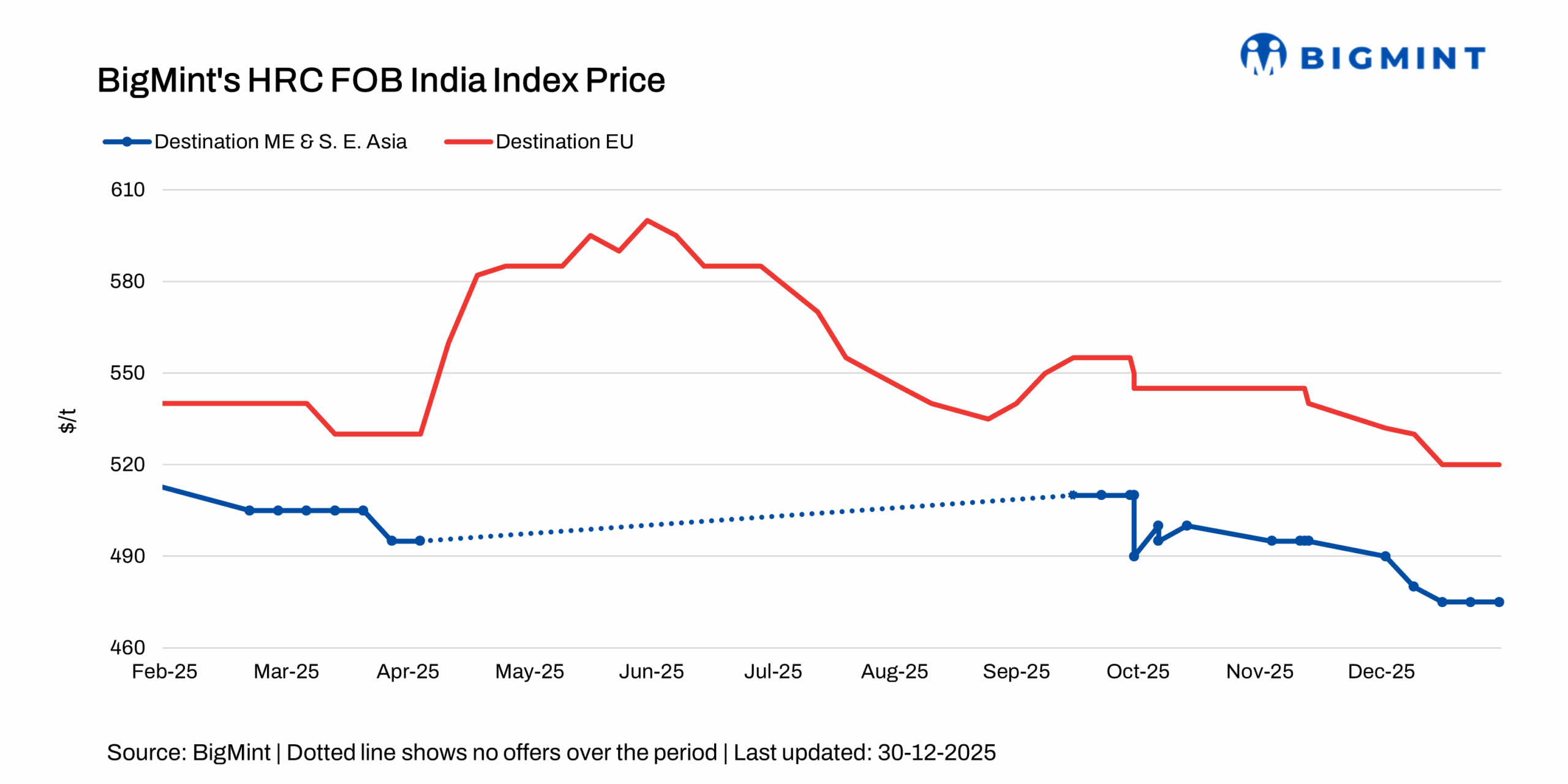

India's HRC export index for EU remains stable w-o-w despite muted trades

...

- EU on holidays, CBAM confusion casts shadow

- Financial year-end in Middle East dents buying interest

BigMint's Indian HRC (S275) export index for the European Union (EU) remained unchanged w-o-w at $520/t FOB main port, as trading activity in the destination markets remained subdued due to the year-end holidays. Indian HRC (SAE 1006) export index for the Middle East also remained stable w-o-w at around $465/t.

1. HRC offers to EU: Indian HRC export offers to the EU remained unchanged w-o-w at $570/t CFR Antwerp, with trading activity in the region remaining muted as European buyers refrained from imports in the midst of the holiday slowdown and persistent CBAM-related uncertainty, which continued to weigh on market sentiment and overall trade activity.

2. HRC offers to Middle East: Indian HRC export offers to the Middle East remained unchanged w-o-w at $490/t CFR UAE. A source told BigMint: "demand in the region remained stable; however, market activity stayed weak as participants were largely occupied in the middle of financial year closing.

