India's crude steel output hits record high in Jan'26 even as downstream growth concerns persist

...

- Manufacturing PMI rises but business confidence slips to 3-year low

- IIP slows even as construction goods output climbs to 2-year high

- Auto sales surge m-o-m on robust rural demand, PV inventory slides

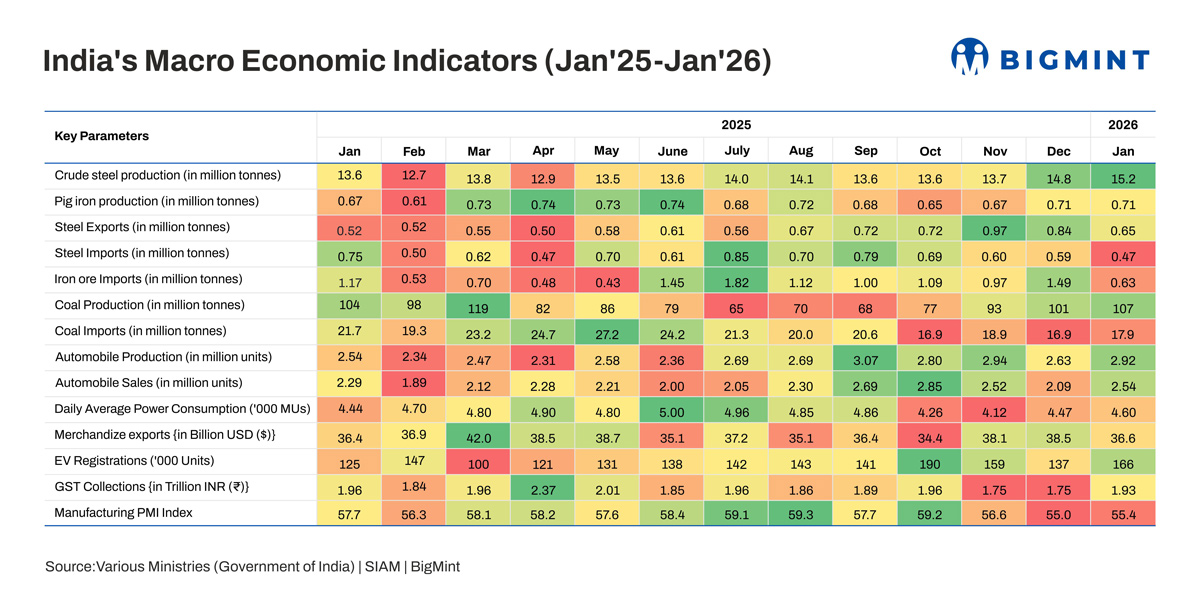

Morning Brief: India's crude steel production hit a record 15.15 million tonnes (mnt) in January 2026, the highest monthly volume ever recorded. Expectations of 8-10% steel demand growth in FY'26 have kept the Indian steel industrys prospects bright and pushed steelmakers to steadily ramp up output.

However, considering key macroeconomic indicators, while activity in the infrastructure, automotive, and manufacturing segments continued to expand, concerns persisted. Notably, signs of slowing momentum emerged in manufacturing, driven by geopolitical tensions and external trade headwinds.

Highlights of India's steel, iron ore, coal Industry dynamics

While crude steel production increased 2% m-o-m in January, steel exports moderated m-o-m but remained elevated, as India continued to ship high volumes to the EU before demand slowed due to the Carbon Border Adjustment Mechanism (CBAM). Meanwhile, imports fell 20%, driven by the full implementation of the safeguard duty during December-end.

Meanwhile, iron ore imports fell sharply, following elevated arrivals in the previous month. Iron ore and pellet production had increased by 5% and 6% m-o-m, respectively, in December, indicating improved domestic supply.

Coal production also rose, supported by improved operational momentum at Coal India. The miner's production rose 5.5% y-o-y to around 80 mnt in January.

