India: Sponge iron export prices stable even as buying activity improves

...

- Weekly export offers show limited movement

- Weak steel demand continues to cap price upside

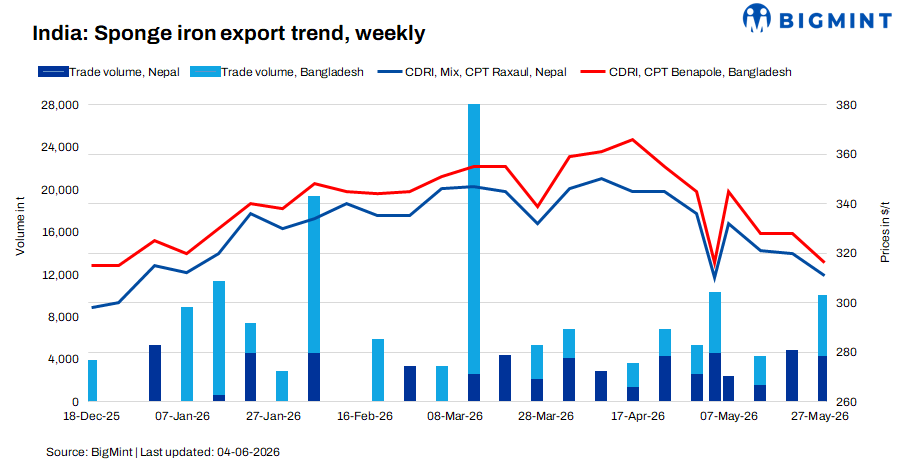

India's sponge iron (DRI) export market remained largely range-bound this week, with export offers showing only marginal movement despite improvement in booking activity.

As per BigMint's weekly assessment, export offers to Nepal edged down by $1/t w-o-w to $310/t CPT Raxaul, while offers to Bangladesh remained unchanged at $316/t CPT Benapole. Market participants reported that approximately 10,000 t of sponge iron deals were concluded for Nepal and Bangladesh combined during the week, indicating better buying interest compared to recent weeks.

The improvement in bookings was supported by buyers re-entering the market at current price levels after several weeks of cautious procurement. However, participants noted that enquiries and bids continue to remain concentrated at lower levels, highlighting the absence of strong demand-side support. While trading activity improved, buyers remained reluctant to accept higher offers due to weak finished steel offtake.

Market sources indicated that Bangladeshi buyers are currently comfortable booking within the range of $315-320/t CPT Benapole, while Nepal buyers are active within the range of $310-315/t CPT Raxaul. These working levels have established a trading band for the market, limiting significant upside in export offers despite slight improvement in volumes.

Nepal budget brings no major changes

Market participants also assessed the impact of Nepal's recent budget announcement. No changes were introduced for sponge iron imports or semi-finished steel products, suggesting limited direct implications for cross-border DRI trade in the near term.

Overall, India's sponge iron export market displayed greater stability this week compared to recent periods of sharp price fluctuations. While improved bookings suggest that buyers are becoming more comfortable at prevailing price levels, persistent weakness in finished steel demand continues to cap aggressive procurement. In the near term, export offers are expected to remain range-bound, with market direction depending on downstream steel demand recovery in Nepal and Bangladesh and the ability of sellers to maintain competitive pricing.