India: Pig iron prices inch down in Jun'26 amid weak demand; exports cushion downside

...

- Pig iron-scrap price spread widens; cheaper metallic substitutes cap demand

- Auction participation improves towards month-end as availability tightens

India's pig iron prices fell marginally across most regions in June 2026 amid weak downstream demand and cautious buying. Procurement remained predominantly need-based as steelmakers and foundries refrained from building inventories due to sluggish finished steel demand and comfortable stock levels. Lower-priced substitute metallics such as sponge iron and steel scrap further weighed on domestic consumption. However, firm export bookings, relatively stable raw material costs, controlled supplies, and dispatch constraints prevented a sharper decline in prices.

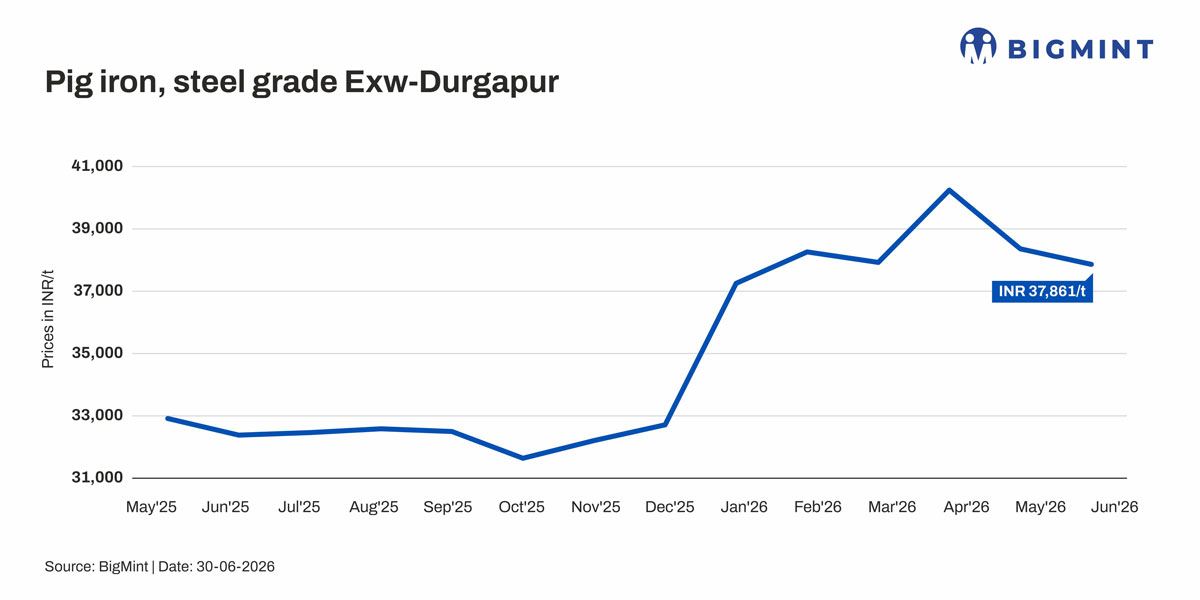

According to BigMint, Durgapur steel-grade pig iron prices declined by around INR 486/t (1.27%) m-o-m to INR 37,861/t in June from INR 38,348/t in May.

Raw material costs remain firm

Raw material prices remained largely stable to firm during the month, continuing to provide a cost floor to pig iron prices. Premium hard coking coal prices increased by around $2/t m-o-m to $265/t CFR Paradip, while merchant BF-grade met coke prices edged up by around INR 50/t to INR 36,600/t ex-Jajpur.

Although raw material procurement by integrated steelmakers remained limited due to comfortable inventories and earlier bookings, elevated production costs discouraged producers from offering aggressive discounts. Easing freight costs, however, provided partial relief and are expected to keep input costs broadly stable in the near term.

