India: Portside Indonesian thermal coal market stays firm as export policy uncertainty hovers

...

- Stocks at the Indian power plant decline marginally

- Global Indonesian prices inch up

Indian portside prices of Indonesian-origin thermal coal witnessed a marginal increase during the week ended 12 June 2026, with most imported coal grades sustaining levels close to their highest point in nearly three years.

The price firmness was largely driven by restricted spot availability from Indonesia, steady demand from Asian buyers, and uncertainty surrounding Indonesias upcoming export policy framework.

Market participants indicated that "Indian buyers remained cautious at prevailing high price levels and continued to prefer domestic coal availability. Meanwhile, demand from China and Vietnam remained supportive, providing strength to Indonesian coal prices. The proposed export centralization policy in Indonesia has added further uncertainty, as miners are expected to have limited flexibility in releasing cargoes. Under the new framework, export approvals and pricing mechanisms are likely to come under greater government oversight, which may impact miner margins, particularly for large producers with higher operating costs."

Marginal improvemnt in portside prices

Premium 5,000 GAR coal prices increased by around INR 100/t w-o-w to approximately INR 11,000/t at Kandla and INR 10,900/t at Visakhapatnam. Similarly, 4,200 GAR coal prices moved up by INR 100/t to around INR 9,100/t at Kandla and INR 9,000/t at Visakhapatnam.

The lower-calorific 3,400 GAR segment recorded stronger gains, rising by nearly INR 250/t week-on-week to around INR 7,100/t at Navlakhi. The increase was primarily attributed to limited availability of ready stock and tighter spot supply conditions.

Freight rates ease marginally but continue to support delivered costs

Freight rates for Supramax vessels from East Kalimantan to Navlakhi increased slightly w-o-w by around $0.2/t during the week to nearly $22/t. Although freight movement remained relatively stable, elevated shipping costs continued to provide support to delivered coal prices.

Port inventories witness minor drawdown amid comfortable supply

Coal inventories at major Indian ports declined by 1.9% week-on-week to around 15.31 million tonnes (mnt) in Week 23 compared with 15.61 mnt in Week 22. The decline reflected mixed inventory trends across ports, while overall availability remained adequate.

Imported coal demand remained subdued as domestic coal supply continued to support consumption requirements, limiting aggressive procurement from international markets.

Power plant stocks decline despite adequate overall availability

Thermal power plant coal inventories declined week-on-week to approximately 47 mnt, equivalent to around 16 days of consumption. While the broader supply situation remained comfortable, around 26 power plants continued to report critical stock levels, highlighting uneven distribution and regional supply constraints.

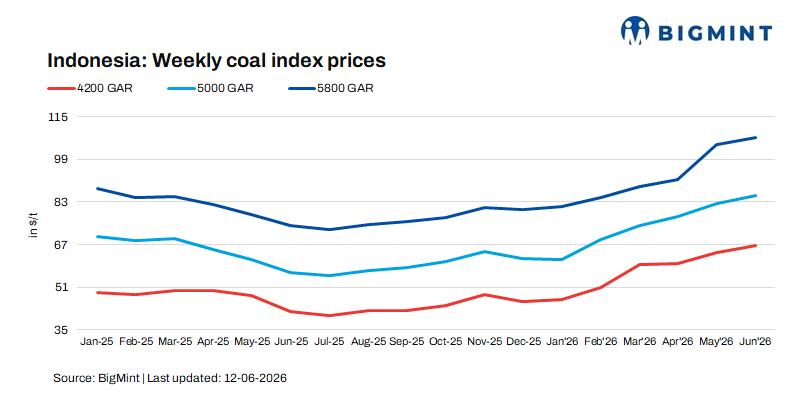

Global market support from tight Indonesian availability

International thermal coal markets remained firm, supported by stable Asian demand and tighter availability of Indonesian spot cargoes. Benchmark 5,800 GAR prices increased marginally by around $0.5-1/t week-on-week, while 4,200 GAR and 3,400 GAR grades gained approximately $1/t and $0.5/t, respectively.

Outlook

Indonesian thermal coal prices are expected to remain supported in the near term due to restricted spot availability, strong Chinese buying interest, and uncertainty around Indonesia's export policy implementation. However, upside potential in the Indian market may remain limited as buyers continue to rely on domestic coal and resist high imported coal prices.

Going forward, market direction will largely depend on the pace of Indonesia's export policy rollout, availability of spot cargoes, and demand recovery from Indian power and industrial consumers. A sustained supply squeeze could keep prices elevated, while improved domestic availability in India may cap further increases.