However, Chinese HRC export offers to the Middle East increased by $5/t w-o-w to $485/t CFR UAE from $480/t a week earlier. A market participant noted that "fresh offers remained low as exporters are focused on obtaining export permits, resulting in limited active offers currently."

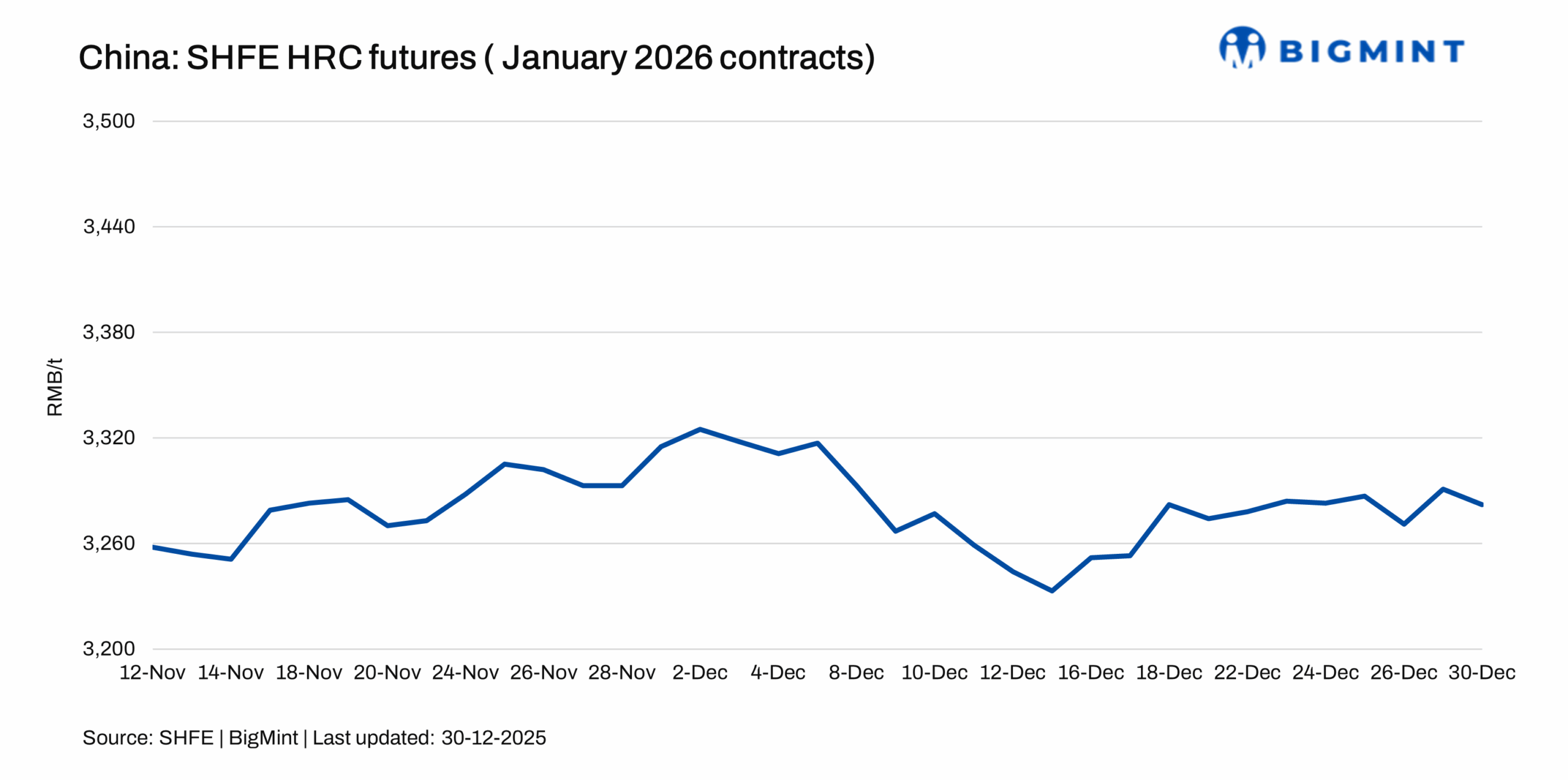

HRC January 2026 contracts on the Shanghai Futures Exchange (SHFE) remained stable w-o-w at around RMB 3,282/t ($469/t) on 30 December.

3. HRC offers to Nepal: Indian HRC export offers to Nepal remained stable w-o-w at $495/t CFR Raxaul. A deal of 16,200 t was reportedly concluded at $490-495/t CFR for January 2026 shipment. A BigMint source indicated that although Indian mills continued to push prices higher, buying interest stayed subdued as buyers adopted a cautious stance."

Outlook

Indian HRC export offers are expected to show mixed sentiments, as year-end holidays continue to weigh on buying interest across key markets. However, Indian steel mills have increased their domestic HRC prices and a further uptrend is expected in the early January. Furthermore, Indian currency depreciation is expected to provide better realisations to mills for exports. The overall outlook remains mixed, with a meaningful recovery in export activity likely only once demand picks up and market participants return after the year-end holidays.