India: SECL auction sees strong allocation amid selective premium trends

...

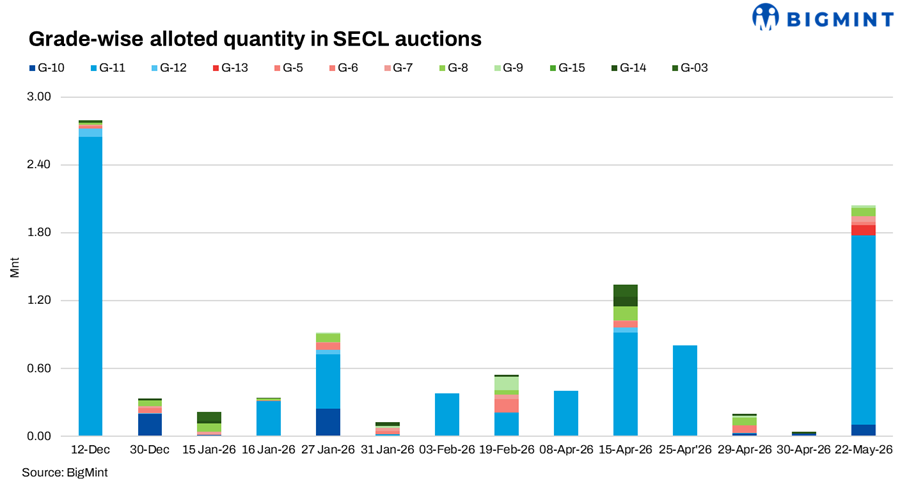

- G11 coal dominates allocations

- G6 records highest premium

SECL's non-coking coal auction held on 22 May 2026 witnessed strong participation, with total allocation reaching around 2.04 mnt against the offered quantity of 2.17 mnt, reflecting healthy absorption levels despite cautious downstream industrial demand.

G11 coal dominated the auction with allocation of around 1.67 mnt at an average winning price of INR 1,612/t against the notified price of INR 1,184/t, translating to a premium of around 36%. Large allocations from Gevra OC and Dipka OC supported overall auction participation, primarily driven by power, cement and industrial consumers.

Among the two major G11 sources, Gevra OC allocated around 1.17 mnt at a relatively moderate premium of nearly 20%, while Dipka OC recorded stronger bidding with a premium of around 66%, indicating selective demand for specific source quality and logistics advantages.

Mid-grade coal records healthy premiums

G10 coal witnessed one of the strongest responses in the auction. Around 106,000 t were allocated at an average winning price of INR 3,006/t against the notified price of INR 1,360/t, reflecting a premium of around 121%.

Amadand OC remained the key contributor in the segment, allocating 100,000 t at an average winning price of INR 3,399/t, implying a sharp premium of nearly 150%, indicating strong industrial preference for the grade despite overall cautious market conditions.

G7 coal from Ketki UG also witnessed healthy participation, with 50,000 t allocated at an average premium of around 41%. Meanwhile, G13 coal from Manikpur OC remained comparatively subdued, recording a premium of around 20% with allocation of nearly 88,650 t.

Higher-grade coal continues attracting strong premiums

Higher-grade coal continued witnessing aggressive bidding in selective pockets. G6 coal from Amera OC recorded the highest premium in the auction, with 30,000 t allocated at an average winning price of INR 5,532/t against the notified price of INR 2,761/t, translating into a premium of around 100%.

Similarly, G8 coal allocated across Bangwar UG, Rajnagar OC, Kanchan OC and Nowrozabad Siding recorded varying premium trends. Overall G8 allocation stood at around 74,000 t with an average premium of approximately 42%.

Kanchan OC witnessed the strongest response within the G8 segment, with premiums reaching around 92%, while Rajnagar OC recorded comparatively moderate premiums near 22%, highlighting selective grade-wise and source-wise demand.

G9 coal allocation remained relatively limited at 22,000 t, with premiums averaging around 35%.

Industrial consumers dominate buyer participation

Buyer participation remained concentrated among power, cement, aluminium and coal beneficiation companies. Rama Coal Washeries emerged as the largest buyer with allocation of 100,000 t of G11 coal.

Vedanta Lanjigarh secured 80,000 t, while Ultratech Cement booked 75,000 t entirely in G11 grade. Bharat Aluminium, Phil Coal Benefication, Phil Steel & Power, JSW Mahanadi Power and Param Mitter Ventures also secured sizeable volumes, largely focused on G11 coal.

The participation pattern reflected continued preference for lower and mid-grade fuel coal among large industrial consumers amid stable operational demand.

Market sentiment remains balanced

The latest SECL auction reflected balanced market sentiment with healthy allocation volumes but selective bidding across grades. Market participants noted that requirement-based buying continued amid weak sponge iron and steel demand, while comfortable domestic coal availability and frequent CIL auctions continued limiting aggressive premiums in several grades.

However, strong premiums in G6, G8 and G10 coal indicated that demand for better-quality and operationally flexible material remained firm despite subdued downstream industrial sentiment.

Outlook

SECL auction participation is expected to remain stable in the near term supported by comfortable industrial coal consumption and regular procurement by large consumers. However, weak sponge iron margins, sufficient domestic coal availability and cautious steel sector demand may continue limiting aggressive bidding across broader coal grades.