India power market: Early april demand holds steady, but market balance turns decisively loose

...

- India enters summer with comfortable power surplus and falling market prices

- Coal loses momentum as renewables and hydro increasingly meet demand

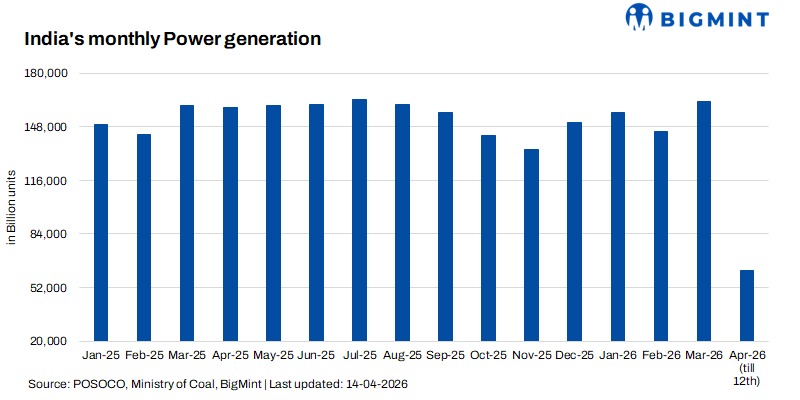

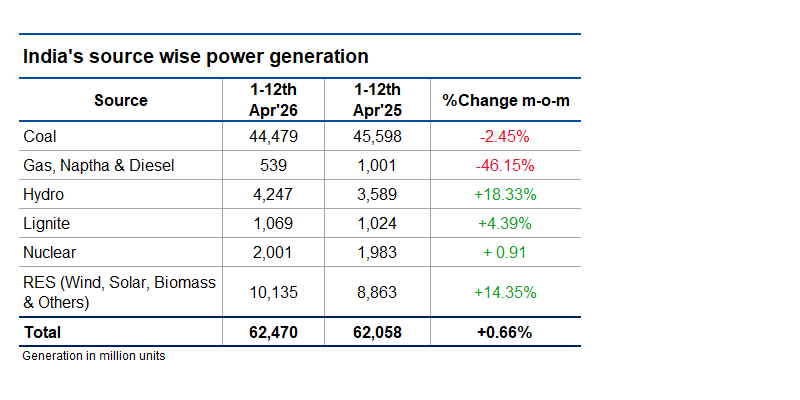

The first 12 days of April 2026 present a nuanced picture of India's power market. Total electricity generation during this period stood at 62,470 million units (MU), compared to 62,058 MU in the same period last year - a marginal increase of just 0.66%. While this headline figure suggests a broadly stable demand environment, the internal composition of supply and the behaviour of the spot market point to a system that is increasingly well-supplied, with emerging signs that the tightness witnessed in March is now easing.

The changing generation mix: Coal loses ground to renewables

At first glance, flat generation growth might imply little has changed. However, the underlying composition tells a more important story. Coal-fired generation - still the backbone of India's power system - actually declined by 2.45% compared to April 2025, falling from 45,598 MU to 44,479 MU. This decline occurred even as total demand held steady, indicating that coal is being displaced at the margin.

The table below illustrates the shifting generation landscape:

Renewable energy sources led the growth, adding 1,272 MU - a remarkable 14.35% increase over last year. Hydro generation also contributed significantly, rising by 18.33% or 658 MU. Together, renewables and hydro accounted for more than four times the incremental generation needed to meet the modest rise in demand. Gas-based generation, meanwhile, collapsed by nearly half, reflecting the poor economics of gas-fired power in a coal-and-renewables dominated market.

The structural shift becomes even clearer when examining generation shares. Coal's share of the total generation mix fell from 73.5% in April 2025 to 71.2% in April 2026 - a decline of 2.3 percentage points. Over the same period, renewable energy's share expanded from 14.3% to 16.2%, gaining 1.9 percentage points. Hydro also increased its share marginally from 5.8% to 6.8%. This confirms a clear trend: coal is no longer driving growth; it is being displaced at the margin by cleaner sources.

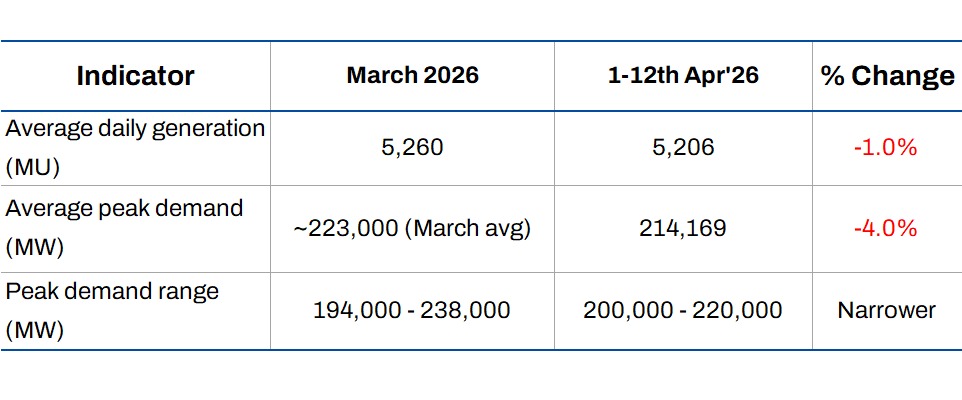

Demand trends: Steady but not yet surging

Peak demand data reinforces the picture of a stable but not aggressive demand environment. During the first 12 days of April 2025, peak demand ranged from approximately 199,000 MW to 223,000 MW. In April 2026, the range was nearly identical - from about 200,000 MW to 220,000 MW. The average peak demand met during this period increased only modestly, from 212,756 MW to 214,169 MW, a gain of just 0.66%.

