India: Iron ore concentrate prices remain rangebound amid demand uncertainty

...

- Absence of transactions reflects weak market activity

- Pending negotiations highlight widening bid-offer gap

Iron ore concentrate prices in the Jabalpur region remained under pressure during this assessment period as weak market sentiment, limited buying interest, and a widening gap between buyer expectations and seller offers continued to suppress trading activity. The absence of significant fresh transactions highlighted the cautious stance adopted by market participants amid uncertainty surrounding raw material prices and downstream steel demand.

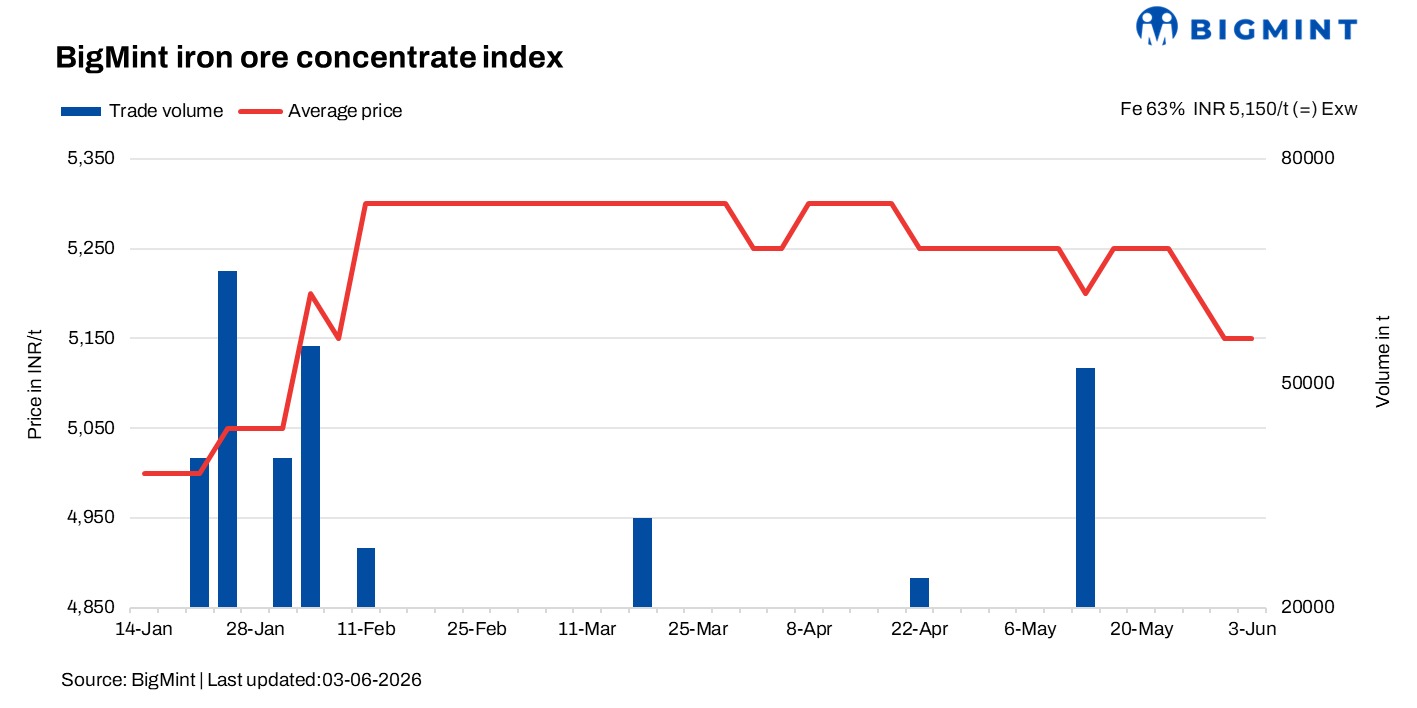

According to BigMint's latest bi-weekly assessment, Fe 62% iron ore concentrate prices were assessed at INR 5,150/t ($54/t) ex-works, unchanged from the previous assessment on 30 May 2026. Meanwhile, Fe 63% concentrate was heard at around INR 5,400/t ($56/t) ex-works.

