India: Steel prices remain stable amid margin pressure in south India

...

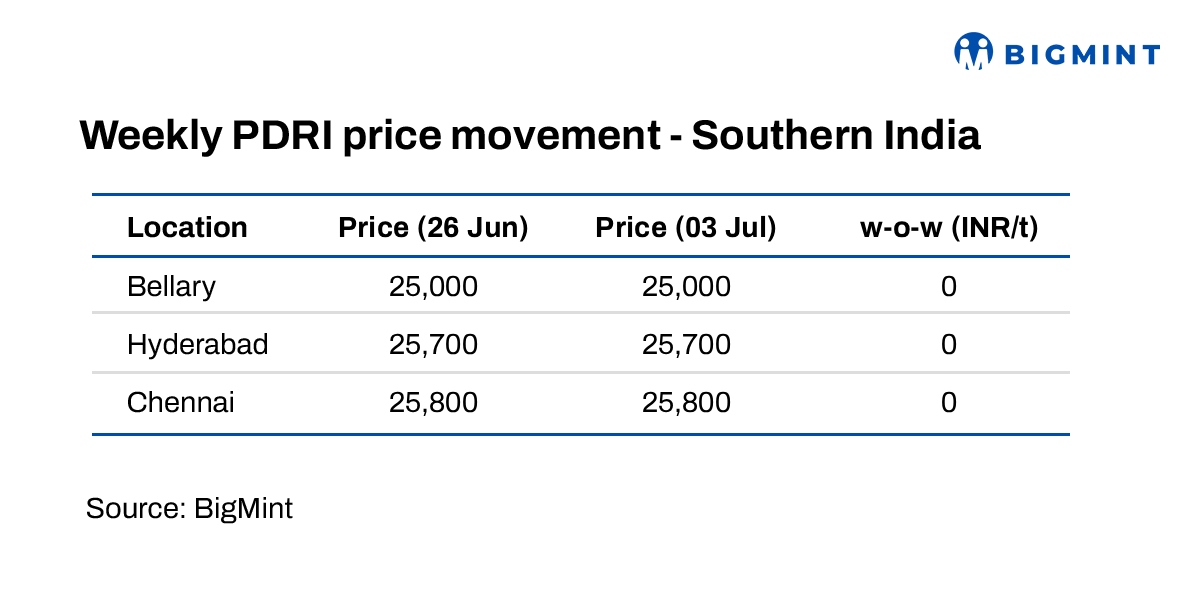

- Bellary sponge iron prices at INR 25,000/t

- Chennai billet prices rise INR 800/t w-o-w

Sponge iron & melting scrap

South India's sponge iron market remained largely stable during the week ended 3 July 2026, as weak downstream steel demand offset easing raw material costs and kept prices rangebound. Bellary sponge iron prices remained unchanged at INR 25,000/t ex-works despite limited buying interest from steelmakers across the region.

Market participants indicated that sponge iron consumers attempted to negotiate lower prices amid sluggish finished steel sales. However, producers resisted price reductions as operating margins remained compressed, leaving little room for further corrections. Sponge iron units in the Bellary cluster continued to operate at around 60-70% capacity utilisation levels, reflecting cautious production strategies amid uncertain demand conditions.

Raw material prices reflected mixed signals during the week. Iron ore pellet (Fe-63%) prices remained stable at INR 9,800/t ex-Bellary, while RB2 coal prices declined by around INR 500-600/t w-o-w to INR 10,600/t ex-Gangavaram, providing modest cost relief to sponge iron manufacturers.

Meanwhile, the ferrous scrap market weakened, with HMS (80:20) prices in Chennai declining by INR 300/t w-o-w to INR 31,000/t as of 3 July. The decline was mainly driven by weak buying interest from steel producers, who preferred alternative raw materials available at more competitive prices. Additionally, higher scrap availability and sluggish finished steel demand forced scrap traders to reduce their offers to stimulate transactions.

Despite muted downstream demand, sponge iron trading activity improved considerably during the week. Trade volumes captured during the assessment period increased by around 25-30% compared with the previous week, with approximately 15,000 t of pellet-based DRI transactions concluded during the trading window. Market participants attributed the increase largely to replenishment buying and short-term inventory adjustments rather than a structural improvement in steel demand.

MS Billet :