TABLE

Notably, the timing of peak demand has shifted. In April 2025, peaks occurred predominantly during late morning and afternoon hours (9:00 AM to 4:30 PM). By April 2026, the peak had shifted decisively to evening hours, typically between 7:00 PM and 8:00 PM. This suggests changing consumption patterns, possibly driven by increased residential air-conditioning use as summer approaches. However, the absence of a sharp year-on-year increase in peak demand levels indicates that summer demand, while building, has not yet accelerated dramatically.

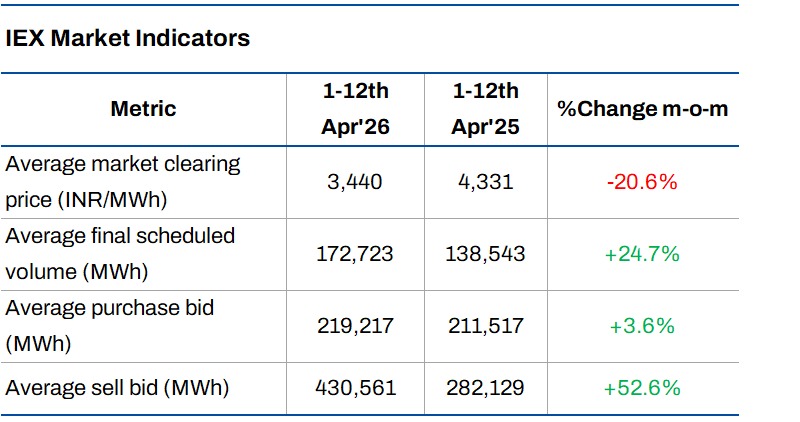

IEX market signals: From tightness to oversupply

The most telling shift in market conditions is visible in the Indian Energy Exchange (IEX) data. The spot market has moved decisively from a position of tightness in March to one of comfortable oversupply in early April.

The average Market Clearing Price (MCP) fell sharply by 20.6%, from INR 4,331 per MWh in April 2025 to INR 3,440 per MWh in April 2026. Even more striking is the daily price behaviour. Between April 5 and April 9, 2026, MCP traded 50-60% below 2025 levels, dropping as low as INR 2,013 per MWh on April 5 - a level rarely seen during the early summer months.

The primary driver of this price collapse is on the supply side. Sell bids surged by 52.6% compared to last year, indicating significantly higher availability of power on the exchange. Purchase bids, by contrast, grew only modestly at 3.6%. The ratio of sell bids to purchase bids increased from 1.33 times in April 2025 to 1.96 times in April 2026 - a nearly 50% increase in the supply-demand surplus. Final scheduled volumes also rose by nearly 25%, reflecting greater market liquidity and participation.

This is a clear signal of oversupply in the spot market. The system is no longer struggling to meet demand; it is comfortably supplied, with excess generation capacity seeking buyers.

March to april momentum: Has summer demand arrived?

To assess whether summer demand is genuinely picking up, it is useful to examine the momentum from March to April 2026. The data reveals a clear cooling off after the high-demand winter months.

March 2026 saw peak demand frequently cross 230,000 MW, touching as high as 238,378 MW on March 7. Daily generation regularly exceeded 5,500 MU. In contrast, the first 12 days of April have largely remained below 220,000 MW in peak demand, with generation mostly in the 5,000-5,300 MU range.

This suggests that the momentum of March has not carried into April. Rather than accelerating, demand has moderated - as is typical during the transition from winter to spring. The sharp summer peak, typically seen in late April through June, has not yet materialised.

What this means for the coal market

The power market data has direct and important implications for the coal sector, which has been accumulating significant pit-head inventories.

First, coal is losing marginal share in the generation mix. Even with flat total demand, coal generation declined by 2.45%, while renewables and hydro absorbed the incremental load. This trend, if sustained, will have long-term implications for coal demand growth.

Second, there is no urgency for incremental coal burn. Stable power demand, combined with higher non-coal generation and well-supplied spot market conditions, means thermal power plants are not under stress. There is no immediate need to draw down coal inventories or ramp up generation.

Third, the data reinforces the pit-head stock build observed in the coal sector. With coal production remaining strong (1,040.83 MT in FY 2025-26), despatch growth slowing (1,019.50 MT), and power demand stable, the system is accumulating coal inventories upstream. As estimated previously, pit-head stocks as of March 31, 2026, stood at approximately 151 MT, with CIL holding the vast majority (130.76 MT).

Conclusion: A well-supplied system heading into summer

The early April data suggests that India's power system is entering the summer season with stable but not aggressive demand, increasing renewable and hydro contribution, loose supply conditions in the spot market, and reduced reliance on coal at the margin. The tightness recorded in March, when peak demand crossed 238 GW and MCP spiked above INR 6,000 - has given way to a more comfortable supply-demand balance.

The key question now is one of timing. Will peak summer demand - typically seen in late April, May, and June - tighten the system again and absorb the coal inventory overhang? Or will the combination of robust renewable generation, healthy hydro levels, and moderating demand growth allow this supply comfort to persist?

For now, it is clear that India is not short of power, and by extension, not short of coal. The market has entered the summer season with a buffer, and the pressure that characterised the early summer of 2025 has yet to reappear. Market participants will be watching the next two weeks closely for the first signs of the seasonal demand surge.