updates:

1. Domestic trade-level prices under pressure amid cheaper alternatives: The trade market was under pressure from the ample supply of cheaper domestic alternatives with participants only adhering to need-based buying. The recent price hike from mills failed to lift the mood of the market.

"The price hike announced by mills is not providing any support as the market has ample supply of cheaper domestic and imported materials," a market participant opined. "As long as the inventories or cheaper alternatives are available it will be tough to hike prices and thus these could stay stable for a while," he added.

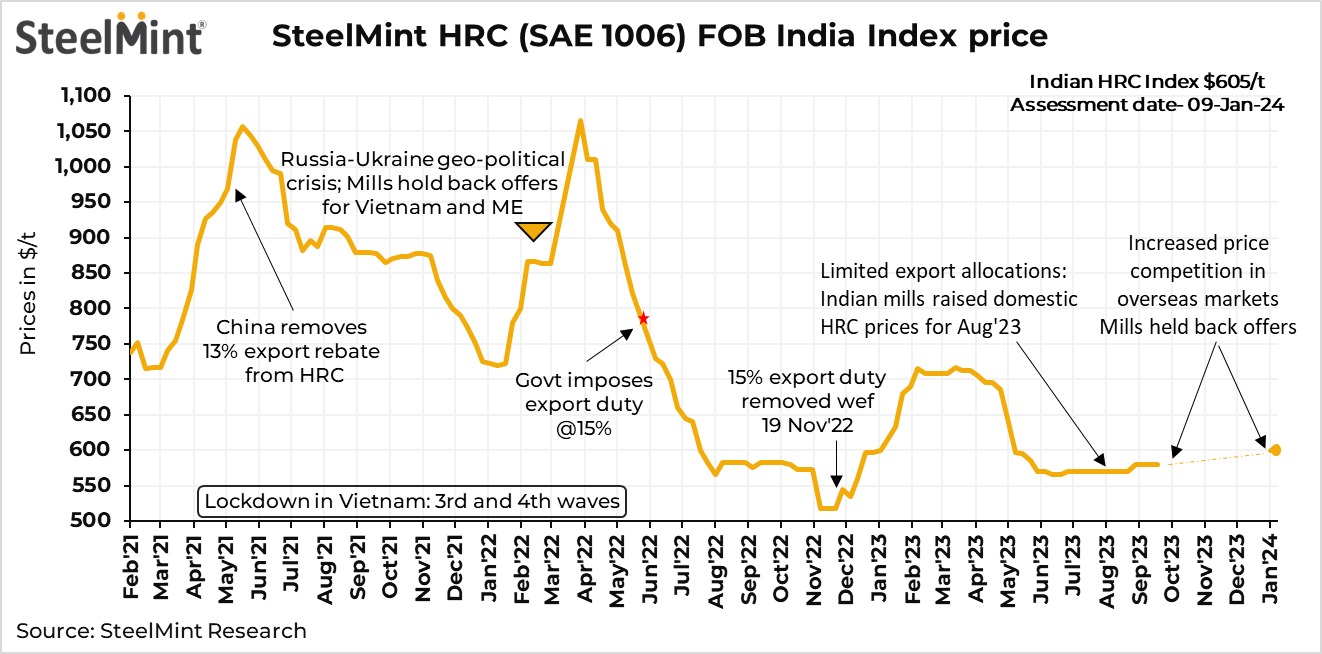

2. SteelMint's India HRC export index rises: SteelMint's India HRC (SAE 1006) export index for the Middle East and Vietnam increased to $605/t FOB east coast India, up from $600/t FOB the previous week. After a hiatus, mills re-entered the Middle East market with new offers last week, and this week saw their return to Vietnam after an extended absence.

Indian HRC exports to Europe remained unchanged, while European domestic prices are rising.