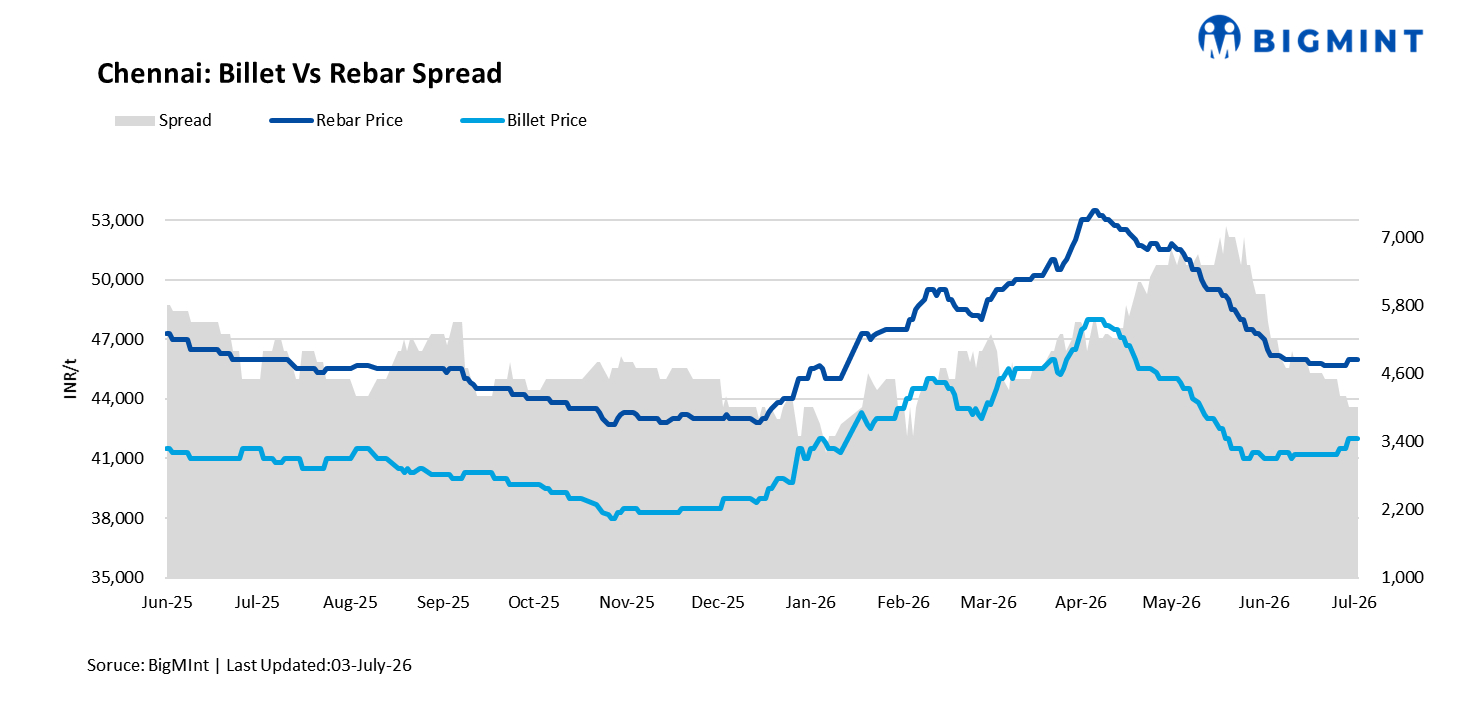

In the semi-finished segment, mild steel billet prices in Chennai increased by around INR 800/t w-o-w as merchant billet suppliers attempted to recover narrowing conversion margins. The spread between HMS (80:20) scrap and MS billets widened to approximately INR 11,000/t, supporting higher billet offers despite the absence of meaningful improvement in finished steel offtake.

Merchant billet transactions remained limited overall, as re-rollers avoided building inventory positions and continued to purchase only against confirmed orders due to slow movement in finished steel products.

Rebar :

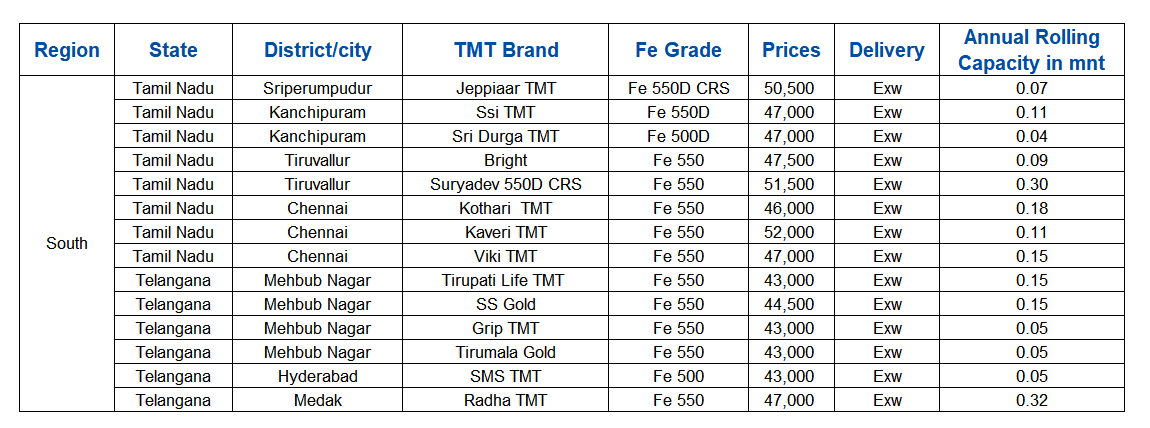

The finished steel segment remained under pressure across southern India. Induction furnace route rebar prices remained stable week-on-week at INR 43,000/t ex-Hyderabad and INR 46,000/t ex-Chennai, supported by stable input costs but constrained by weak construction demand and limited project execution activity.

Rebar inventories across mills and re-rolling units were estimated at around 30-40 days of sales, depending on plant size and production scale, reflecting slower dispatches and elevated stock positions across the region.

Meanwhile, blast furnace route rebar prices continued to decline, falling to around INR 51,500/t ex-yard Hyderabad and INR 52,000/t ex-yard Chennai. As a result, the premium of integrated route material over induction route rebar narrowed to around INR 7,000-7,500/t in the Hyderabad market, intensifying competitive pressure on secondary producers.

Market sentiment remained cautious as buyers continued to follow hand-to-mouth procurement strategies amid weak visibility on construction demand and the ongoing monsoon season.

However, some support for demand expectations emerged during the period after a large integrated water and urban infrastructure package worth around INR 4,500 crore was floated in Telangana during June 2026. The project attracted participation from major EPC contractors including Megha Engineering & Infrastructures Limited, NCC Limited and Larsen & Toubro. Market participants expect project execution to support long steel demand in the region once work orders are awarded and site mobilisation begins.

Outlook

Prices across the south Indian steel value chain are expected to remain largely stable through July, with limited conversion margins preventing aggressive price cuts by manufacturers.

However, monsoon-related disruptions and the absence of immediate project execution are likely to keep procurement activity cautious over the coming weeks, with any meaningful recovery in demand expected to depend on the pace of infrastructure implementation in the second half of the quarter.