Cheaper metallic substitutes restrict pig iron demand

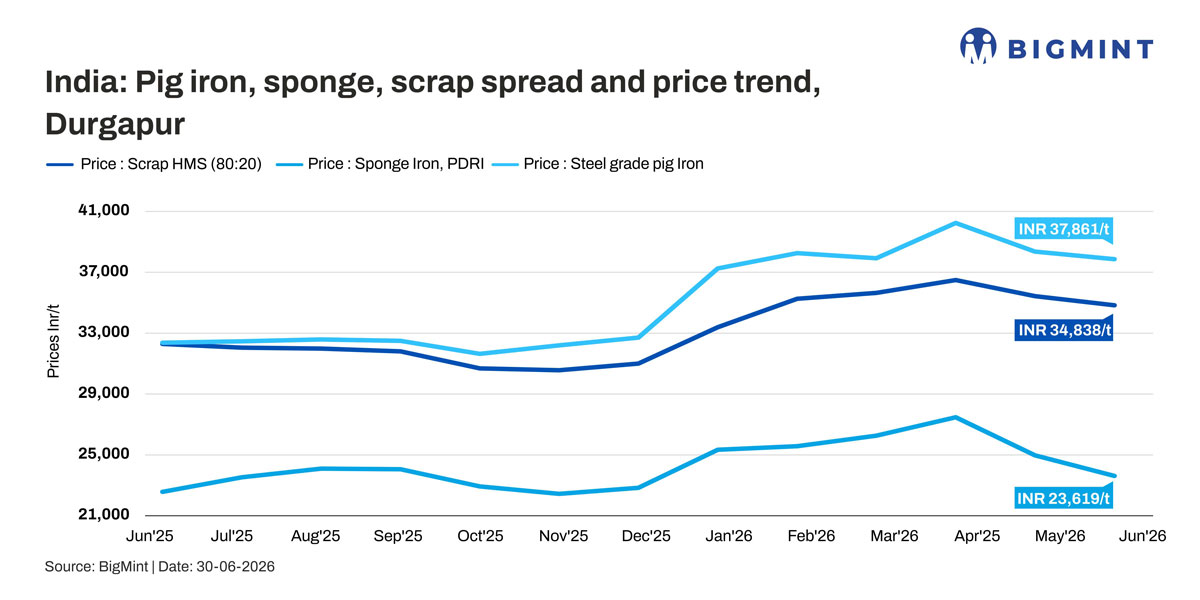

Pig iron continued to lose competitiveness against alternative metallics during June. HMS 80:20 prices declined by around 1.7% m-o-m to INR 34,838/t, while Durgapur sponge iron prices fell nearly 5.4% to INR 23,619/t.

With pig iron trading at around INR 37,861/t, the premium over HMS 80:20 widened to approximately INR 3,023/t, making scrap a more economical feedstock for secondary steelmakers. The sharp correction in sponge iron prices further encouraged mills to optimise their metallic charge mix, restricting pig iron purchases to immediate requirements.

However, substitution remained limited in eastern India, where steelmakers generally maintain a metallic charge mix of nearly 70:30 between sponge iron and other metallics, including pig iron, scrap and ferro alloys, thereby sustaining baseline pig iron consumption.