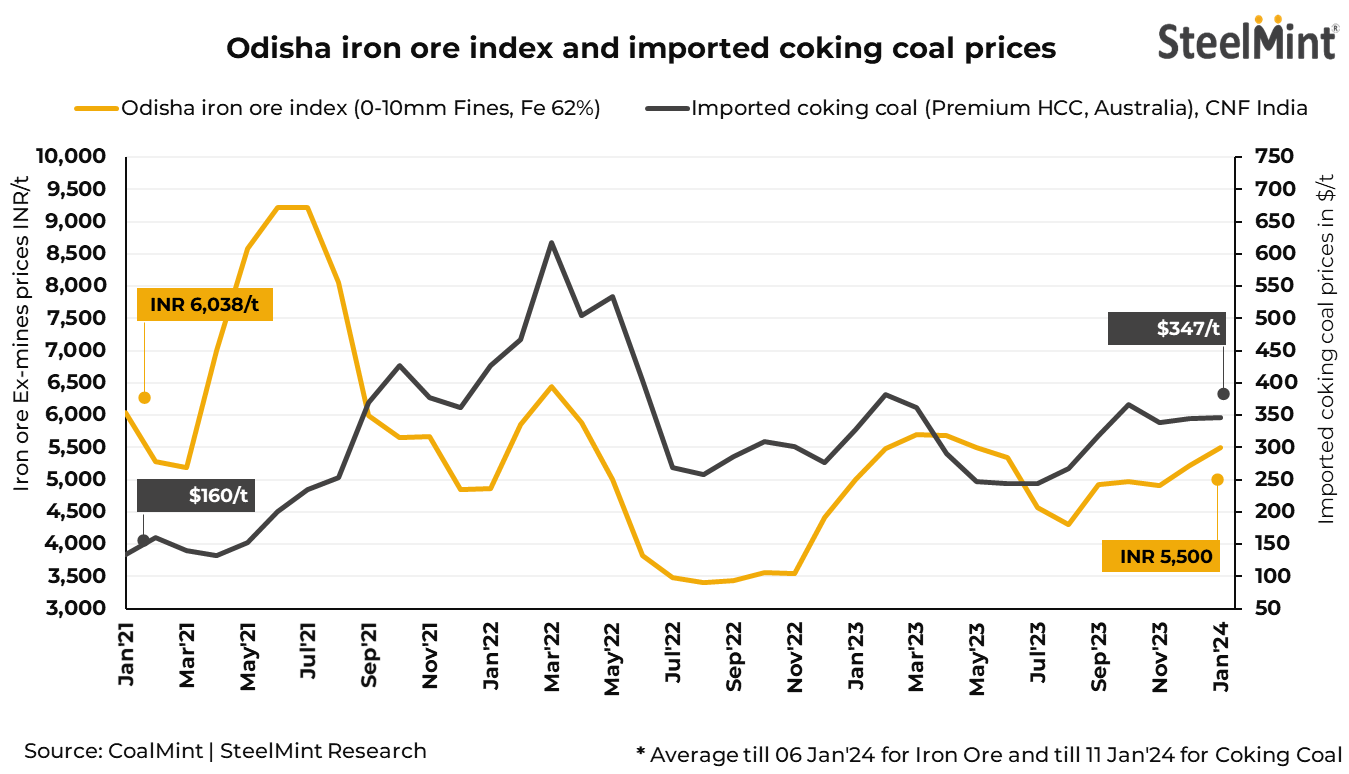

3. Raw material prices increase: The prices exhibited an upward trajectory despite market fluctuations exerting cost pressure on mills. In January 2024, the monthly average price of Odisha iron ore index (0-10mm Fines, Fe 62%) reached INR 5,500/t ($63/t) ex-mines, reflecting an increase of INR 280/t ($5/t) compared to the preceding month's closing figures. In a parallel development, the monthly average rates for imported premium hard coking coal (HCC) of Australian-origin also experienced an uptick, rising by $3/t m-o-m to reach $347/t CNF Paradip, India by the end of December.