Key macroeconomic Indicators in Jan'26

IIP slows; infra activity logs strongest growth

The Index of Industrial Production (IIP), tracking India's industrial output, expanded at 4.8% y-o-y in January -- a three-month low. Among sectors, manufacturing experienced the steepest drop to 4.8% in January from 8.4% in December, dragged down by the wearing apparel, leather goods, and pharmaceutical segments-- segments significantly affected by the increase in US import tariffs to 50%.

Within manufacturing, the strongest performers included basic metals (13.2%), motor vehicles, trailers and semi-trailers (10.9%), and other non-metallic mineral products (9.9%, led by cement, cement clinkers, and stone chips). Basic metals growth was supported by increased production of steel products such as alloy steel flats, mild steel slabs, and hot-rolled coils (HRCs).

In terms of use-based classification, infrastructure and construction-linked goods output grew 13.7%-- the highest since August 2023. This suggests strong construction activity and healthy raw material demand. The fourth quarter of the fiscal year generally experiences robust construction momentum due to favourable weather conditions, with project segment activity accelerating to meet fiscal-end deadlines.

Rural demand anchors auto sales growth

Automotive production increased 11% m-o-m in January, while at the wholesale level, sales surged 22%. Robust demand continued following the reduction in the Goods and Services Tax (GST) rates; this, coupled with a steady reduction in inventory, likely strengthened production enthusiasm.

Demand remained healthy across both mobility and freight segments. Strong rural cash flows, driven by agricultural harvest incomes and seasonal spending related to weddings, supported higher vehicle purchases. Festive events such as Pongal and Makar Sankranti and the wedding season further boosted rural footfall at dealerships.

At the retail level, passenger vehicle inventories softened to around 32-34 days in January from 37-39 days in December. Rural sales grew 14% y-o-y, much faster than the urban market's 3% growth, as per the Federation of Automobile Dealers Associations (FADA).

Heating demand drives up power consumption

Driven by a prolonged cold wave across northern and eastern India, which significantly increased heating demand, daily average power consumption increased by 3% m-o-m. Sustained industrial activity also supported power demand growth and, consequently, coal consumption.

Merchandise exports dip

India's merchandise exports fell 5% m-o-m, as trade headwinds continued. Exports to the US, India's largest trading partner, fell 4.5% m-o-m, amid the impact of elevated tariffs. Meanwhile, imports surged 12% m-o-m to $71.24 billion, attributed to higher gold and silver inflows. Consequently, the trade deficit widened to a three-month high of $34.68 billion.

Manufacturing PMI up but business confidence remains weak

India's manufacturing purchasing managers' index (PMI) -- tracking market sentiment in the manufacturing sector -- rose to 55.4 points in January from 55.0 in December, as new orders, output, and demand strengthened after a year-end slowdown. Domestic demand remained the primary driver, while export growth continued but at one of its weakest rates in the past 15 months.

Input costs increased at the fastest pace in four months, though the rise remained moderate by historical standards. Higher costs were reported for chemicals, copper, iron, jute, paper, steel, and transportation, which created slight pressure on manufacturers' profits.

Despite the stronger activity, business confidence weakened, reaching its lowest level since July 2022, as most firms expect little change in output over the coming year.

Outlook

BigMint expects sustained public infrastructure spending and 2025's GST rate cuts to continue supporting the rise in domestic steel consumption in the rest of Q4FY'26. Easing trade restrictions -- with the India-EU and India-US trade deals -- will also support steel procurement and operational momentum across export-oriented industries.

However, in March, industrial output is likely to be adversely affected by the Middle East conflict. Heavily export-oriented segments such as agricultural products and textiles have already faced logistics disruptions, with rising freight expenses and fears of potential attacks leading to deferral of shipments. Coupled with oil and gas shortages, the logistics disruptions will certainly drag down industrial output, though the impact may not be immediately evident.

Steel exports to the Middle East, which typically comprise around 60-70,000 t per month, have stalled, and supply concerns regarding raw materials such as South African thermal coal have also emerged. Steel production may decline if supply shortages become pronounced and energy costs become unviable.