Steel-grade pig iron auction prices recover towards month-end

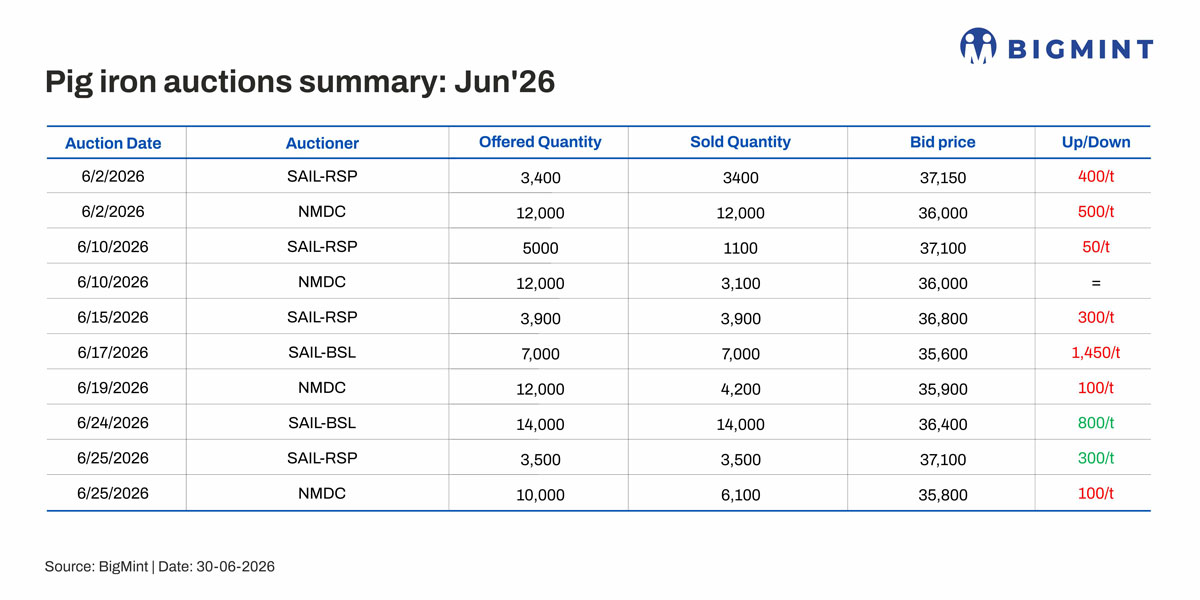

Steel-grade pig iron auctions remained mixed during June, with sentiment improving in the second half of the month. SAIL conducted five auctions, offering 36,800 t, of which 32,900 t was sold. Bids ranged between INR 35,600-37,150/t, with prices atthe latest Bokaro Steel Plant auction rebounding by INR 800/t after a sharp correction earlier in the month.

NMDC conducted four auctions, offering 46,000 t, with 25,400 t booked. Bid prices remained largely stable at INR 35,800-36,000/t, although buyer participation stayed cautious.

NMDC conducted four auctions, offering 46,000 t, with 25,400 t booked. Bid prices remained largely stable at INR 35,800-36,000/t, although buyer participation stayed cautious.

Overall, stronger export bookings and tighter spot availability supported auction sentiment towards month-end, while procurement continued to remain largely need-based amid weak domestic demand.

Exports continue to underpin market

Exports remained the strongest pillar supporting the domestic pig iron market throughout June. Major eastern producers reportedly booked nearly 300,000 t of pig iron for exports at around $435-440/t FOB, significantly above domestic realisations.

Export commitments tightened spot availability in eastern India and supported producer sentiment despite sluggish domestic demand. Dispatch delays and heavy order pipelines also contributed to tighter supplies, preventing producers from offering significant discounts.

Regional markets

Eastern India

Eastern India remained the most resilient region during June. Steel-grade pig iron prices corrected by around INR 500/t, largely trading within INR 37,500-38,100/t. Robust export bookings, inter-regional dispatches to north India and Jharkhand, and procurement of around 10,000-15,000 t by major Kharagpur-based buyers reduced spot availability. However, delivery delays remained a challenge as producers prioritised export commitments.

Central India

The central Indian market remained subdued amid weak downstream demand. Buyers increasingly preferred lower-cost sponge iron and scrap over pig iron. According to BigMint, Raipur pig iron prices declined by INR 800/t m-o-m to INR 37,200/t DAP, while Raigarh prices eased by INR 200/t to INR 38,000/t DAP. Weak participation in NMDC Nagarnar auctions reflected cautious buying, although limited spot availability prevented sharper corrections.

North India

The north Indian market remained balanced as improved supplies from eastern India eased earlier shortages. Procurement continued on a need basis, with most transactions executed on advance payment terms. Although export bookings remained strong, their impact on northern availability had yet to fully materialise. Market participants expect export-led supply tightness to gradually support prices in Ludhiana and Delhi over the coming weeks if downstream demand improves.

South India

South India also witnessed a largely stable market during June. Prices corrected marginally by around INR 200/t to nearly INR 37,000/t. A leading southern producer exported around 30,000-50,000 t, tightening regional supplies. However, sluggish domestic demand and cautious procurement offset the impact of lower availability, keeping prices largely range-bound.

Outlook

Pig iron prices are expected to remain largely stable in July. Weak domestic demand, comfortable inventories and competitive pricing of substitute metallics are likely to keep procurement cautious, while the monsoon season may further restrict buying activity.

Nevertheless, sustained export bookings for July-August, relatively firm raw material costs, controlled spot availability, and ongoing dispatch commitments are expected to prevent any significant downside. Unless domestic steel demand improves meaningfully, the pig iron market is likely to remain stable with a mildly bearish bias in the coming weeks.