India's thermal coal port stocks rise further amid weak demand sentiment

...

- Inventories increase on steady arrivals

- Demand remains cautious across sectors

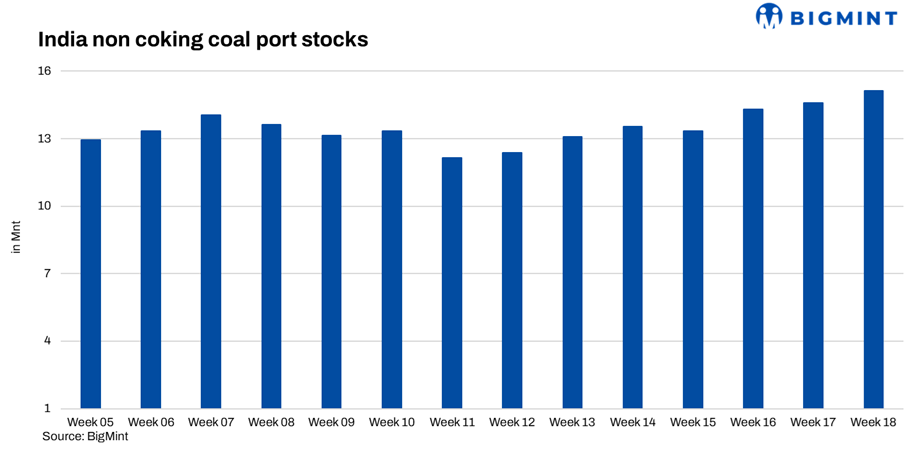

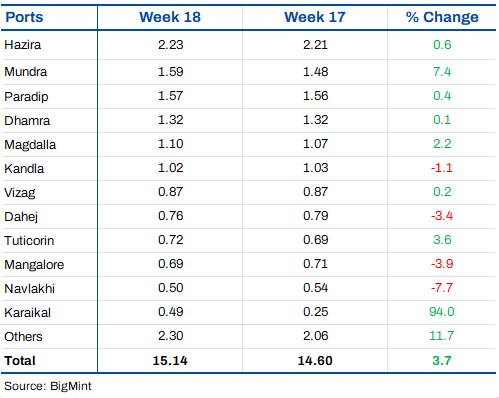

India's non-coking coal inventories at major ports increased by 3.7% w-o-w in Week 18, rising to 15.14 mnt from 14.60 mnt in Week 17, indicating continued supply build-up despite subdued demand conditions. The rise reflects steady cargo inflows, while evacuation remained moderate, keeping overall inventories elevated.

Mixed port trends reflect selective inflows and evacuation

Port-wise trends remained mixed, highlighting a market driven by regional dynamics rather than uniform demand. Incremental gains at ports such as Mundra, Magdalla, Tuticorin, and Hazira indicated continued cargo arrivals and trader positioning. Sharp increases at Krishnapatnam and Karaikal suggest fresh inflows or repositioning of cargoes.

On the other hand, declines at Tuna, Navlakhi, Dahej, and Mangalore pointed to ongoing evacuation and limited new arrivals. Paradip and Dhamra remained largely stable, indicating balanced inflow and offtake at key east coast hubs.

Overall, stock movement suggests routine adjustments rather than aggressive inventory build-up, with traders aligning positions based on local demand and logistics.

Weak demand, price pressure continue to weigh on sentiment

As on 29 April 2026, South African portside thermal coal prices declined further, with ex-Paradip RB2 5,500 NAR falling by INR 200-300/t w-o-w to INR 10,700/t, while RB3 4,800 NAR dropped to INR 9,500/t amid weak sponge iron demand and ample domestic coal availability.

Market sentiment remained cautious during the week, with weak industrial demand continuing to weigh on buying activity. Sponge iron and steel segments showed limited recovery, keeping procurement largely need-based.

Imported coal markets reflected mixed trends. Indonesian prices strengthened on tighter supply and seasonal demand, while South African coal remained under pressure due to weak enquiries, a fall in sponge prices despite some cost-side support from freight and forex. US coal inflows continued, supported by petcoke substitution, though rising arrivals may add pressure ahead.

Domestic coal and ample supply limit import appetite

Domestic coal prices remained relatively stable at lower levels after recent corrections, maintaining their cost advantage over imports. Muted participation in recent auctions and adequate availability continued to keep buyers inclined towards domestic sourcing.

At the same time, rising portside inventories and significant volumes in transit ensured comfortable supply conditions, reducing urgency for fresh import bookings.

Outlook

The continued rise in inventories suggests that supply will remain comfortable in the near term. However, with demand still weak and prices under pressure across segments, significant stock build-up may remain limited.

Going forward, improvement in industrial demand, movement in sponge iron prices, and clarity in domestic coal trends will be key in determining whether inventories stabilise or continue to rise. Until then, the market is expected to remain cautious, with buying driven by immediate requirements rather than stock accumulation.