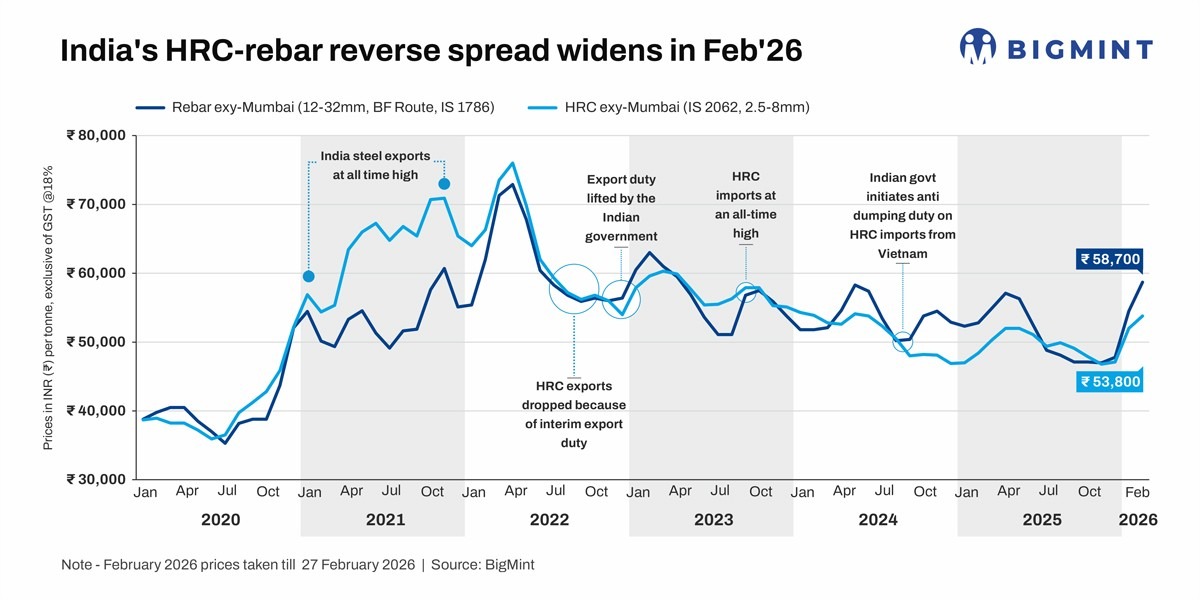

India: Primary rebar prices rise faster than HRC, higher by nearly INR 5,000/t in Feb'26

...

- HRC-rebar negative spread deepens in Feb as mills sustain rebar hikes

- Rebar rises on inventory drawdown, HRC market sees trade slowdown

- Mills looking to hike prices in early March, Iran crisis adds to volatility

Morning Brief: The reverse or negative spread between domestic hot-rolled steel coil (HRC, IS 2062, 2.5-8mm) and blast furnace-origin reinforcement bar (12-32mm, IS 1786) prices in the domestic market expanded sharply to - INR 4,900/t in February compared to - INR 2,500/t in January, as per BigMint assessment.

Data show that while HRC prices in the domestic market increased by just 3.4% m-o-m in February to an average of INR 53,800/t for the said grade, BF rebar prices increased much sharply by around 8% m-o-m. Therefore, the price rally since end December 2025 has benefitted construction steel prices more than HRC.

The domestic HRC-rebar reverse spread has again touched levels last witnessed in April 2025. Global weakness and the sharp decline in imports have resisted HRC from rising sharply even as the BF mills have raised rebar prices continuously backed by steady offtake from the projects segment and declining inventory.

Under normal circumstances, the spread between HRC-rebar stands at around INR 4,500-5,000/t.

Steel price trends in Feb'26

Rebar maintains upward trajectory: The primary steelmakers increased rebar prices by up to INR 3,000/t ($33/t) for early-February dispatches over end-January levels in the second week of the month and followed it up with successive INR 1,000/t hikes in the remaining weeks of the month.

Healthy order bookings supported market sentiment and prompted price hikes, with several mills also facing substantial order backlogs. Inventory levels at primary mills fell by around 40% m-o-m in early-February on strong dispatches in January, which led to inventory reduction.

Additionally, the shutdown of a major steelmaker's blast furnace for capacity upgradation since September 2025 constrained availability. Trade participants indicated that ''major mills are operating with restricted inventories and are largely booked for nearly a month due to ongoing project commitments, thereby limiting spot supplies and creating shortages of certain sizes''.

These factors led the mills to keep sustained price hikes throughout February despite softening trade sentiments in the latter half of the month and the decline in IF rebar prices towards the end of the month.

HRC market softens towards month end: The primary steelmakers increased list prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 1,750-2,500/t ($19-28/t) for early February sales. Notably, after the release of January sales prices, list prices were revised twice or thrice in the month. As a result, in early February, the cumulative m-o-m increase in list prices was INR 2,500-3,250/t ($28-36/t).

Demand remained stable, while some regions witnessed tight supply. Some market participants also reported smooth absorption of prior price hikes and potential acceptance of a price rise. Higher raw material costs were also another key factor influencing the sharp uptick in prices till the middle of the month. Additionally, HRC imports decreased by over 20% m-o-m in January and HRC export prices to the EU rose on the back of strong domestic.

However, towards the end of the month, the trade market turned muted across key regions on soft sentiments. While most markets saw stable to soft trends, tight availability of some specifications in certain markets in south India kept prices supported. Trade slowdown ahead of the Holi festival affected prices in end-February.

Outlook

Buoyant economic momentum ahead of the fiscal year-end will support steel prices, and mills are already looking at a hike for early March. Geopolitical conflict in the Middle East has added an extra layer of volatility; if energy prices soar and logistics disruptions follow in the event of a prolonged conflict then steel prices are expected to increase.

We believe the spread will remain negative in March. But HRC prices have room to rise further considering the spread with imported prices, while rebar seems to be nearing a ceiling.