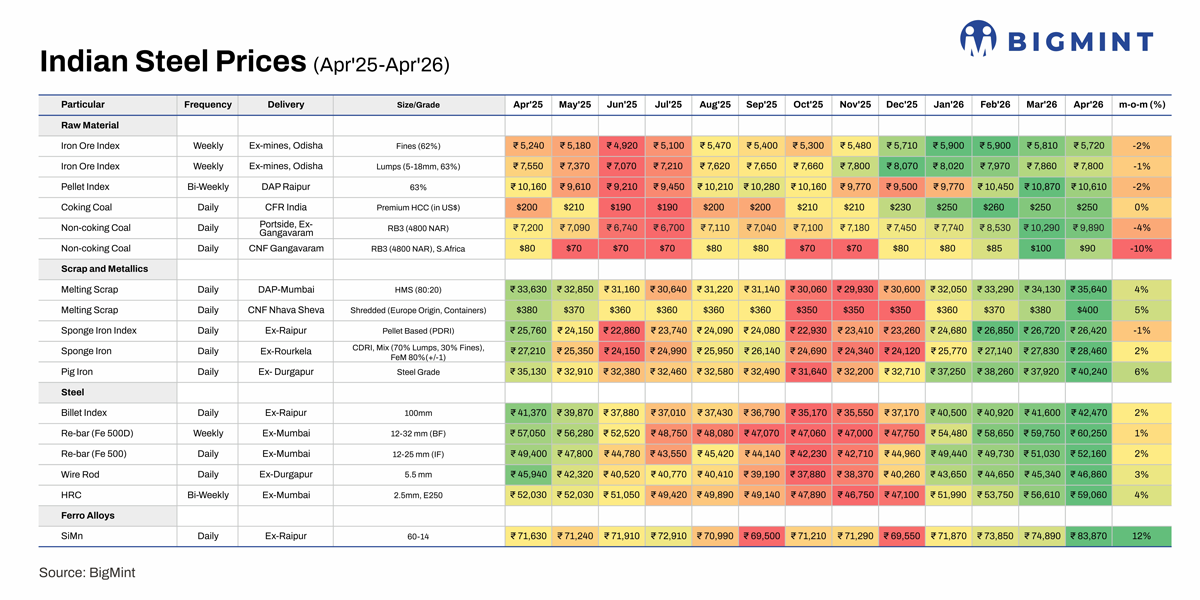

India: Steel prices rise m-o-m in Apr'26, led by stronger gains in flat steel

...

- HRC prices rise 4% m-o-m, outpacing long steel

- Iron ore and coal decline, while scrap and pig iron increase

- Silico manganese prices surge 12% m-o-m, marking the sharpest increase

Morning Brief: Indian steel prices increased m-o-m in April 2026, with gains observed across both long and flat steel segments, led by stronger increases in flat steel. The uptrend comes despite softer movement in key bulk raw materials such as iron ore and coal, indicating that the current price cycle is being driven by tightening metallics, mill-side price revisions, and supply-side factors rather than broad-based input cost inflation.

At a structural level, India's steel sector continues to be supported by capacity-led growth, with crude steel production rising 10.5% y-o-y to 168 mnt in FY'26, driven by sustained capacity additions and stable utilisation levels. Iron ore production also increased 7% y-o-y to 310315 mnt, with higher merchant output offsetting a decline in captive production, ensuring adequate availability across the system.

Demand conditions, however, remain measured rather than broad-based. While macro indicators such as IIP and automotive production point to healthy underlying activity, market-level buying continues to be driven largely by low inventories and the need to secure material at prevailing prices, rather than a strong expansion in end-use consumption.

On the supply side, mill price hikes in early April and maintenance shutdowns at select facilities have tightened availability in the domestic market. In addition, disruptions across key maritime routes and higher freight costs have impacted trade flows, particularly in flat steel, supporting domestic prices and reinforcing the upward trend.

Iron ore: Iron ore prices declined m-o-m in April, with fines (62%) down 2% to INR 5,720/t and lumps falling 1% to INR 7,800/t, while pellet prices also decreased 2% to INR 10,610/t. The decline was driven by improved domestic availability, as higher production and strong merchant supply weighed on prices. Auction trends also reflected softer realisations, with weighted average bids declining m-o-m despite some premiums over base prices.

Coal: Coking coal prices remained stable at $250/t, supported by sustained import dependence amid strong steel production. In contrast, non-coking coal prices declined, with domestic RB3 down 4% to INR 9,890/t and imported prices falling 10% to $90/t, reflecting weaker demand from end-use sectors and improved domestic supply. Overall, easing coal prices reduced cost pressure across the value chain.

Scrap and metallics: Domestic scrap prices increased 4% m-o-m to INR 35,640/t, while imported shredded scrap rose 5% to $400/t, reflecting tightening availability. This comes despite a 24.5% y-o-y increase in domestic scrap availability, indicating that demand from electric route producers continues to absorb incremental supply and support prices.

Sponge iron prices increased 2% m-o-m to INR 28,460/t, although the index declined marginally by 1%, reflecting mixed movement amid softer coal prices. Pig iron prices rose more sharply by 6% to INR 40,240/t, supported by steady demand from downstream segments. Overall, metallics provided the primary cost support to steel prices in April, offsetting weakness in bulk raw materials.

Steel

Billet: Billet prices increased 2% m-o-m to INR 42,470/t, supported by firming metallic input costs, particularly scrap and pig iron. However, the increase remained moderate, as easing iron ore and coal prices limited broader cost pressures and downstream demand remained cautious.

Rebar: BF rebar prices rose 1% m-o-m to INR 60,250/t, while IF rebar increased 2% to INR 52,160/t, indicating relatively slower gains in the long steel segment. Demand remained steady but measured, with buyers cautious at elevated price levels and procurement largely driven by immediate requirements. Although inventory levels remained low, the absence of strong end-use demand limited sharper price increases.

Wire rod: Wire rod prices increased 3% m-o-m to INR 46,860/t, tracking the broader trend in long steel. Demand from construction-linked applications remained steady, supporting prices, although gains were broadly aligned with the moderate movement seen in rebar.

HRC: HRC prices rose 4% m-o-m to INR 59,060/t, marking the strongest increase among finished steel products. The sharper increase reflects mill-side price hikes implemented in early April and tighter availability due to maintenance-related disruptions. In addition, disruptions across key maritime routes, higher freight costs, and subdued export competitiveness have supported domestic pricing by limiting import pressure.

Ferro alloys

Silico manganese: Silico manganese prices surged 12% m-o-m to INR 83,870/t, marking the strongest increase across the value chain. The rise was driven by firm global manganese ore prices and tightening supply conditions, which increased input cost pressures for steelmakers despite measured domestic demand. However, towards the end of the month, prices declined on lower export inquiries and improved domestic availability.

Outlook

We expect steel prices to remain under pressure in the near term on easing iron ore and coal prices, posing indications that the current uptrend is not being driven by broad-based raw material inflation.

With demand remaining measured and largely inventory-driven, price movement will depend on supply-side developments and the sustainability of flat steel strength. Continued tightness in vessel freight rates and external trade uncertainties are likely to keep a floor under prices, even as underlying demand remains moderate.