India: Supply-driven rally continues in foundry scrap markets; margins remain under pressure

...

- Restricted supply continues to support prices

- Elevated raw material costs squeeze profitability

Domestic foundry scrap markets across India recorded broad-based w-o-w increases, with notable gains in the western and southern regions, while the eastern market showed comparatively moderate movement. The overall market sentiment remained supported by active procurement from foundries and relatively tighter material availability across key trading hubs, reflecting a firm underlying demand environment.

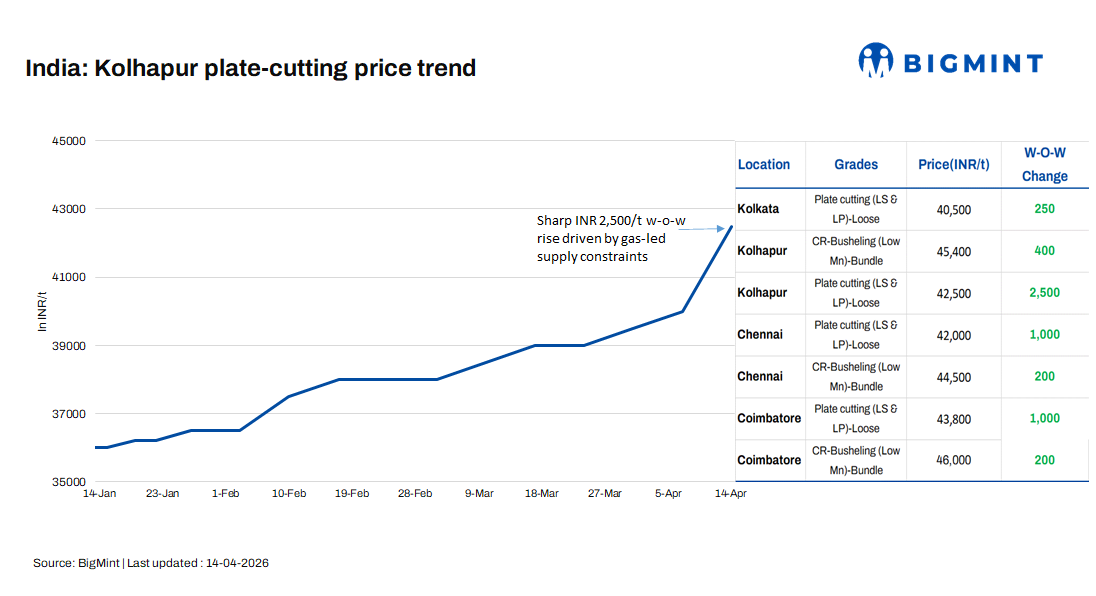

Western India leads the uptrend

In Kolhapur, prices recorded sharp gains, particularly in plate-cutting scrap:

Plate-cutting scrap (4-8 mm) increased significantly by INR 2,500/t to INR 42,500/t

CR-busheling (low Mn) rose by INR 400/t to INR 45,400/t

The sharper rise in plate scrap reflects tightening availability in secondary grades, while relatively moderate gains in CR-busheling indicate continued but controlled shortage of prime scrap, amid limited generation from OEMs and restricted CRC availability.

South India markets maintain steady strength

Southern markets continued to exhibit consistent upward movement, supported by ongoing procurement activity:

Coimbatore

Plate-cutting scrap increased by INR 1,000/t to INR 43,800/t

CR-busheling rose by INR 200/t to INR 46,000/t

Chennai

Plate-cutting scrap moved up by INR 1,000/t to INR 42,000/t

CR-busheling increased by INR 200/t to INR 44,500/t

The steady rise across both regions indicates sustained buying interest, with market participants accepting higher prices amid limited scrap inflows and tightening supply conditions.

Eastern region shows controlled movement

Kolkata

Plate-cutting scrap (4-8 mm) increased by INR 250/t to INR 40,500/t

The relatively moderate increase suggests a more balanced demand-supply scenario, although availability constraints continue to lend underlying support to prices.

Supply-side constraints remain key driver

Market momentum continues to be dominated by structural supply limitations, as scrap generation remains restricted due to subdued OEM production levels, with many units operating at reduced capacity. Additionally, limited availability of import-dependent CRC material is constraining the generation of CR-busheling, keeping prime scrap supply tight.

Notably, plate-cutting scrap has witnessed relatively sharper price increases compared to CR-busheling, driven by gas cutting constraints and lower generation of heavy melting scrap, which has further tightened availability in secondary grades and pushed prices higher across key markets.

At the same time, escalating geopolitical tensions between Iran and the United States are adding further cost pressure through higher energy prices and elevated freight rates, increasing overall replacement costs for foundries.

Outlook

Foundry scrap prices are expected to continue their upward trend in the near term, as scrap generation remains restricted from OEMs and gas-related constraints persist. As long as these conditions continue, prices are likely to witness further w-o-w gains, supported by tight supply fundamentals.