India: Steel prices soften in May'26 while raw materials show mixed trend

...

- Iron ore drops sharply post OMC auction, coking coal firm

- IF steel prices fall to 4-month low on construction sector blues

- Firm raw material prices may rein in steel price decline in June

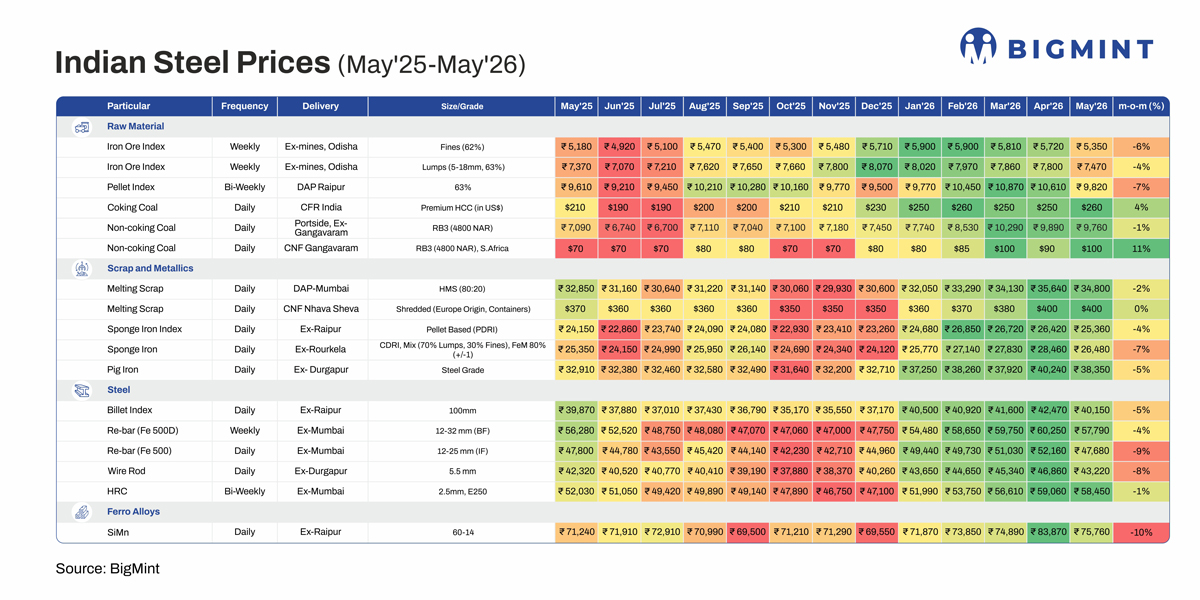

Morning Brief: Domestic steel and raw material prices, excluding coal, witnessed corrections in May 2026 as steel market conditions softened due to a slowdown in construction activity. Slower project execution and higher working capital and logistics costs kept buying activity subdued. In the long steel segment, an intense heatwave slowed construction activity, reducing enquiries from project and retail customers.

However, overall manufacturing momentum and the slight push in exports kept flat steel prices largely stable compared with the steep drop in long steel and semis. The sharp depreciation of the INR made exports more lucrative while imports became unviable. Landed costs of imports remained higher than domestic steel prices, thereby alleviating the pressure on prices. This accounts for the fact that rebar prices dropped 4-9% m-o-m in May due to soft construction sentiment, while HRC fell just 1%.

Crude steel production rose by 3% on-month in May to over 14 mnt, while the HSBC PMI surged to 55, indicating largely positive growth-oriented signals. This drove market momentum.

Snapshots of price movements in May

Iron ore & pellets: BigMint's Odisha iron ore fines index fell by 6% while the lumps index dropped 4% m-o-m. Prices started declining in the second half of May on pressure from declining steel prices and the drop in bids at OMC's monthly auction for May.

In OMC's iron ore fines auction for 1.97 mnt (Fe 51-65%) on 20 May, 1.37 mnt (70%) was booked at INR 3,550-5,150/t; with bids (weighted average) dropping by INR 700/t m-o-m.

