India: South African thermal coal portside prices fall, buyers wait for further softening in offers

...

- Buyers remain on sidelines, sponge iron prices range-bound

- Freight sentiment weakens as oil prices drop

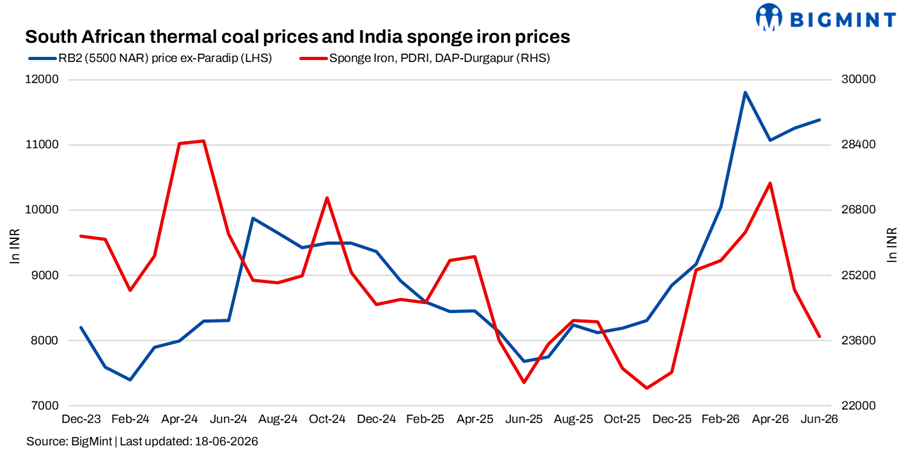

South African thermal coal sentiment remained subdued during the week ended 18 June despite lower freight rates and easing geopolitical concerns. As per BigMint's assessment, ex-Paradip RB2 (5,500 NAR) declined by INR 450/t w-o-w to INR 11,050/t, while RB3 (4,800 NAR) fell by INR 200/t to INR 9,700/t. At Vizag, RB2 dropped by INR 200/t to INR 10,800/t, while RB3 decreased by INR 150/t to INR 9,750/t.

India's coal inventories at major ports declined by 5.7% w-o-w to 14.72 mnt in week 24 from 15.61 mnt in week 23, reflecting stronger evacuation across several key ports.

BigMint assessed CNF Gangavaram RB2 at $113/t, down $5/t w-o-w. Market participants also reported vessel offers around $110/t, indicating growing pressure on sellers to adjust prices amid limited buying interest.

Buying interest remains absent

Market participants reported that enquiry levels remained extremely weak during the week, with most buyers adopting a wait-and-watch approach. Steel and sponge iron consumers largely stayed away from spot purchases, anticipating further softening in imported coal offers.

Participants indicated that sentiment weakened following discussions around a potential US-Iran peace agreement. Buyers have increasingly started bidding around $5/t below prevailing offer levels, expecting lower freight rates and softer import prices in the coming weeks.

Several traders noted that while sellers remained keen to push volumes, actual buying interest remained limited. Procurement activity continued to be restricted to immediate operational requirements, with no significant bulk bookings reported across major consuming regions.

Bunker prices drop w-o-w

Bunker prices decreased by $158/t w-o-w to $658/t on 18 June, as easing geopolitical tensions and the expected reopening of the Strait of Hormuz weighed on crude prices. Lower fuel costs are providing relief to shipping expenses and supporting a softer freight outlook, although lingering security concerns continue to keep market participants cautious.

Softer freight weighs on sentiment

Imported coal offers came under pressure as freight rates softened and geopolitical risk premiums eased. Market participants stated that a formal peace agreement could further reduce freight costs, creating additional downside pressure on seaborne coal offers.

Although international indices also weakened during the week, traders reported no meaningful improvement in buying activity. Most consumers preferred delaying purchases, expecting a price correction over the next one to two weeks.

Participants believe enquiries could improve from next week if prices continue to soften, although actual bookings are likely to depend on downstream demand conditions and monsoon-related consumption trends.

Domestic coal remains competitive

Domestic coal continued to exert pressure on imported cargoes. BigMint assessed 5,000 GCV coal stable at INR 5,500/t, while 4,500 GCV coal remained unchanged at INR 4,050/t w-o-w.

Comfortable domestic availability, regular auction participation and lower procurement costs continued encouraging consumers to prioritise domestic supplies over imported material.

Sponge iron market under pressure

Weak downstream steel demand continued weighing on coal consumption. PDRI DAP-Durgapur prices remained stable w-o-w at INR 23,600/t.

Despite subdued buying interest, sponge iron sellers largely maintained offers, supported by elevated raw material costs, which limited any significant downside in prices. Market participants reported that most transactions were concluded at lower price levels, while bulk bookings remained absent.

Demand from finished and semi-finished steel segments continued to remain weak, limiting sponge iron consumption and keeping overall market sentiment cautious. Several participants noted that while trade volumes improved marginally, confidence in a near-term demand recovery remained low.

Outlook

South African coal sentiment is expected to remain cautious in the near term. Softer freight rates, easing geopolitical concerns and lower import offers may encourage more enquiries in the coming weeks. However, comfortable domestic coal availability, weak sponge iron economics and subdued steel demand are likely to keep procurement largely requirement-based. Market participants will closely monitor freight movements, developments in the Middle East and domestic auction participation for indications of a change in market direction.