Market activity remained largely muted as suppliers focused on executing previously booked orders rather than pursuing fresh sales. Despite the softer outcome of the recent Odisha Mining Corporation (OMC) iron ore fines auction, sellers refrained from revising offers downward, citing ongoing dispatch commitments and limited urgency to liquidate inventories. Several transactions had reportedly been concluded prior to the auction, allowing suppliers to maintain current offer levels despite weakening sentiment.

The cautious mood in Jabalpur mirrored broader trends across Odisha's iron ore and pellet markets, where weak downstream demand and shrinking steel margins have prompted buyers to adopt a wait-and-watch approach. Buyers are increasingly seeking discounts in anticipation of further price corrections, while suppliers remain unwilling to lower offers beyond sustainable levels. This divergence in price expectations has widened the bid-offer gap and delayed multiple negotiations, resulting in reduced market liquidity.

Adding another layer of complexity to the market, NMDC increased its iron ore prices for June deliveries despite the subdued spot market environment. The miner raised prices of DR CLO (10-40 mm, Fe 67%) to INR 6,150/t ($65/t) and iron ore fines (-10 mm, Fe 64%) to INR 4,700/t ($49.5/t) on a FOR Bacheli basis, excluding royalty, DMF, and NMET. The increase of INR 50-100/t across grades reflects the miner's confidence in longer-term demand fundamentals, although its immediate impact on the concentrate market remains limited.

A Jabalpur-based supplier told BigMint that producers are currently prioritising fulfilment of existing orders and are unlikely to revise prices until pending dispatches are completed. He added that fresh offers may be reviewed thereafter, depending on prevailing market conditions and inventory positions.

On the demand side, buyers remain cautious. Market participants noted that current offer levels are failing to generate meaningful purchasing interest, with consumers expecting additional downside in the coming weeks. The approaching monsoon season has further reinforced this sentiment, as buyers anticipate that logistical disruptions and inventory pressure may eventually compel sellers to offer discounts to accelerate material movement.

Rationale

- One (1) trade was recorded in this publishing window and is not taken into consideration, receiving a 0% weightage.

- Thirteen (13) offers and indicative prices were heard, and eleven (11) were taken into consideration as T2 trades, receiving 100% weightage.

Factors affecting prices

- PELLEX declines by INR 150/t ($1.5/t) w-o-w: PELLEX, BigMint's bi-weekly domestic pellet (Fe 63%) index for Raipur declined by INR 150/t to INR 9,400/t ($98/t) DAP on 2 June compared with 26 May, reflecting persistent weakness in demand and bearish sentiment across the steel value chain. Pellet manufacturers lowered offers for Fe 62.5/63% (0.5%) grade pellets by INR 200/t to INR 9,200-9,300/t ($97-98/t) ex-works amid subdued buying interest and softer market fundamentals following the recent Odisha Mining Corporation (OMC) iron ore auction. The correction was further driven by declining sponge iron and billet prices, which have eroded steelmakers' margins and led to cautious raw material procurement. Sponge PDRI prices in Raipur fell sharply by INR 1,050/t m-o-m to INR 25,350/t ($267/t) ex-works in May, highlighting the broader weakness in downstream steel markets and adding further pressure on pellet prices.

- Odisha iron ore prices remain firm w-o-w: BigMint's Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,100/t ($53/t) ex-mines on 30 May. Market activity remained cautious following the OMC auction, with buyers and sellers continuing to evaluate post-auction price levels. While some private miners adjusted offers in line with auction outcomes, several producers maintained existing prices, resulting in mixed market signals and limited trading momentum.

Outlook

Iron ore concentrate prices in the Jabalpur region are expected to remain under pressure as weak buying interest, declining pellet prices, and subdued downstream steel demand continue to weigh on market sentiment. The onset of the monsoon is likely to intensify selling pressure, with buyers anticipating that suppliers may eventually offer discounts.

However, any immediate correction could remain limited as most suppliers are still focused on fulfilling previously booked orders and are not actively chasing fresh sales. Once these dispatch commitments are completed, producers are expected to reassess market conditions and announce revised offer levels based on inventory positions and demand trends.