BigMint's domestic pellet index, PELLEX, dropped 7% m-o-m in May. Pellet prices softened following the decline in sponge iron and billet prices due to pressure from the steel market. Weak domestic demand led to brisk export sales.

Coking & non-coking coal: India's import prices of coking coal increased by 4% m-o-m as global prices edged up on tight Australian supplies and higher bids by suppliers. Mine accidents in China and successive rounds of hike in coke prices also propped up seaborne coking coal prices.

While low-grade coal prices at the India portside witnessed a minor correction, South African imported coal prices increased by 11% m-o-m amid the continuing Middle East conflict and its impact on freight and fuel costs.

Melting scrap: Domestic melting scrap prices fell by 2% m-o-m on muted steel market sentiments. Heatwaves in many regions of the country impacted construction and industrial activity, weighing on steel demand. Subdued sentiment and slower offtake resulted in a correction in domestic scrap prices.

Imported scrap prices remained flat, with declining domestic prices weaning buyers away from imports. Supply surfeit, weak steel market conditions and rebar export demand in Turkiye weighed on global scrap prices.

Sponge iron: Average prices of pellet and iron ore lump-based sponge iron declined by 4-7% m-o-m mirroring the weakness in the steel and semis markets. Weak construction sentiment led to induction furnace steel prices falling to a four-month low in May which weighed on sponge iron prices. Additionally, the decline in export offers due to bearish demand also impacted prices.

Pig iron: Blast furnace grade pig iron prices fell by 5% m-o-m reflecting the overall soft steel market conditions. Need-based procurement and muted trade demand weighed on prices. However, firm coke costs and buoyant export demand restricted prices from falling further.

Billet: Weak induction furnace steel market sentiments weighed on billet prices, with BigMints billet index dropping 5% m-o-m. Persistent weakness in finished steel demand and limited offtake forced billet producers to lower offers to attract buying interest.

Rebar: IF rebar fell to a four-month low on subdued trade, weak end-user demand, and limited order bookings. Heatwaves and labour shortages disrupted construction activity across several regions, resulting in slower steel consumption and cautious procurement.

BF rebar prices softened in late May as distributors reduced offers amid persistent selling pressure and slower construction-linked demand. Buyers continued following a need-based procurement strategy amid uncertain pricing trends and delayed project execution during the monsoon phase.

On the other hand, the widening gap with IF-route rebar prices, which softened throughout May, impacted BF rebar prices. Supply-side pressure remains a key concern. Inventories at major mills reportedly increased materially entering the quarter, while distributors continue holding elevated stock levels amid slower market movement and softer project offtake.

HRC: Leading steelmakers had initially revised their list prices upward for early May, raising both HRC and CRC prices by INR 1,000/t ($11/t). The price uptick was driven by scheduled maintenance shutdowns at key steel mills. These planned outages temporarily constrained HRC production by approximately 10-15%.

However, market conditions remained weak through late May, with buyers restricting procurement to immediate requirements and distributors reporting slower movement across regional markets. Mills continued focusing on inventory liquidation and dispatch discipline amid subdued spot demand and cautious downstream participation.

That said, fresh exports bookings amid currency depreciation and the uptick in Chinese HRC prices provided some support to HRC prices in late May, which accounts for the relatively stable performance of HRC in May.

Silico manganese: Domestic silico manganese prices fell sharply by 10% on month due to due to weak demand, sluggish export activity, higher supply levels and inventories amid cautious buying, and competitive domestic pricing pressure. The sharp drop in manganese ore prices (imported) also impacted domestic silico prices.

Outlook

The upcoming monsoon months are a weak period for steel prices, especially long steel prices, due to subdued construction activity and material movement. However, manufacturing momentum and crude steel production edged up in May from April levels and are expected to keep HRC prices largely supported. That said, trade restrictions in the form of EU safeguard quotas are expected to weigh on export sentiments and domestic HRC prices.

But NMDC has increased iron ore prices slightly for June, while coking coal prices remain firm following China mine accident and tight supply conditions. Firm raw material prices may rein in the drop in steel prices in June and a rangebound trend is what is most expected.