India: Petcoke prices soften as cement buyers delay purchases amid monsoon lull

...

- Buyers delay fresh purchases amid ample inventories

- US NAPP coal stays key competing fuel, domestic prices dip

Imported petcoke prices into India have continued to soften in June as weak cement-sector buying, ample spot availability, and falling US Gulf Coast prices weigh on market sentiment. However, elevated freights and fuel-switching economics with US NAPP coal are preventing a sharper collapse in delivered prices.

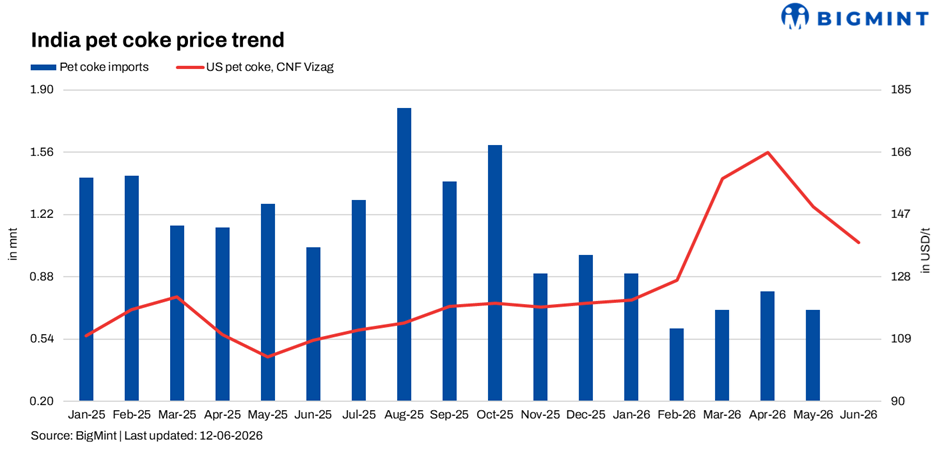

CFR India high-sulphur petcoke offers were largely heard around $132-138/t, with some buyers bidding closer to $125-130/t. The correction follows a sharp fall from May levels, when imported petcoke remained expensive and cement producers had increased the share of domestic coal and US NAPP coal in their kiln fuel mix.

Cement buyers stay cautious

Indian cement producers are not facing an immediate fuel shortage. Several buyers are covered with existing inventories and are delaying fresh purchases for August or post-monsoon delivery. Market feedback indicates that enquiries have slowed, with buyers expecting further price softness as construction activity eases during the monsoon.

Major cement buyers are also actively comparing petcoke with US NAPP coal and domestic coal. While petcoke has regained competitiveness after the recent correction, buyers are not rushing to accumulate cargoes. Instead, they are adopting a hand-to-mouth strategy and waiting for a clearer price direction.

US Gulf prices under pressure

The weakness in India is feeding back into the US Gulf Coast market. High-sulphur petcoke prices have fallen sharply in recent weeks as sellers try to clear cargoes into India, Turkiye, and other consuming markets.

FOB USGC high-sulphur petcoke is now near the high-$70s/t level, down significantly from early-May levels. The decline reflects better supply availability, weaker Indian buying and pressure on traders holding prompt cargoes.

NAPP coal remains a key competing fuel

US NAPP coal continues to act as a price anchor for petcoke in India. Offers for 6,900 kcal/kg NAR NAPP coal are heard in the low-to-mid $130s/t CFR west coast India, broadly overlapping with current high-sulphur petcoke offers.

This has narrowed the energy-adjusted gap between the two fuels. Cement producers who shifted towards coal earlier this year are now reassessing petcoke, but only where prices are attractive enough. The market is therefore not seeing a one-way switch, but a more flexible fuel-balancing strategy.

Domestic petcoke also adjusts lower

Domestic petcoke prices in India have also been cut, reflecting weaker import parity and subdued demand. This adds another layer of competition for imported cargoes, especially as local material remains available and buyers are avoiding heavy forward coverage.

Outlook

The near-term outlook remains bearish to stable. Indian demand is expected to stay muted through the monsoon, and buyers are likely to resist offers unless prices fall closer to their target levels.

However, a steep decline may be limited by high freight costs, Middle East-related shipping risks, and the possibility that petcoke demand returns quickly if prices move decisively below competing coal on an energy-adjusted basis.

For now, the Indian petcoke market remains buyer-driven. The key level to watch is $125-130/t CFR India. If sellers accept this range more widely, fresh cement-sector buying may emerge; otherwise, the market is likely to remain quiet.